Child Tax Credit: Options for Reform

Key Takeaways

-

The Child Tax Credit (CTC), which reduces tax liability for most parents and is designed to encourage work, is scheduled to be cut at the end of 2025. In this context, we analyze four CTC reform proposals with varying objectives for work incentives, poverty alleviation, and tax simplification.

-

The phase-in and phase-out ranges are key policy parameters: a quicker (or elimination of the) phase-in benefits the lowest earners, while a longer phase-out benefits the middle class.

-

We project that some proposals would increase employment, and others would reduce it, in the range of a -0.1 percent to 0.3 percent change in the U.S. labor force.

-

Under strong assumptions, including that cash transfer receipt causes 20 percent of the gap in adult earnings outcomes between high-income children and low-income children, our modeling estimates that average wages for people in 2050 who were exposed to a full 18 years of the most generous reform option would be more than 0.6 percent higher compared to current law (about $200 in additional earnings every year, adjusted to current price levels). For children growing up in bottom-quintile families, this effect is more than 1 percent (about $300 per year).

-

All reform options would have small effects on macroeconomic aggregates such as real gross domestic product (GDP), inflation, and interest rates, although including a pay-for improves the long-run growth and budgetary outlook.

Summary

Most of the 2017 Tax Cuts and Jobs Act’s (TCJA’s) individual tax provisions, including its CTC expansion, are scheduled to sunset at the end of 2025. Beginning in 2026, the maximum CTC value will fall from $2,000 to $1,000 and be limited to a narrower set of taxpayers. This expiration may renew discussion of reform options for the CTC.

This report informs that discussion by exploring four reform options.

- Current Policy is a straightforward extension of the current CTC design, which was first enacted under the TCJA and is scheduled to expire at the end of 2025.

- The Family Security Act 2.0 (“FSA”) is a proposal by Senators Romney, Burr, and Daines. It would consolidate several child-related provisions in the tax code and expand the CTC, especially for parents of young children, in a way that strengthens the credit’s incentive for parents to participate in the labor force.

- 2021 Law would revert CTC parameters to those of 2021, when the American Rescue Plan Act (ARPA) temporarily increased the maximum credit value and removed all earnings requirements.

- Edelberg-Kearney, a proposal by Wendy Edelberg and Melissa Kearney, is designed to maintain current-policy work incentives while providing some amount of relief for those with no earnings.

The FSA is unique among the four reform options in that it is not deficit-financed: the FSA expands the CTC while curtailing the Child and Dependent Care Tax Credit, Earned Income Tax Credit, and state and local tax deduction. It can be challenging to compare the distributional impacts of paid-for versus unpaid-for reforms, since deficits are, by convention, not distributed. As a result, we present estimates of the FSA with its pay-fors (“Full FSA”) and without (“CTC FSA”).

We estimate that extending Current Policy would increase the primary deficit by approximately 0.5 percent of GDP in each of the next ten years relative to current law. The three reform proposals (excluding the Full FSA) have similar budgetary impacts: each would increase the primary deficit by approximately 1 percent of GDP in each subsequent year relative to current law. By contrast, the Full FSA would reduce the primary deficit in each subsequent year by approximately 0.5 percent of GDP.

