Simulating the Long-Term Impact of Cash Assistance to Children on Future Earnings

Background

Children who grow up in low-income families are more likely to earn low incomes in adulthood than children who grow up in families with higher incomes. But to what extent can cash assistance to families with children – especially low-income families with children – improve the later-life economic outcomes of those children? In other words, how much of the difference children’s earnings as adults is due to the income their parents had and how much due to other factors that are correlated with parental income? The answer to this question, a subject of substantial academic attention, has important implications for economic mobility, racial inequality, evidence-based policy design, and other topics.

Any effect would also have important implications for budget scorekeeping: if policy interventions today can increase the income of the next generation in adulthood, some fraction of the up-front costs will be offset by higher income and tax revenues in the future. Incorporating this kind of long-run impact into budgetary analyses of policy reforms is a key mission of the Budget Lab at Yale.

In this report, we describe our approach to modeling the impact of changes in family income during childhood on labor market outcomes in adulthood.

Relevant research and existing estimates

Incorporating behavioral feedback into policy estimates involves two key assumptions:

- Functional form: How, exactly, does variable Y change causally with variable X? What are the parameters which govern this relationship? For example, Y may be linear in X such that Y = BX, where B is the parameter.

- Parameter values: Conditional on functional form choice, what are the parameter values? In other words, what is the value of B in the linear example above?

For example, to account for how investors respond to changes in tax rates, revenue estimators would typically review the empirical literature on capital gains elasticities, impose an assumption that the log of capital gains realizations varies with the percentage-point change in effective marginal tax rates, decide which estimated parameter value is most appropriate for our setting, then run simulations using that assumption.

This task is comparatively harder for the long-term impacts of cash assistance to families, a topic which is difficult to study in an empirical setting. First, the functional form is unclear, even in theory. Does the impact scale per dollar of benefit, or as a share of income? Do only low-income children benefit? Are impacts concentrated on those who would otherwise rank at the bottom in adulthood, or do all children see some benefit? How long does it take for the effects to materialize? Do effects depend on whether the cash assistance is conditional or unconditional? And so on.

Second, parameter values can be difficult to measure empirically. Doing so requires following children across generations either in a survey setting (where sample size, attrition, and measurement issues present substantial difficulties) or through administrative data (access to which, at least in the United States, is often limited). Econometric identification is another problem. Natural experiments are limited, and when available, they are typically limited to specific institutional and policy contexts. For instance, to what extent are effects estimated in prior generations or other countries applicable to the modern American experience? Can we really assume that impacts of disability insurance are similar to those of the Child Tax Credit (CTC)?

There exists a literature of empirical evidence which may be instructive. Both Duncan and Le Menestrel (2019) and Maag et al. (2023) offer broad literature reviews on the relationship between government assistance programs, both cash and noncash, and later-life outcomes of children. A more recent review from Page (2024) offers a comprehensive review of the causal literature, standardizing estimated effect sizes into comparable elasticities. Many of these studies measure the relationship between family income and educational or health outcomes – factors which affect economic outcomes, but are not economic outcomes per se. Direct causal evidence linking income in childhood with income in adulthood includes:

- Bleakey and Ferrie (2013) conduct a study tracking the outcomes of winners of a land grant lottery in the 19th century finds that large increases in family wealth did not improve economic outcomes for children.

- Aizer et al. (2016) use evidence from an early 20th century public pension program and find that income support during childhood led to more income in adulthood.

- Bastian and Michelmore (2018) find that expansions of the Earned Income Tax Credit (EITC), a federal earnings subsidy program, improve future labor market outcomes for children with parents who benefit. The main channel is higher pretax family earnings – that is, the measured effect is attributable to the EITC’s work incentives, not the cash itself.

- Price and Song (2018) study a state-level negative income tax experiment. Their estimates indicate no statistically significant impact on the economic outcomes of affected children.

- Hoynes et al. (2016) and Bailey et al. (2020) find evidence that increases in near-cash food assistance during childhood have a positive impact on an index of economic measures during adulthood.

- Exploiting a discontinuity in the timing of eligibility for child-related tax benefits, Barr et al. (2022) find a large later-life earnings effect of shifting resources to early childhood.

- Recent quasi-experimental evidence from Hawkins et al. (2023) on the Supplemental Security Income (SSI) program, which gives cash to certain families of children with low birthweights, finds no effect on later-life outcomes of these children.

Some policy researchers have relied on this evidence when estimating the budgetary and economic outcomes of a scenario in which the 2021 CTC design is made permanent:

- Garfinkel et al. (2022) rely on several of the aforementioned studies when quantifying the long-term earnings effects in a cost-benefit analysis of the 2021 CTC design.

- Goldin et al. (2022) follow the metanalysis from Garfinkel et al. (2022) and use the findings to estimate a positive 1.2 percent earnings effect for all affected children. For children with family incomes below $50,000, the effect is twice as large.

- Werner (2024) uses the Social Genome Model,1 a simulation tool which links health, educational, and economic outcomes at different stages in life, to estimate the long-term earnings impact of this CTC expansion if it were made permanent. The author finds that earnings for affected children would be increased by 7 percent to 12 percent relative to baseline, with even larger future gains for girls and Black children.

- Aizer et al. (2024) review the both growing literature on short-run impacts of the 2021 CTC expansion and the broader evidence on transfers and long-run outcomes. The authors describe in qualitative terms the likely effects of this temporary expansion.

This research has helped shape our thinking, especially on questions about potential channels and plausible magnitudes. In the extant literature, results vary widely in magnitude, and the specific institutional settings may be of limited external validity. The latter issue is especially problematic for our goal of being consistent in our approach across policy areas: we wish to express any effect in a flexible and generalized way such that it can be incorporated into any policy reform which changes families’ disposable income, whether that is a tax rate cut, an increase in the standard deduction, CTC expansion, a change in EITC eligibility, a new transfer program, or something else.

