Behavioral Responses: Capital Gains Realizations

This post is part of a broader series explaining the modeling assumptions underlying our estimates. See here for other posts on this topic.

Capital gains are taxed on a realization basis. Compared with tax on other types of income, taxpayers have more latitude to decide when – and in some cases whether – to pay capital gains tax. One implication of this treatment is that realizations are sensitive to tax rates, meaning that revenue scores for capital gains tax changes will depend on the assumed realization elasticity. Below, we describe our approach to choosing a parameter value for this elasticity.

An empirical literature spanning decades has attempted to measure the realization elasticity; see Gravelle (2021) for a broad overview.1 Historically, the Joint Committee on Taxation (JCT), Treasury’s Office of Tax Analysis (OTA), and researchers at think tanks have assumed a realization elasticity of about -0.7. This assumed degree of responsiveness implies that the revenue potential for capital gains tax rate increases is limited by taxpayer avoidance strategies.

Sarin et al. (2022) offer several arguments for why this assumed elasticity may be too large. One argument is that the share of capital gains2 relatively inelastic taxpayers has risen over time. Some taxpayers are especially sensitive to tax changes: for example, someone holding publicly traded stock in a taxable brokerage account. But others are less responsive to tax changes. These inelastic taxpayers include limited partners, receivers of carried interest, and owners of mutual funds – owners who do not directly control when asset sales occur. In addition, due to the rise of tax-deferred savings accounts, a growing share of domestic US equity is completely tax-inelastic. If the composition of capital gains has meaningfully shifted towards inelastic gains since the period used in econometric studies of the realization elasticity, then the assumed elasticity in today’s budget estimates should be lower.

In our revenue scores, we choose a parameter value for the realization elasticity based on this argument. Our approach is to take the historically assumed elasticity and adjust it to reflect compositional changes in capital gains over the last two decades. We categorize capital gains as accruing to one of two kinds of taxpayers: elastic or inelastic. Given the relative shares of elastic and inelastic asset holdings, and given an assumed overall elasticity value of –0.72, we generate an implied elasticity for these two categories using the following equation for the overall elasticity:

ε = SE ⋅ εE + SI ⋅ εI

where S are shares of assets in either the elastic (E) or inelastic (I) group and ε are the respective elasticities. This equation is simply the weighted averages of the elasticities. Setting this equation to historical shares and an estimated overall elasticity of –0.72 yields an elasticity of -0.473 for the inelastic group and -0.945 for the elastic group.

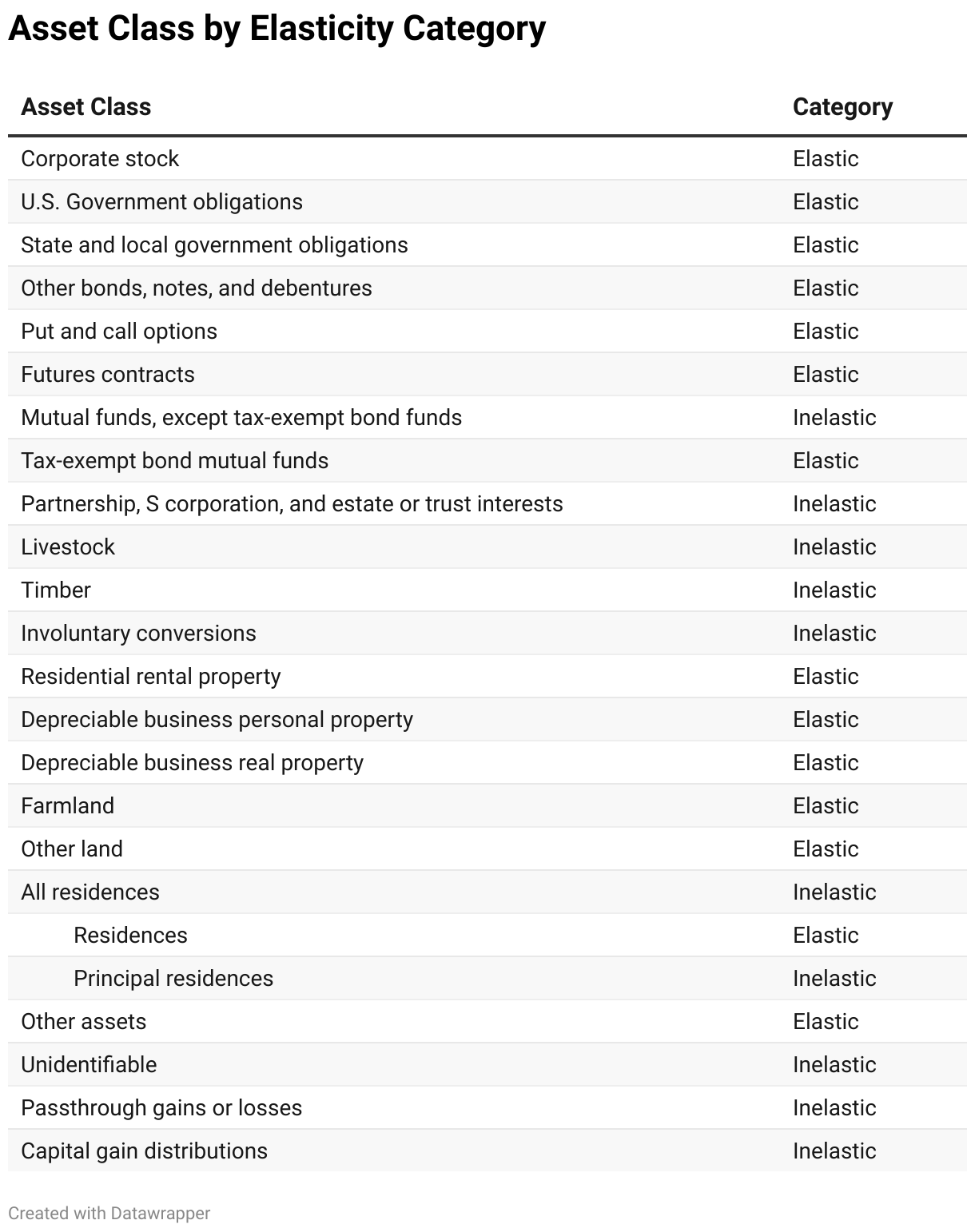

Conditional on these category-specific elasticities, setting the relative shares to those of a more recent period generates an overall elasticity of –0.62. This is the value we use in our revenue estimates and is consistent with recent empirical evidence. These calculations are based on the IRS’s Sales of Capital Assets (SOCA) data. Using this data, we find that the share of elastic assets (SE 52 percent in 1997 to just 30 percent in 2015. Correspondingly, the share of inelastic assets (IE rises from 48 percent in 1997 to 70 percent in 2015. We classify the data reported by IRS in the following way:

This page was most recently updated on June 17, 2024.

Footnotes

- Gravelle, Jane. “Capital Gains Tax Options: Behavioral Responses and Revenues.” CRS R41364, 2021.

- Natasha Sarin, Lawrence Summers, Owen Zidar and Eric Zwick. “Rethinking How We Score Capital Gains Tax Reform” Tax Policy and the Economy Volume 36, Issue 1. 2022. Pages 1-33. https://doi.org/10.1086/718949