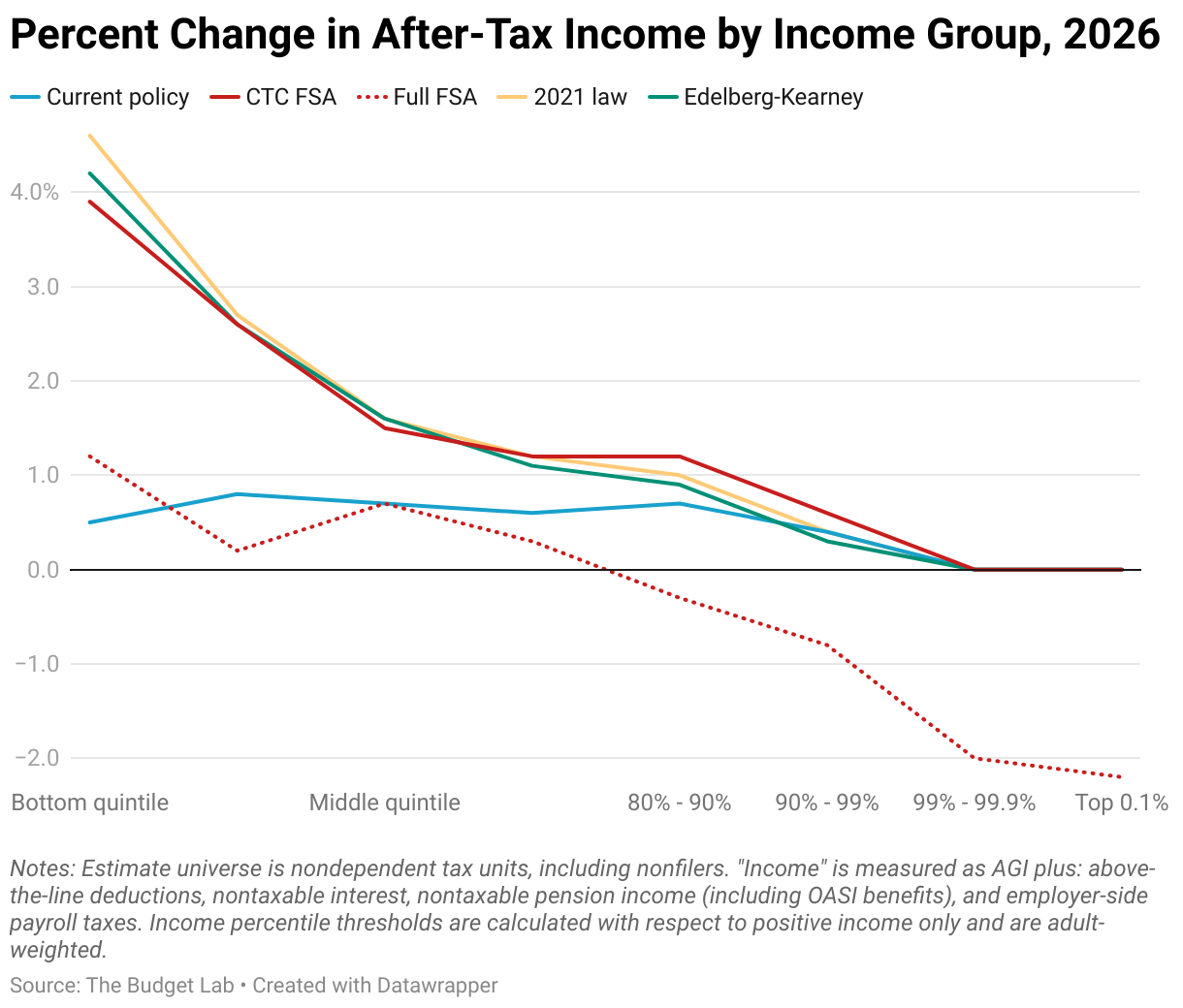

Apart from Current Policy and Full FSA, the CTC proposals have relatively similar distributional impacts. In particular, each of these remaining proposals would increase bottom quintile after-tax income by approximately four percent relative to current policy, with smaller percentage increases at middle incomes. We follow convention in not distributing those proposals’ deficit increases, only considering their direct distributional effects. The Full FSA would increase after-tax incomes in the bottom four quintiles relative to current law, reduce them in the second quintile relative to current policy, and reduce them in the top two quintiles relative to current law and policy.

Despite having broadly similar distributional impacts, each proposal contains design differences that affect work incentives in different ways and lead to modest changes in overall employment. We find that under the FSA reforms, Current Policy, and Edelberg-Kearney 100,000-150,000 fewer people would decide to work, while under the 2021 Law, 200,000 fewer people would decide to work.

Long-run impacts of child-focused policies can affect long-run budgetary impacts. We make several strong assumptions to provide an initial modeling analysis of the long-run earnings impacts and associated tax revenue feedback of the CTC. Existing research provides a large band of estimates of the causal share of cross-sectional child-parent income relationship, ranging from 0 percent to above 100 percent. We assume that 20 percent of the existing relationship between parent income and child income is causal: if the CTC moves a child from parent income X to parent income Y, we assume that the child’s earnings outcome on average will be 20 percent of the way towards the outcomes of children who currently have parents with income Y. In this preliminary analysis, we assume that this 20 percent figure is net of general equilibrium labor market adjustments, and we make no wage adjustments due to capital crowd-out from higher interest rates under a deficit-financed CTC, both of which tend to overestimate long-run impacts.