Methodology

This section describes how we incorporate the effects of cash assistance to children on later-in-life outcomes into our tax microsimulation model. The code implementing the calculations explained below can be found here.

Our approach is based on a simple idea: if we can measure the statistical association between income during childhood and income during adulthood, and if some fraction of this association is causal, then a policy reform that affects income during childhood implies some change in income during adulthood. And indeed, we can measure this association. A body of high-quality research, often based on administrative data, measures intergenerational mobility – that is, the extent to which a parent’s income can predict a child’s income.

Thus, at a high level, our approach involves three steps:

- Measure the impact of a reform in terms of changes in parent income percentile. For example, imagine a CTC reform which delivers a $5,000 tax cut to a family at the 15th percentile of the income distribution. Because the distance between the 15th and 20th percentile is about $5,000, this reform is worth 5 rank units.

- Scale the result of (1) to remove plausibly non-causal variation in child outcomes. If we believe that only, say, 20 percent of the observed difference between child outcomes at the 15th and 20th percentile of parent income is due to the causal effect of income itself, then the impact of the example reform would be scaled to 5 * 20% = 1 rank unit.

- Adjust future earnings of affected children to reflect those of children in the counterfactual parent rank. Continuing the example above, in future years of our simulation, we track the 15th percentile children into adulthood and scale their wages to reflect those who grew up in 16th percentile families.

The main benefit of this approach is its universality. At all points in the parent income distribution, we know the observed distribution of outcomes for the children of those parents. This way, we are not relying on evidence from a narrow subset of the population in some specific institutional context. Instead, we can model a broader array of policy reforms.

The downside is that this approach requires imposing strong and somewhat arbitrary assumptions about causality. Measures of intergenerational mobility are correlational, but our simulations require a notion of how income causally affects later-life outcomes. We deal with this issue by imposing structure and assuming that only a fraction of observed intergenerational correlations reflect the causal impact of income in childhood. In that sense, our estimates are more illustrative than definitive. Our goal is not to provide a final answer but instead add to the conversation by ballparking a plausible effect size. We welcome comments from other researchers and future research that will inform our estimates here.

The remainder of this section describes our approach in more detail.

Parent income rank imputation

Our tax microsimulation model has no longitudinal dimension; we project only the cross-section of tax units each year. In order to follow children into adulthood, as is required for this exercise, we need to link simulated children today with simulated adults in the future. That is, for any given adult in the simulation, we must assign a parent income rank answering the question: growing up, what was the relative income position of your family?

Our basis for this imputation is the 100-by-100 mobility matrix from Chetty et. al (2014).2 This data estimates the joint probability distribution of income rank during childhood and income rank during adulthood using U.S. tax data. We use these estimates to probabilistically assign parent income rank, ranging from 1 to 100, to each adult in our tax data conditional on their income rank, again from 1 to 100, in adulthood. Code for this imputation step can be found here.

This step is important because it allows us to account for the future distributional impacts of policy interventions today. If low-income adults are more likely to have come from low-income family – which is true – then any benefits from a reform giving resources to low-income children will disproportionately benefit low-income adults in the following generation. The first-order distributional benefits are interesting per se, but this dynamic also has budgetary implications. Because the income tax system is progressive, wage gains accruing to bottom earners will lead to less additional tax revenue than wage gains accruing to top earners.

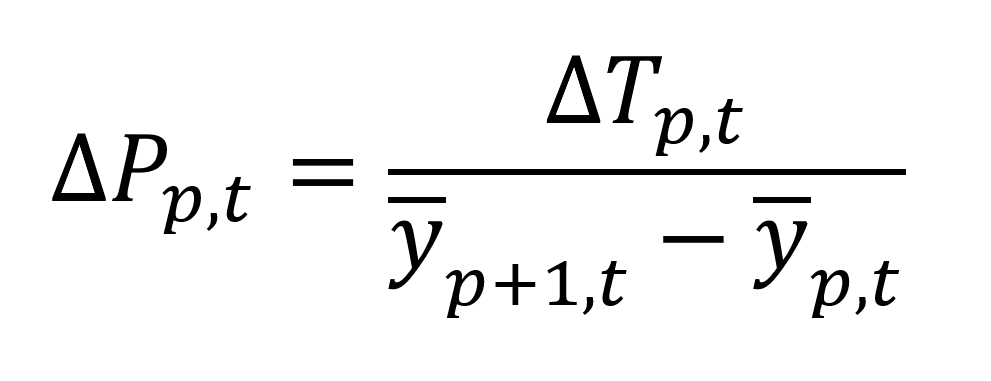

Assumed functional form

Let ȳp denote mean income for parent income rank group p. A policy reform delivers some average tax change ΔTp to families in this group, measured in dollars and weighted by number of children. Expressed in rank-space units, the size of the policy reform for children in group p in year t is:

This metric gives us a child’s one-year exposure to a counterfactual policy reform, measured in terms of income rank rather than dollars. (Note that we are not re-computing income ranks in the counterfactual scenario. Rather, we are fixing baseline income ranks and using these units as a scale for measuring the size of a reform.)

