Clausing-Sarin: Conventional Revenue Score

Key Takeaways

-

The Clausing-Sarin reform cuts average annual primary deficits by nearly two-thirds. It raises 1.3 percentage points of GDP of new revenues on average over the decade.

-

The proposal would raise a net $4.3 trillion over the budget window, with more substantial savings in subsequent years.

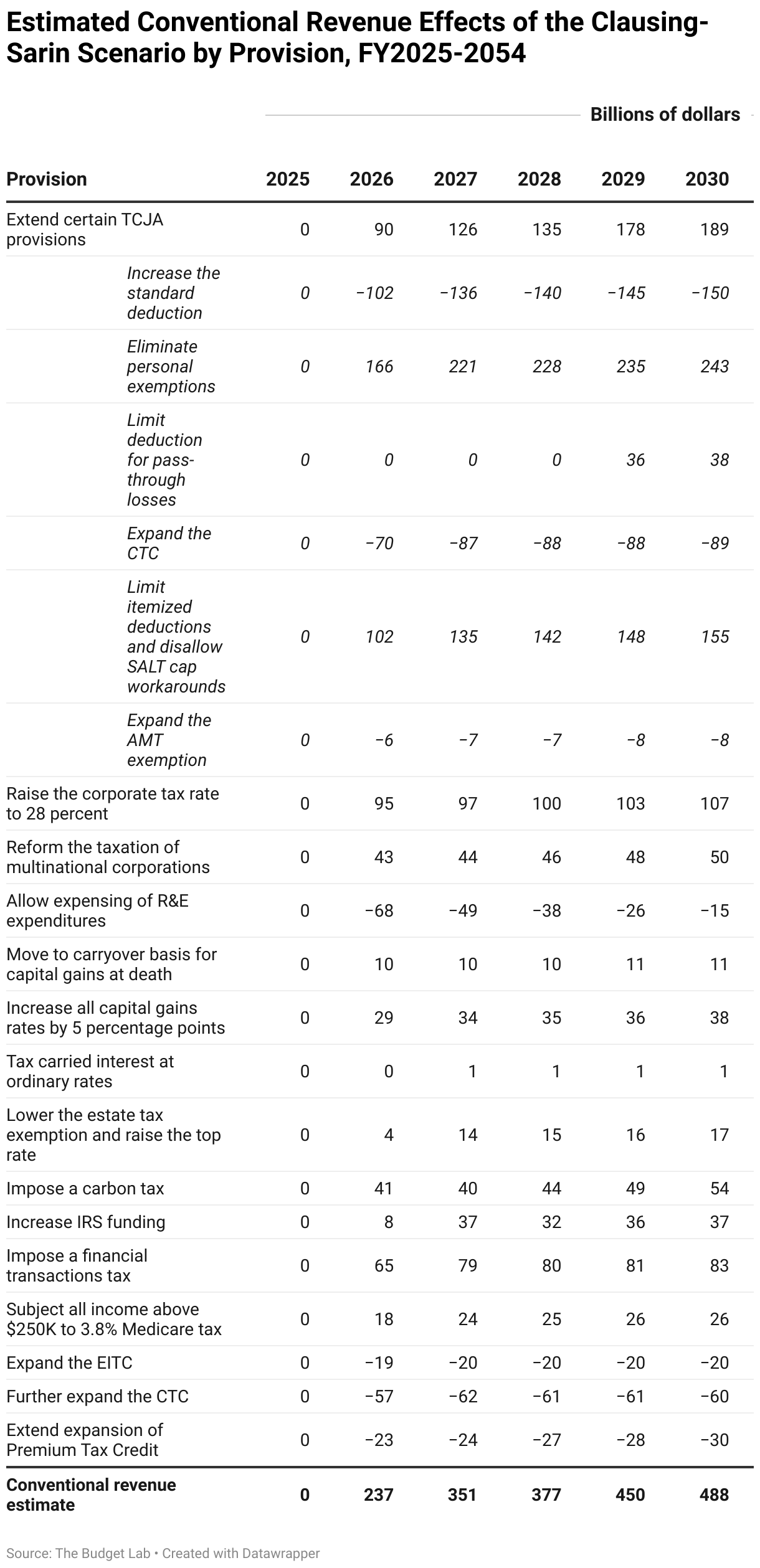

Unlike the Full and Partial Extension scenarios, the Clausing-Sarin reform is designed to be a net revenue-raising package. At the provision level, however, there is considerable variation in estimated budget effects.

Deficit reduction in the second and third decades is considerably higher than that of the first decade, as some revenue-raising provisions (the carbon tax and IRS funding) are fully phased in only after the first decade, and the move to R&E expensing represents a one-time up-front cost.

Notably, the TCJA component of the reform is a substantial revenue raiser relative to current law. The package raises $1.6 trillion by extending many expiring TCJA provisions but allowing tax rates to revert, the QBI deduction to expire, and the estate tax exemption to rise. It also raises substantial revenue from disallowing state-level SALT cap workarounds, a policy change that would require legislation or new IRS regulations.

Our findings suggest that TCJA extension could raise revenue, rather than lose revenue, if all provisions except for the full rate cuts are extended.