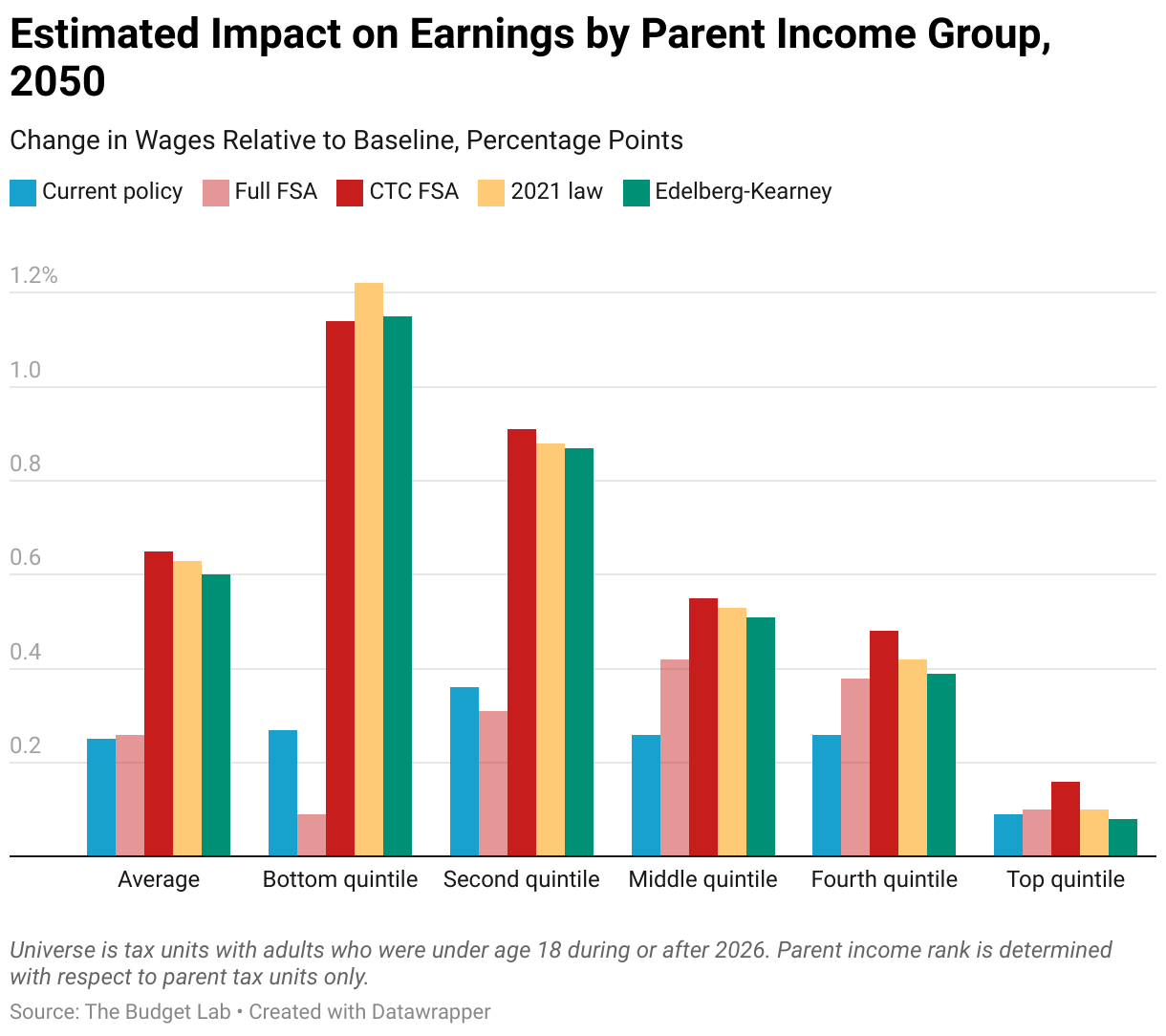

The figure below displays the estimated change in wages in 2050 among adults who would have been exposed to a full 18 years of each reform during childhood, overall and by parent income quintile.

On average, we project that Current Policy raises the next generation’s wages by 0.2 percent. The percentage gains are roughly equal across parent income levels, with top-quintile children enjoying the smallest percentage gains primarily because the CTC is a smaller percentage of top incomes. The CTC FSA, 2021 law, and Edelberg-Kearney each yield 0.6 percent average wage increases, with percent wage gains concentrated at lower quintiles.