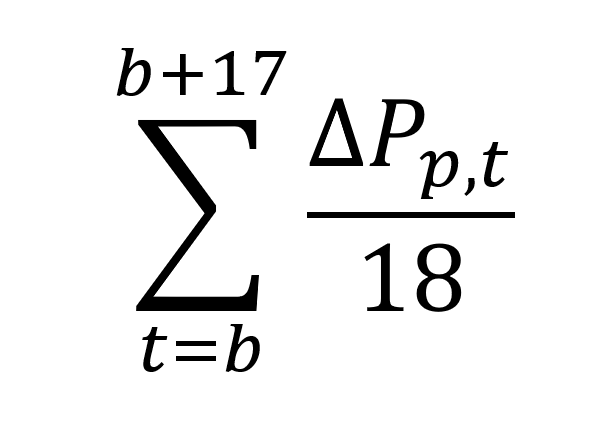

Some children will only be exposed to a few years of a reform while they are still children. For example, a child who is 16 when a policy reform is enacted will only experience two years of exposure, whereas a newborn will have a full 18 years. We assume that partial exposure is proportionally weighted to full exposure, and that total exposure is the equal-weight average across all years of childhood. For a child born in year b into a family of parent income rank p, total exposure is:

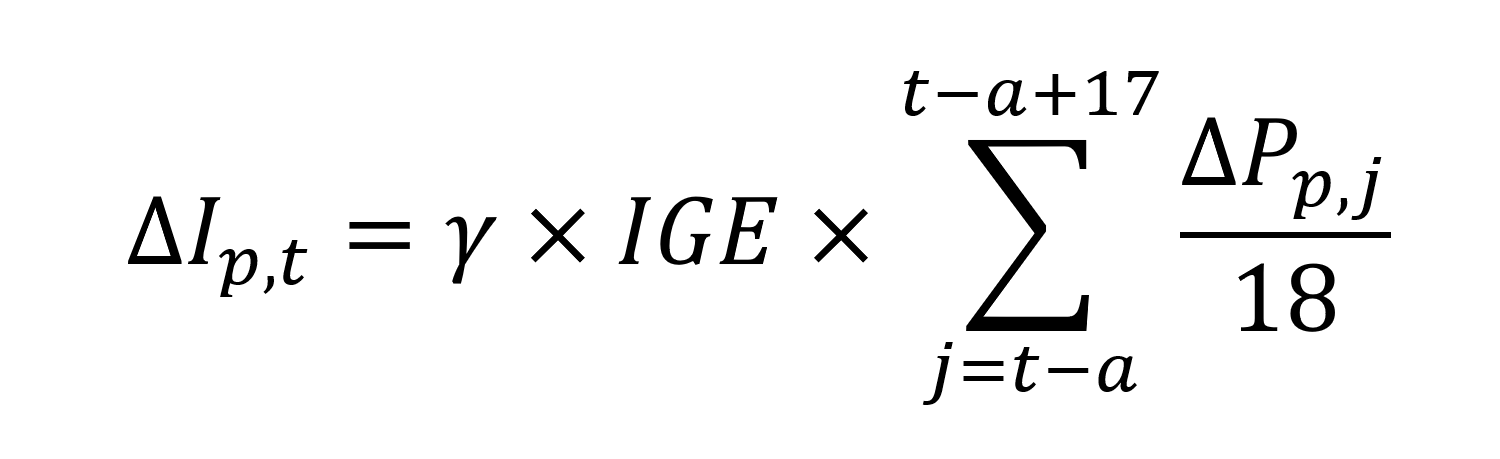

We wish to translate this quantity into the change in later-life earnings of those children. Like before, we begin in rank space rather than dollars. Let i ∈ [1..100] denote wage earnings rank for all adults. Let a = t – b denote age for each adult, such that t – a is birth year. The year t change in wage earnings, measured in rank units, for a simulated adult of age a who grew up in a family with parent income rank p is:

where IGE is the unconditional rank-rank intergenerational elasticity of income and γ is the causal share of the IGE. We provide additional details on these parameters below.

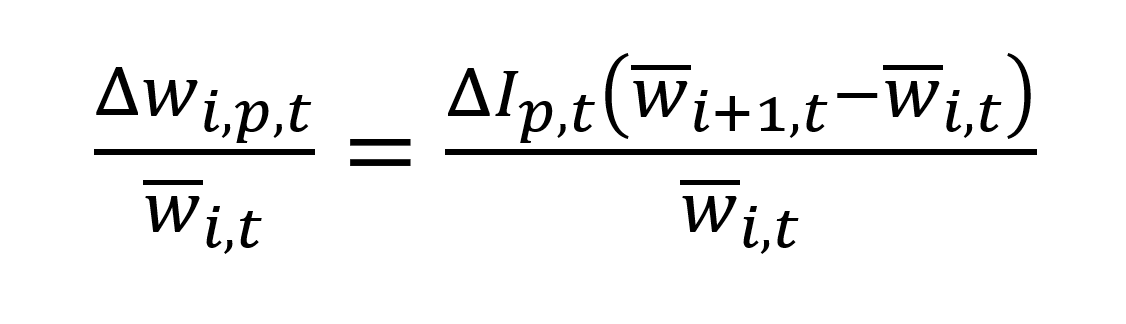

Finally, we wish to convert the change in wage earnings rank to dollars. If wi,p,t denotes year-t wage earnings for an adult of earnings group i and parent income group p, then the implied percent change in wages due to the policy reform at time t is given by:

We multiply baseline wages by one plus this quantity for all adults to get post-effect counterfactual wages.

Choice of parameter values

The next step is to choose a parameter value for the intergenerational elasticity of income (IGE) -- the extent to which additional income in childhood is associated with additional income as an adult. To be consistent with our baseline intergenerational mobility imputations, we rely on Chetty et al. (2014) for an estimate of the IGE.3

The authors show that the conventional “log-log” formulation of IGE, in which the log of child income is regressed on the log of parent income, is unstable with respect to the treatment of zero incomes. We instead use their preferred “rank-rank” formulation, which is a relative mobility metric, expressing child income rank as a function of parent income rank. The authors estimate an unconditional rank-rank IGE of 0.34. That is, a 10 percentile point in parent income rank is associated with a 3.4 percentile point increase in child income rank. Using rank units (rather than dollars) allows us to capture that a dollar is worth more to a low-income child than to a high-income child while avoiding the problems associated with logs for families with low or no incomes.

The IGE measures the univariate correlation between parent income and child income, but parent income itself is only one such factor which generates divergent child outcomes at different levels of parent income. Children of higher-income parents have better outcomes on average than children of lower-income parents in part because of the material advantages that income can buy. But there may be additional differences between families at these ranks, including the burden of racism (e.g. a greater share of lower-income families are Black), rivalrous social capital (e.g. the social background of higher-income families allows children to more easily navigate college admissions), and academic prowess. These factors are not unilaterally alleviated by additional cash income, at least not on the scale of the policy interventions we consider in our analyses.

Because our formulation requires a causal relationship, we must isolate the component of the IGE attributable only to income. To do so, we impose a causal share parameter, denoted γ above, which ranges from 0 to 1 and is multiplied through in our expression such that the implied effect of additional income is scaled downwards.4 Informed by our conversations with researchers who work on intergenerational mobility and poverty issues, and as an initial, illustrative step, we present results using a value for γ of 0.2 – that is, assuming that 20 percent of the relationship between parent income and child income is explained by the direct impact of parent income.

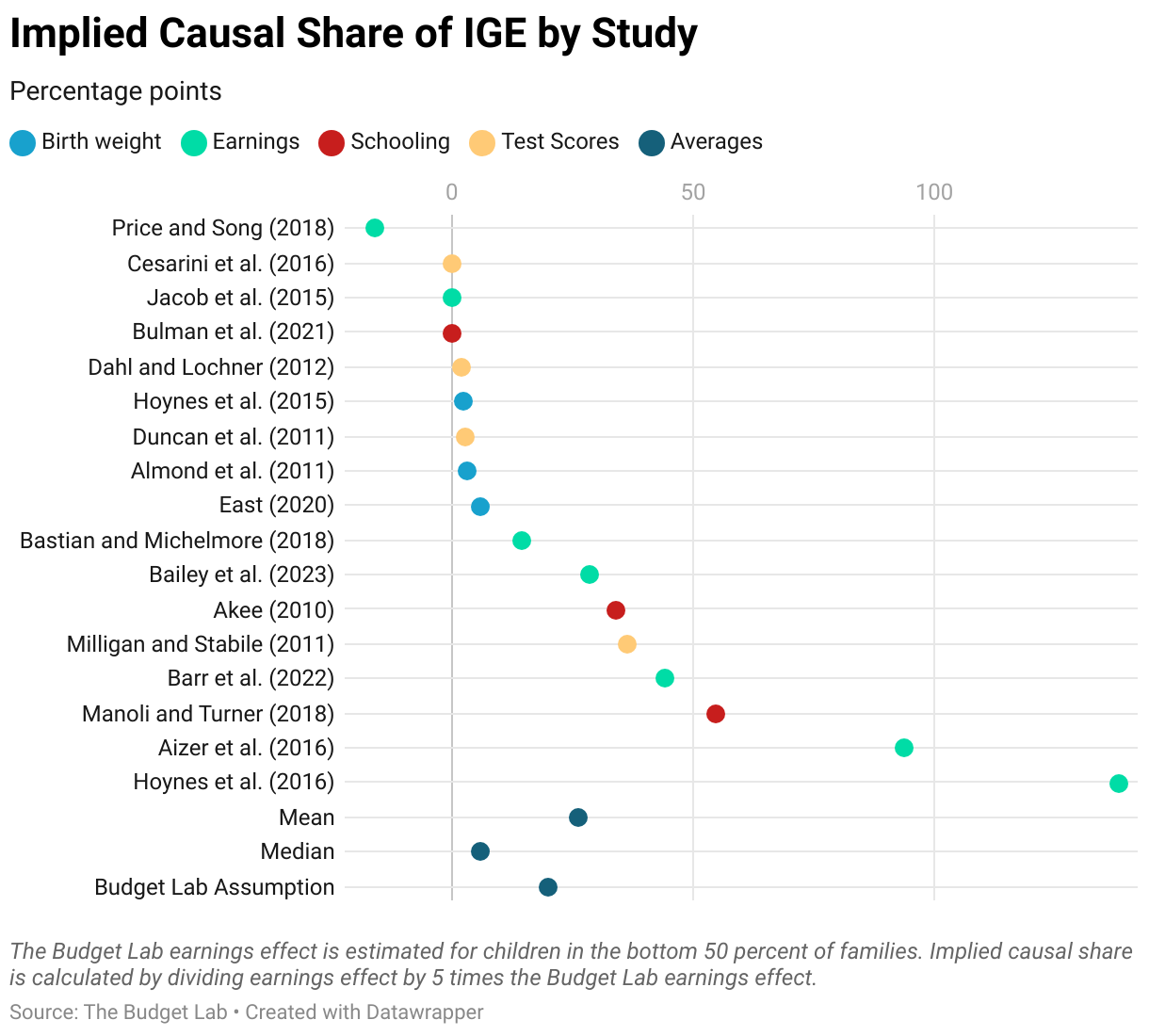

How does this assumption compare with existing causal evidence? While researchers do not express results in terms of a causal share of the IGE, we can calculate a back-of-the-envelope implied casual share for major studies. The following graph shows a range of estimated effect sizes in the literature, expressed in terms of the causal share. We begin with the standardized elasticities calculated in Page (2024), which expresses the long-term earnings effect as percent change in earnings per $1,000 of annual additional income during childhood. After adding a few additional studies, we convert these elasticities to an assumed causal share by benchmarking against our implied elasticity (estimated on the results described in the section below) and its 20 percent assumption.5 There is a wide range: the mean implied causal share is about 30 percent while the median is approximately 5 percent.

Note: this graph was updated on 4/19/2024 to correct an inflation-indexing error.

Other assumptions we make in this process include:

- Though the elasticity is for income, we use it in the context of projecting changes in earnings only, a subset of income. In other words, we assume that the wage share of income is held fixed when income rises due to increases in parent income.