The Full FSA yields average wage increases similar to Current Policy, with wage increases concentrated at middle incomes that avoid both the EITC reductions and the SALT effective tax increases. Note that children growing up in the top quintile benefit from all policies including the Full FSA despite its net tax increase on top quintile households, because the Full FSA redistributes within the top quintile from childless households to households with children.

Programs that yield long-run benefits may nevertheless fail a cost-benefit analysis. A full cost-benefit analysis of the CTC requires further modeling, including discounting next-generation benefits to the present and comparing them to up-front costs. Moreover, we emphasize that given that the Full FSA is paid for while the others are not, it is hard to compare the long-term impacts of children of different CTC proposals with different pay-for assumptions.

Our macroeconomic results (which do not include the employment and earnings impacts discussed above) show relatively small impacts from these proposals (though, given the modest effects of all the options we analyzed, the employment channel is unlikely to significantly change our macroeconomic simulations).

All macroeconomic forecasts and estimated effect sizes are subject to uncertainty, particularly in the long term and in future generations. Furthermore, since the magnitude of policy effects is in part conditional on macroeconomic conditions, the uncertainties around each effect interact with one another. Budget scoring requires educated assumptions and guesses. In addition, estimates involving future earnings outcomes rely on past research informed by models of the historical labor market. However, the labor market may look considerably different in the decades to come than. We do not provide confidence intervals throughout this report, but we do attempt to communicate where we are more or less certain in our work.

Background

The Child Tax Credit (CTC) provides a flat dollar amount of income tax relief for most parents. Introduced in 1997 as a modest nonrefundable credit, the CTC has evolved into a substantial part of the tax code through subsequent rounds of legislation expanding the credit.

Historically, the CTC has served several purposes:

- Horizontal equity is the idea that taxpayers with similar resources should pay similar amounts in tax. The CTC promotes horizonal equity by adjusting tax burdens to reflect the fact that families with children have fewer resources than those without children.

- Vertical equity is the principle that tax liability should rise with income. As a share of income, the CTC delivers larger benefits to middle-income families than it does for high-income families.

- Work incentives are a key part of the CTC’s design. The credit phases in with earnings, reducing marginal tax rates for low-income workers and thus encouraging workers to join and stay in the labor force.

Crucially, the exact mix of these goals has varied with the credit’s design and the broader context of the tax code. For example, the Tax Cuts and Jobs Act (TCJA) both expanded the CTC and eliminated the deduction for dependent exemptions with the goal of consolidating child-related benefits in the tax code – an instance of moving towards horizontal equity. More recently, the American Rescue Plan Act (ARPA) moved towards greater vertical equity by temporarily allowing nonworking parents to claim the CTC. These episodes underscore the importance of analyzing potential CTC reforms within the broader context of the tax code.

This report proceeds by viewing reform options through four analytical lenses.1

- Budgetary: By how much would each reform affect government budgets over the next three decades?

- Distributional: How much do the benefits and costs of each reform vary with income and age?

- Microeconomic: To what extent does each reform induce parents to enter or exit the workforce? Can we expect these reforms to affect future economic outcomes for today’s children?

- Macroeconomic: How would broader economic indicators like gross domestic product (GDP), inflation, and interest rates change under each option – and to what extent do these outcomes depend on the Federal Reserve’s actions?

Reform Options

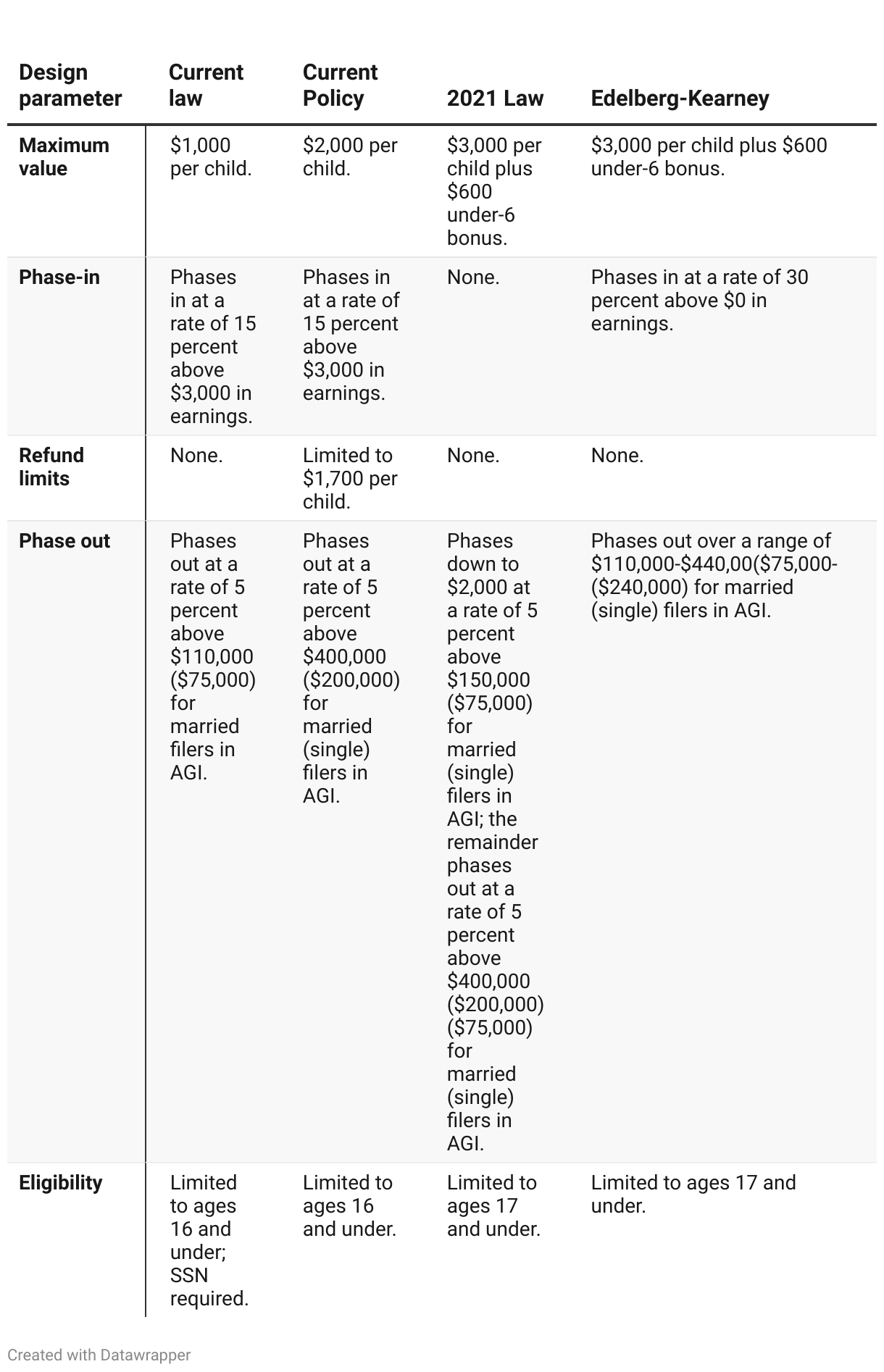

The table below summarizes major CTC design parameters across each proposed reform.