- We assign a single parent income rank to each adult. In reality, families move around the income distribution year to year; children grow up in economic conditions which vary over time. This assumption can be interpreted as measuring the average income rank during childhood.

- We apply calculations at the tax unit level, not the adult level.

- Post-adjustment wages are capped at the mean of the baseline 100th percentile. That is, no one’s earnings exceed that of the highest group we project under current law.

- All children, even those growing up in high-income families, are assumed to see some nonzero benefit from additional income. This assumption contrasts with those of other researchers, who generally impose a zero-effect assumption above some income threshold to capture the idea that additional cash is more effective at improving outcomes for low-income children versus high-income children. Our rank-rank specification, however, generally limits the size of implied earnings effects for high-income children because the distance between parent income thresholds – the denominator in the expression the rank-unit size of policy effect – rises with income. Thus, our setup does embed an implicit assumption that cash assistance to children has diminishing marginal returns as it moves up the family income distribution.

- Any aggregate earnings effect will likely have both an extensive-margin component (higher labor force participation rate and/or more hours worked) and an intensive-margin component (higher wage rates). We assume that effects occur entirely at the intensive margin, an assumption that we believe to be reasonable in aggregate and that is directionally consistent with the assumptions made by Garfinkel et al. (2022).

- Some evidence suggests that parents do not view certain cash transfers as fungible with other income, and that the effects of transfers may vary with how the policy is framed (for example, Benhassine et al. 2015). Our method treats all cash as having the same impact, whether earned through work or any number of transfer programs.

- We stress that our approach does not capture the full range of potential benefits of child poverty alleviation, nor does it speak to welfare effects of transfers per se. This method reflects our narrow interest in the question of earnings and its feedback on the federal budget.

Example results

To illustrate our methodology in practice, we present results from an example counterfactual policy reform in this section. Specifically, we analyze the impact of expanding the CTC to its American Rescue Plan Act of 2021 design on a permanent basis. An approximate comparison of results with those of other researchers suggests that our approach generates conservative estimates of the long-term earnings impacts of family support policies.

Policy reform size

We model the impact of expanding the CTC to its 2021 law parameters, starting in 2026. The policy reform would make the CTC more generous across several dimensions:

- It would increase the maximum per-child value from $1,000 to $3,000 with an additional $600 for children under age 6.

- It would raise the income phaseout threshold from $110,000 to $400,000 in Adjusted Gross Income (AGI) -- $75,000 to $200,00 for non-joint returns. Before that threshold, the credit would phase down from its maximum value to $2,000 per child starting at $150,000 ($75,000).

- It would remove the earnings phase-in and remove all refundability restrictions, meaning that low-income families with little or no earnings could claim the full value of the credit.

- It would raise the maximum age for a child to be claimed for the credit to 17 from 16.

Note that we use a current-law baseline, meaning that we assume the CTC reverts to its less generous pre-Tax Cuts and Jobs Act of 2017 (TCJA) design in 2026, as is scheduled in law. Against this backdrop, the 2021 CTC design is an even larger increase in family incomes compared to its impact in 2021, before which the TCJA CTC parameters were law.

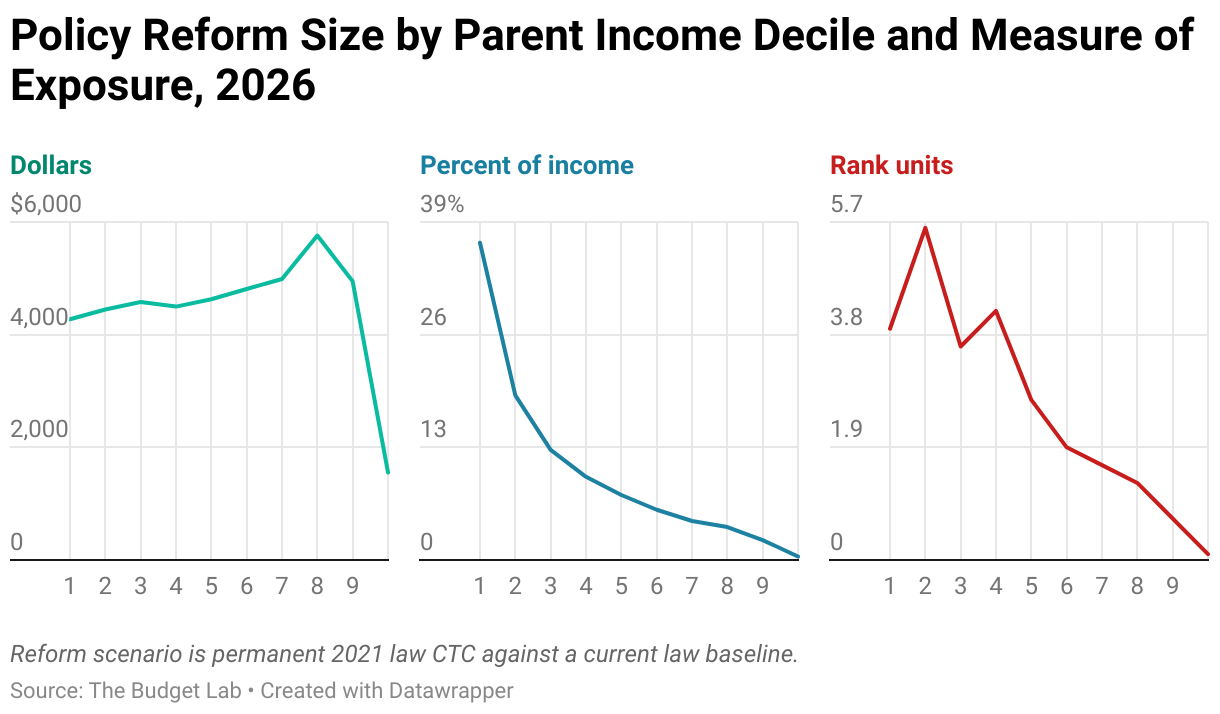

The reform delivers about $4,000 to $6,000 on average to families with children, excluding those at the very top who are phased out of the credit. Average benefits are larger for those in the 70th to 90th percentile because these groups receive little to no CTC under current law. As a share of income, the effect falls as income rises. Similarly, when expressed in parent income rank units, the reform is a much larger increase for low-income families than for high-income families. For the bottom decile, $4,000 is worth about 4 percentile rank units. For those in the top decile, it is worth less than half a rank unit. The following figure plots these measures.

Estimated effect size

The average wage earnings increase (conditional on being exposed to any increase in the CTC) rises over time following enactment because each successive birth cohort experiences more years of exposure. By 2050, the average effect stabilizes as the number of adults who only experienced a few years of CTC expansion becomes negligible. We use this year as a benchmark for calculating earnings effects for children impacted by the reform.

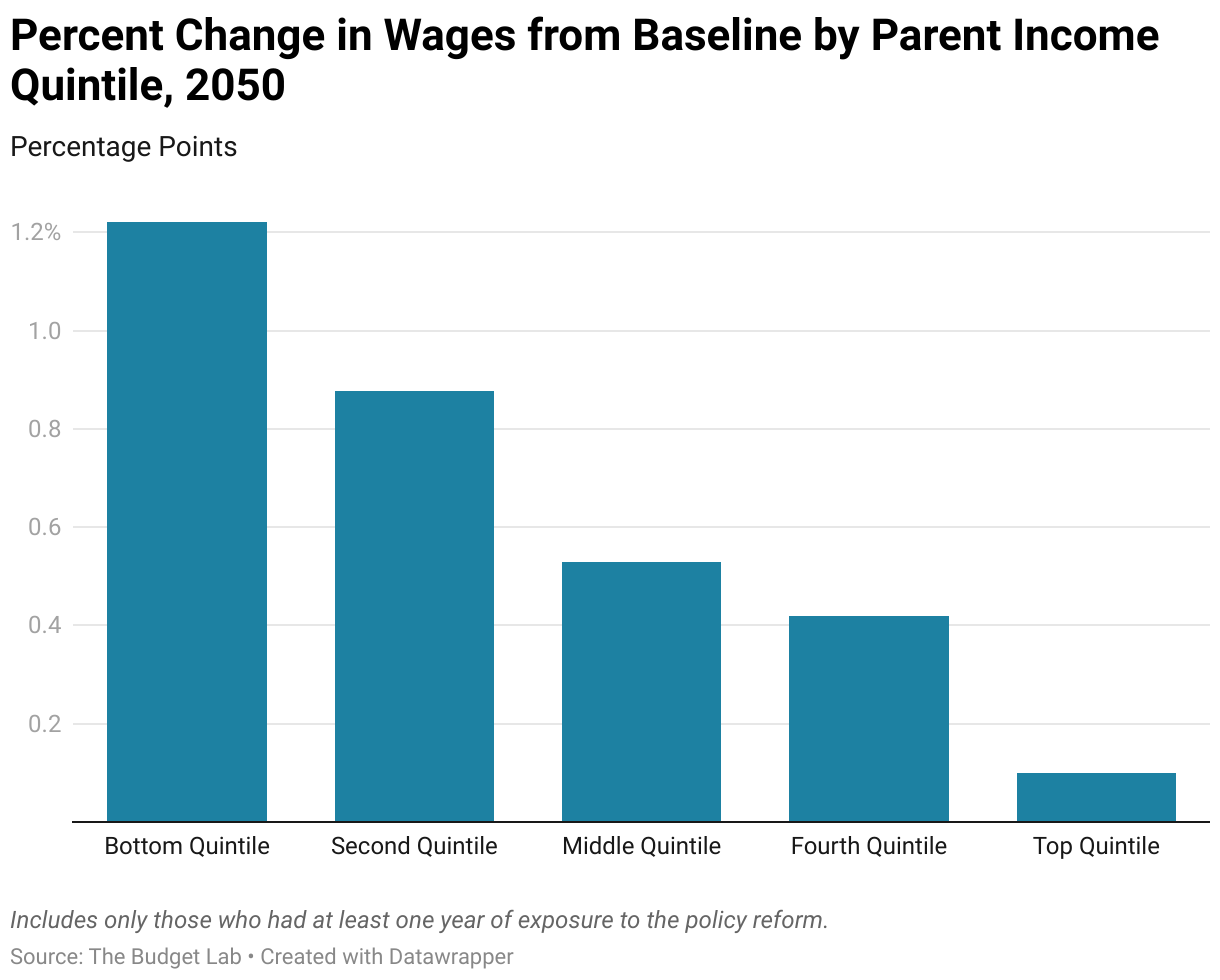

The figure below shows our projections for how the policy reform would translate to earnings, conditional on parent income.

All else equal, children who grew up in the bottom quintile would see larger impacts than those from families at the top. We estimate this group would see an increase in wages of more than 1.2 percent. Overall, the policy reform would increase the earnings of affected children by an estimated 0.6 percent on average (and approximately 0.2 percent if we weight by dollars rather than population).

How do these results compare to those of other researchers? Differences in baselines (we simulate the 2021 against current law, whereas others estimate against a current policy baseline, in which the larger TCJA CTC is law), units, and timeframes make true apples-to-apples comparisons effectively impossible. Nonetheless, we can generate a back-of-the-envelope estimate of the difference.