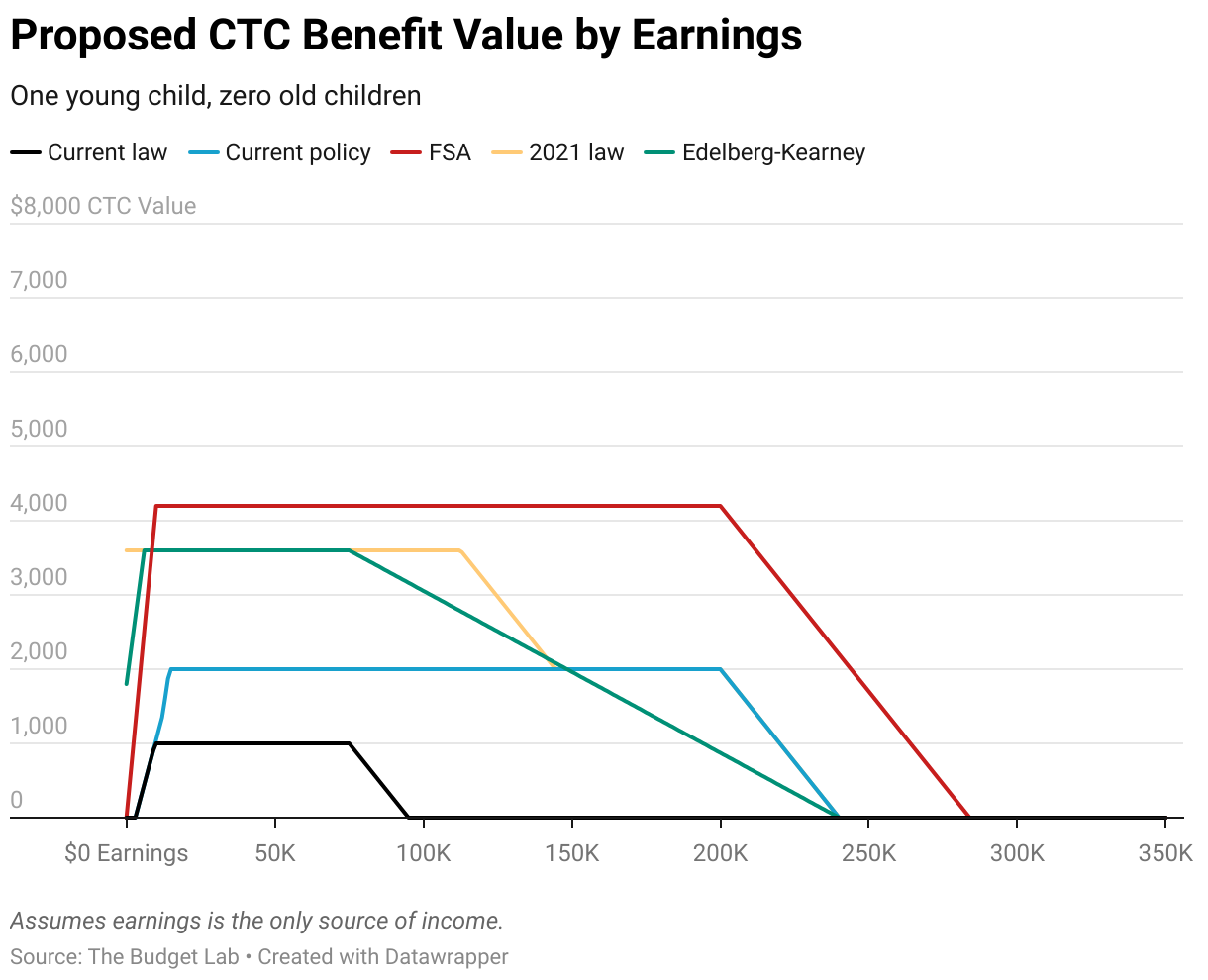

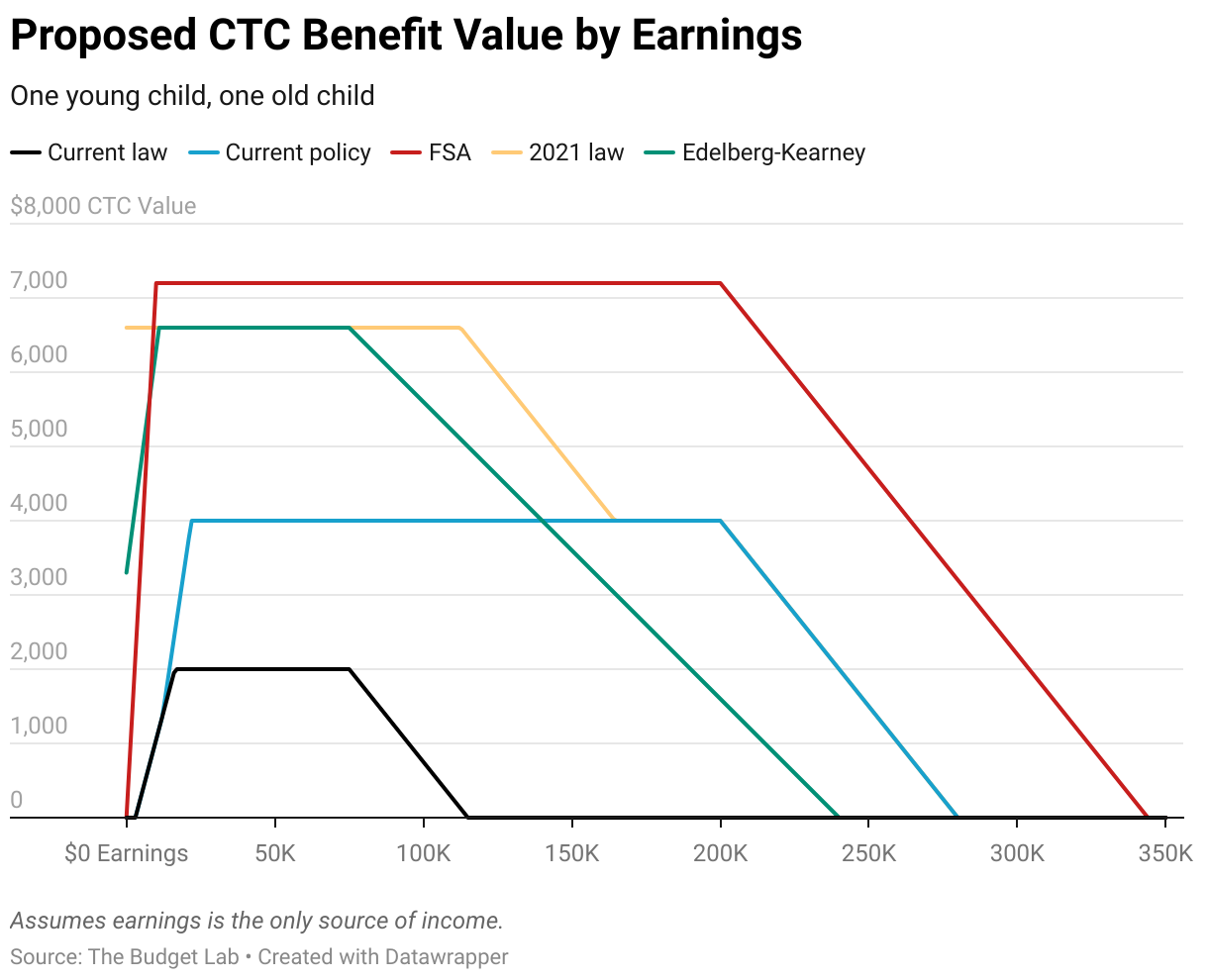

The figure below illustrates how CTC structure would vary with each reform. Tax credits that phase in and out with earnings can be visualized as a trapezoidal figure: the maximum value is represented by the plateau, and the phase-in and phase-out are represented by the left and right edges, respectively. The steeper the slope of an edge, the faster the phase-in or phase-out.

On a per-young child basis, the FSA offers the most generous CTC for families with at least $10K in earnings. For families with no income, the 2021 Law is most generous: it has no phase-in, as reflected by the y-axis intercept being equal to the maximum credit value. The Edelberg-Kearney option represents a middle ground – half of the credit is available at $0 of earnings, with the remaining value phasing in over a range of earnings.

Below, we describe each illustrative reform in detail. Reforms are characterized along four major design dimensions: the per-child maximum credit value, rules related to refundability and phase-in among low-income earners, phase-out rules, and child eligibility. In all scenarios, the current-law $500 credit for other dependents (adults and nonqualifying children) is made permanent. Each scenario assumes the proposed law would go into effect starting in tax year 2026.

Family Security Act 2.0

This reform option aims to simplify the tax code’s treatment of children. It expands the benefit to young children while also strengthening work incentives.

- Maximum value. The maximum amount would be raised to $3,000 per child with an additional $1,200 for each child under age 6.

- Phase-in and refundability. The current-law CTC phases in at a rate of 15 percent for each dollar of earnings. This structure means that a family with two children must make more money to claim the full value of the credit compared with a one-child family. Under this proposal, the entire credit to which a family is eligible would instead phase in over the first $10,000 in earnings. This design means that the phase-in rate rises with the number of children.

- Phase-out. The proposal would retain the current-policy phase-out parameters: 5 percent above $400,000 ($200,000 for non-joint filers) in adjusted gross income (AGI).

- Child eligibility. Under this option, the TCJA-established requirement that a Social Security number (SSN) is required for qualification would be made permanent (rather than expire at the end of 2025 as under current law). The maximum age would be increased from 16 to 17.

- Benefit consolidation. Under this option, the Head of Household (HOH) filing status, which provides preferential tax treatment to certain unmarried parents, would be eliminated. It would also eliminate the Child and Dependent Care Tax Credit (CDCTC), a tax credit which offsets certain childcare costs. The reform also proposes cuts to the Earned Income Tax Credit (EITC). Under current law, the maximum EITC benefit scales with the number of qualifying children, up to three; the proposal would reduce the maximum benefit from $6,600 to $2,000 for childless joint returns and from $7,430 to $3,000 for filers with children. Phase-in and phase-out rates would change, and the current-law EITC marriage penalty would be eliminated.