- Goldin et al. (2022). The authors assume a causal relationship between cash assistance and adult earnings based on the literature review from Garfinkel et al. (2022). They average the results of several papers studying the effects of programs like EITC, SNAP, and widow’s insurance, arriving at effect size of 0.63 percent increase in earnings per $1,000, assuming the effect is half as large for families making between $50,000 and $100,000 and 0 for families above $100,000. In this context, they estimate that the 2021 law design of the CTC, measured against a current policy baseline, would increase long-term wages of all affected children by 1.2 percent, with children in families with income less than $50,000 seeing a larger effect of 2.4 percent. For children of families making less than $50,000 per year, our implied effect size is 0.24 percent per $1,000. In other words, our earnings estimates are about one-third the size of theirs.

- Werner (2024). The author finds a 12 percent increase in earnings for children below 200 percent of the poverty line under a scenario in which the 2021 version of the CTC is made permanent and the effects do not diminish over time. Given the policy intervention in question is about $4,000, this result implies a 3 percent increase in earnings per $1,000. Our equivalent effect size for the group in question is 0.3 percent. The difference between estimates, then, is an order of magnitude. A difference this large is not surprising ex-ante -- the author stresses that a purely causal interpretation of their results is unwarranted and instead that the model is built on linking correlational evidence.

These comparisons suggest our approach generates conservative estimates of the long-term earnings impacts of family support policies.

Budgetary feedback effects

After the model revises its projection of earnings under the counterfactual policy reform, it recalculates tax liabilities for all tax units. This increase in earnings generates higher payroll and income taxes and, in some cases, causes outlays associated with certain refundable tax credits to fall. Because individual income taxes are progressive, the distribution of wage changes matters for the size of these indirect budget effects.

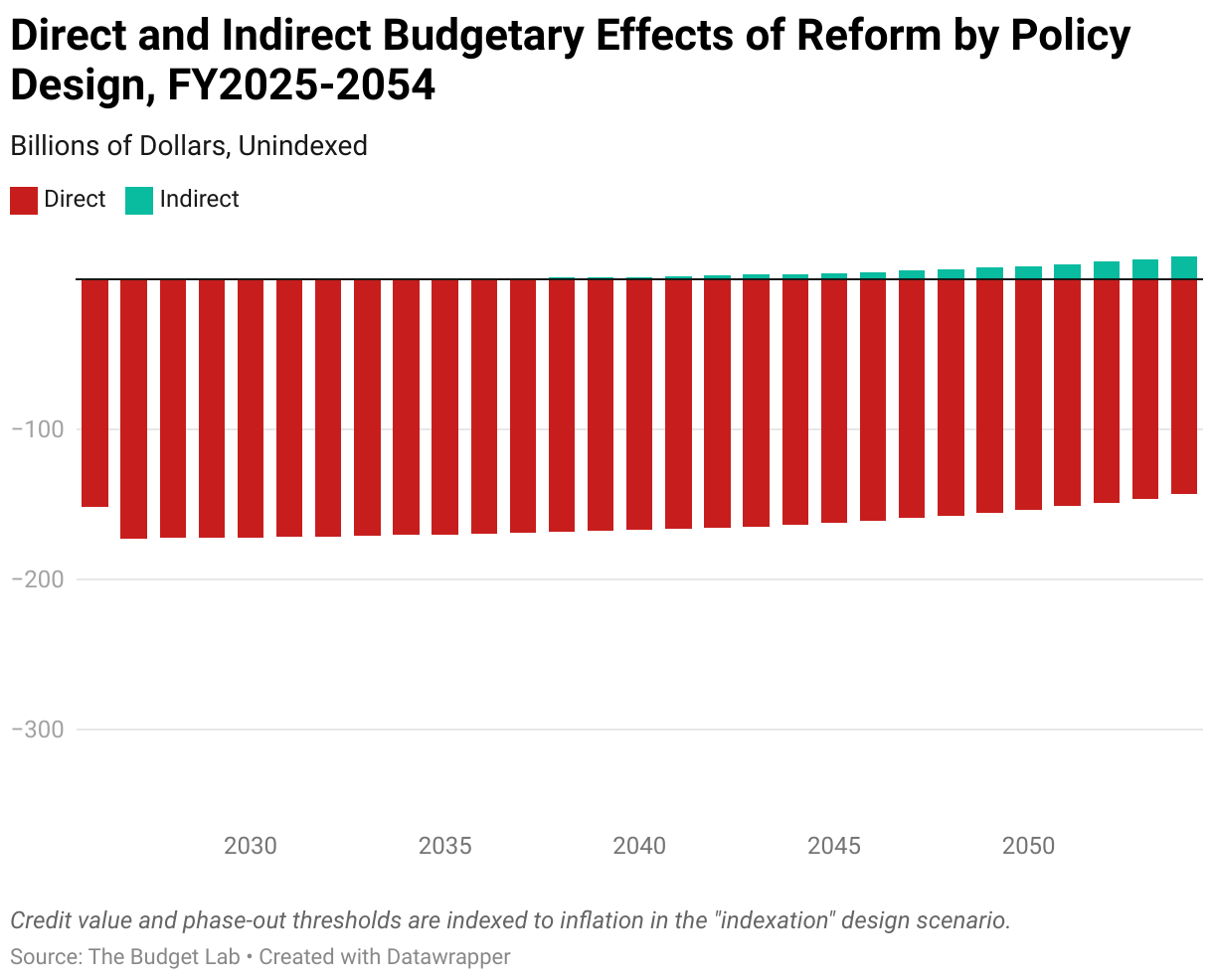

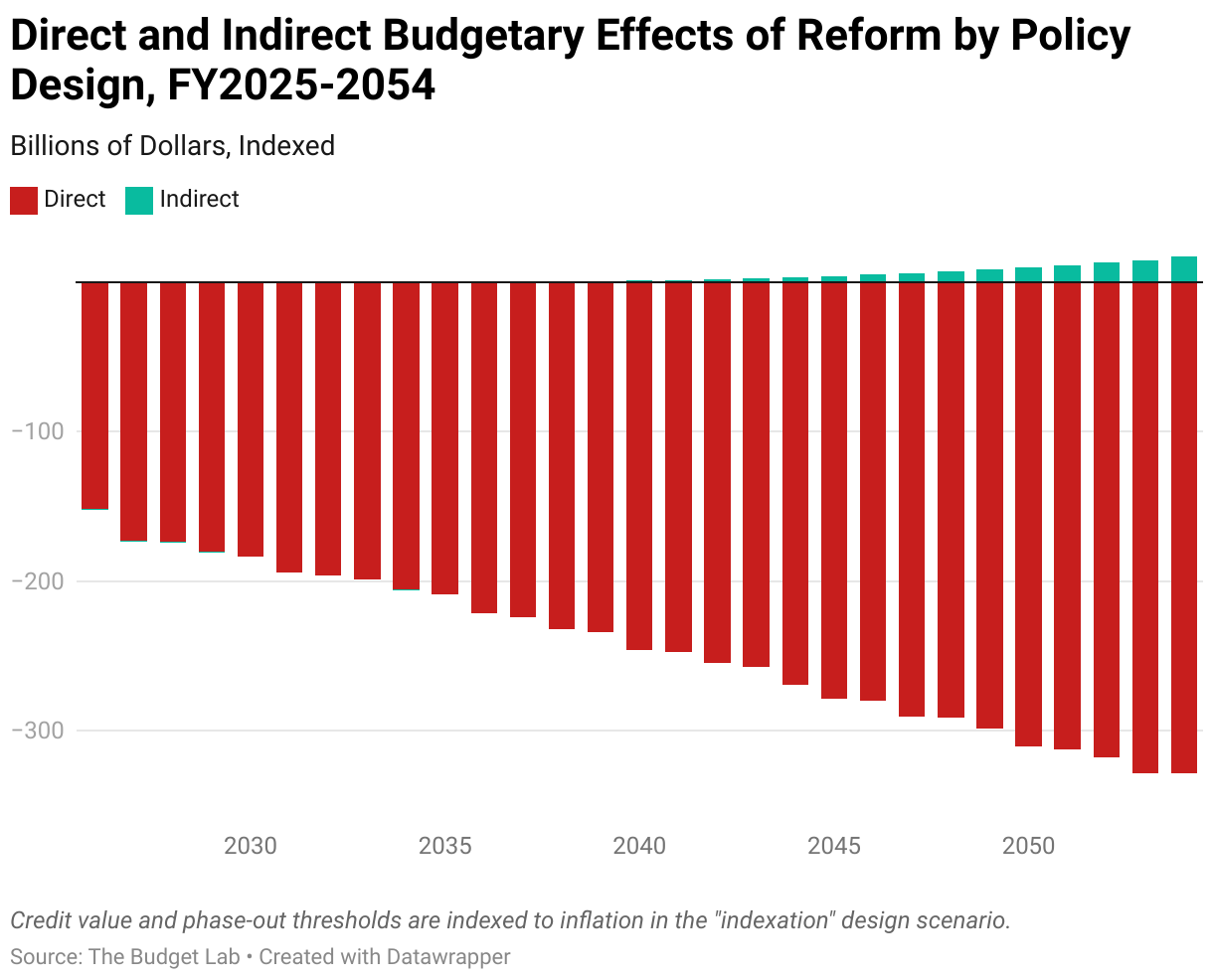

The following figure plots estimated annual budget costs through 2054, decomposing the effect into direct costs (i.e. first-order changes) and indirect changes (i.e. second-order budgetary changes attributable to higher earnings). We present results for two versions of the policy: one where parameters are not adjusted for inflation over time (as per the results above), and another which indexes the credit value and phaseout threshold to inflation.

By 2054, indirect revenues offset about 10 percent of contemporaneous direct costs of the unindexed version of the policy. It is difficult, however, to meaningfully compare concurrent outlays (which are spent on the current generation of children) with new revenues (which accrue due to policy interventions in prior generations). This is especially true of this specific policy reform, which is not indexed to inflation, meaning that its value falls in nominal terms over time due to bracket creep. An indexed version of the reform generates persistently larger direct budget costs, and as such, the indirect revenue offset share is only 5 percent.

A more complete analysis would involve running the simulation for more than 100 years, making assumption about discount rates, and expressing the indirect revenues in present value terms, allowing us to calculate a net ROI-type figure for a specific generation of children. Nonetheless, our results indicate that projected budgetary feedback from making the 2021 CTC permanent would be small but non-negligible within a reasonable time frame.

This page was most recently updated on June 26, 2024.

Footnotes

- The Social Genome Model is a joint project of the Urban Institute, Child Trends, and the Brookings Center on Children and Families.

- The data is available for download at this link, listed as “Geography of Mobility: National 100 by 100 Transition Matrix.”

- As a validation exercise for our mobility imputations, we estimate the implied IGE on our simulated data and confirm our data is consistent with the IGE estimated in Chetty et al. (2014).

- In theory, the causal share could exceed 1 – that is, the causal effect of additional parental income on child earnings could be greater than their unconditional correlation – under certain conditions. For example, if the non-income factors that are positively correlated with parent income described above have a negative impact on children’s earnings, then the correlation between the two would be smaller than the causal impact. Alternatively, if low-income parents are steeply liquidity-constrained, then providing additional cash could allow for second-order behavioral responses that generate increases in family income in excess of the cash itself, leading to even larger impacts on child earnings than the existing correlation between parental income and child earnings.

- Because most of the literature looks only at cash assistance for low-income families, we restrict the population in our elasticity calculation to the bottom 50 percent of children. The implied earnings elasticity is 0.3 percent per $1,000 (2018 dollars) of annual income during childhood.