- SALT deduction. The Family Security Act 2.0 proposes to eliminate the deduction for state and local taxes (“SALT”), which is capped at $10,000 through 2025 and uncapped thereafter.

Note that throughout this report, we often consider the Family Security Act 2.0’s CTC provision separately and then also consider its full set of proposed changes, as other proposals do not contain pay-fors, and we wish to provide some apples-to-apples comparisons.

Current Policy

The first reform option would permanently extend the CTC’s design under current policy (the design under the TCJA). This reform would cement the tax code’s current approach to the CTC and in doing so prevent the credit from reverting in 2026.

- Maximum value. The maximum CTC value would be $2,000 per child.

- Phase-in and refundability. For filers without sufficient tax liability against which to claim the CTC, a partial credit would be available. This refundable portion would be limited to the lesser of (1) 15 percent of earnings in excess of $2,500 or (2) $1,700 per child (indexed to inflation but limited to $2,000). In other words, the credit would phase in at a rate of 15 percent.

- Phase-out. The current-policy AGI thresholds of $400,000 for joint returns and $200,000 for others (above which the credit value phases out at a rate of 5 percent) would be made permanent.

- Child eligibility. This option would make permanent the current-policy SSN requirement while maintaining the age limit at 16.

2021 Law

This reform option would make permanent most CTC design parameters temporarily enacted as part of the ARPA in 2021. In addition to making the CTC more generous by increasing the maximum credit value, this reform expands benefits to low- or no-income families for whom current law provides no benefits. It does so by removing the earnings phase-in entirely and allowing the full value of the credit to be claimed regardless of income tax liability.

- Maximum value. The maximum amount would be increased to $3,000 per child, with an additional $600 for children under age 6.

- Phase-in and refundability. The phase-in would be eliminated, and the credit would be made fully refundable: in other words, the credit’s full value would be made available to all low- and middle-income parents regardless of how much they earn or owe in taxes.

- Phase-out. The CTC would phase out over two separate ranges. First, the credit would be reduced by 5 cents for every dollar over $150,000 in AGI for joint returns ($75,000 single, $112,500 head of households) until it reaches $2,000. It would remain at that level until AGI reaches $400,000 ($200,000 for non-joint returns) when it begins to phase down to zero, again at a rate of 5 percent.

- Child eligibility. This option would allow the SSN requirement to expire as under current law. The age limit would be increased to 17.

Note that the ARPA also made changes to the administration of the CTC in 2021, allowing parents to receive the credit in ongoing monthly installments rather than as a lump sum refund during tax-filing season. As a related matter, it allowed some taxpayers to use AGI from prior years when determining eligibility. These administrative changes shift the timing of government outlays and receipts rather than materially affecting tax liabilities. Because the focus of this brief is on how CTC design affects liability rather than receipts, the 2021 Law scenario modeled in this report does not reflect these administrative changes.

Edelberg-Kearney

This reform option is designed to expand the CTC in a way that provides relief to low-income families while retaining the CTC’s work incentives. It would do so by allowing non-earners to claim up to half of the maximum CTC value while increasing the rate at which it phases in. The reform also includes a broader and slower phase-out structure.

- Maximum amount. The maximum amount would be increased to $3,000 per child with an additional $600 for children under 6.

- Phase-in and refundability. Half of the credit’s full value would be available at $0 of earnings. The remainder of the credit would phase in at a rate of 30 percent of earnings, double the current-law rate of 15 percent. No other restrictions would apply (e.g., additional refund limits as under current policy).

- Phase-out. This reform option would retain the current-law AGI phase-out threshold of $110,000 ($75,000 for non-joint filers). Above this threshold, the credit value would phase down until it reaches $0 at $440,000 ($240,000 single and head of household) of AGI. That is, the design utilizes a range-based phase-out structure, in which the effective phase-out rate depends on the number of children claimed.

- Child eligibility. Under this option, there would be no SSN requirement, and the maximum age would be increased to 17.

Footnotes

- We do not calculate differences in the time burden associated with tax filing across the reforms. We feel the differences would be negligible. For how the Budget Lab constructs taxpayer time burden see here.