Depreciation 101

Economic depreciation is the decline in the value of the services produced by a capital asset. In other words, it accounts for the fact that we only expect capital assets to be useful for so long. The decline is due to physical loss, changing demand for the services the asset provides, or the asset becoming obsolete. Users of capital assets model the value of the capital asset as the present value of the flow of services the asset produces. Tax deductions for depreciation allow users of capital to recover the cost of the asset over the useful life of the asset. Policymakers may want to match the cost associated with an asset to the use of the asset over time. A more commonly cited reason for providing tax deductions for depreciation is that policymakers may want to provide incentives to increase investment. Those incentives for investment may be desired for time-insensitive reasons (capital deepening is a driver of long-run economic growth) and for countercyclical reasons (in a recession, businesses may face a liquidity crunch and thus neglect to make economically good investments that would help spur the economy).

How do deductions for depreciation work?

Businesses pay tax on the difference between revenues and costs—what we call “net income” or “profits.” But it’s not always clear how to define “costs” or what their tax treatment should be.

For current expenses, like wages paid or rent, there’s little ambiguity. These expenses are simply outflows of money from the business, so the tax code allows for an immediate deduction of these costs when calculating net income.

Things are more complicated for capital expenses. When a firm buys a capital good, like a truck or a factory or a piece of manufacturing equipment, it’s merely swapping one asset (money) for another (equipment). From an economic perspective, the cost of that purchase is not incurred when the money is spent but rather when the asset depreciates—that is, when it loses value due to physical wear and tear or obsolescence. Some assets, like computers, depreciate quickly; others, like buildings, slowly lose value over decades. The tax code handles this by assigning a depreciation schedule to each type of asset. When a firm invests in a capital good, it must deduct the costs of that purchase according to the specified depreciation schedule.

The design of these schedules is an important dimension of how businesses are taxed. Economists have a well-established framework for understanding how depreciation policy affects tax burdens based on the time value of money (the idea that as long interest rates are positive, a dollar today is worth more than a dollar tomorrow). Businesses prefer tax savings sooner rather than later, so a faster depreciation schedule is more generous to them than a slower depreciation schedule. In other words, faster depreciation schedules result in lower tax burdens on certain returns from new investments (and thus lower tax burdens on corporations).

By changing depreciation schedules, lawmakers affect investment incentives and change the timing of tax revenues. For instance, “bonus” depreciation is extra first-year depreciation allowance that allows taxpayers to deduct additional cost of assets beyond normal allowances. It is often described as a mechanism to increase investment and was first signed into law as part of the Job Creation and Worker Assistance Act of 2002 in reaction to the recession of 2001. Since 2002, it has been in place every year except for the years 2005-2007.

There is no one “correct” way to design depreciation schedules. Rather, depreciation schedules reflect policymakers’ goals for the tax base (for example, whether it taxes income or consumption), the macroeconomy, and the budget.

Timing of Depreciation Deductions

The time value of money dictates that firms prefer deductions now rather than later. Firms are allowed a schedule of nominal deductions over time, but those deductions lose value due to inflation and opportunity cost. For example, using an 8 percent discount rate, the present value of a five-year straight-line depreciation schedule for $100 of investment—a five-year series of $20 deductions—is about $86. (Of course, the converse is true for the government from a revenue perspective: revenue now is more valuable than revenue later.)

This means that all else equal, faster depreciation schedules allow firms to recover a higher fraction of their initial investment costs in present value terms—and thus reduce the effective tax rate on those investments. The closer this fraction is to 1, the better for the taxpayer since they are receiving the full benefit of depreciation deductions. In the case of full expensing and neutral cost recovery, this fraction is equal to 1 by design. Full expensing achieves this by eliminating cost recovery altogether and treating all costs as immediately deductible while neutral cost recovery achieves this by indexing depreciation deduction to an interest rate such that businesses receive the full present value in deductions. This fraction is less than 1 for all other depreciation policies. We estimate that in 2027, when bonus depreciation is phased out under current law, firms will recover an economy-wide average of 79 percent of investment expenses. Changes to depreciation policy, then, have long-run economic effects by impacting after-tax investment returns and thus capital accumulation and growth.

Temporary bonus depreciation has also been used as a countercyclical policy tool in the past, most notably during the Great Recession. The idea is that if the provision is temporary, it will have a greater, but more transitory effect than a permanent provision. The temporary version increases the amount of investment and potentially moves future investment forward. A permanent provision may increase the amount of investment but there is no incentive to move future investment forward. Businesses may also face liquidity issues, so shifting tax payments from now to later years can be understood as a form of lending to businesses when private sector lending collapses. There are limitations though. It is possible that firms have little or no taxable income during economic slowdowns and therefore cannot benefit from the additional allowances. This latter situation is a partial explanation for why only 60 percent of eligible investment took advantage of the initial bonus depreciation provisions.1

Taxpayers apply their depreciation deductions against their income to calculate taxable income. For some businesses, these deductions put them in a loss position. This tax situation is called a Net Operating Loss (NOL) and occurs when a taxpayer’s allowable deductions exceed its taxable income. If a taxpayer with an NOL makes an investment, they would receive no immediate benefit. These NOLs can be used to offset taxable income in future years ensuring some benefit from the depreciation deductions.2

However, in a tax system where carryforwards are allowed the presence of NOLs limits the usefulness of depreciation policy. As firms carry their NOLs forward, the amount of taxable income is lowered. The lower the taxable income, the less any accelerated depreciation policy can offset and therefore, have little effect on firms’ cash flow and subsequently, incentive to invest. These policies may affect the timing and amount of investment. But only if they are of value to the taxpayer by reducing tax liability. The economic literature has found empirically that the 2002 100 percent bonus provisions increased investment between 10 and 18 percent while 179 special depreciation provisions had a considerably smaller (~2%) effect.3

Budgetary Dynamics of Depreciation

All accelerated depreciation policies come with increased cost in the near term. The expectation is that a portion of the cost is recovered in future years as taxpayers trade the near-term benefit for higher future taxes. This fact is an important consideration for lawmakers. The TCJA was passed as part of reconciliation and was limited by a maximum deficit increase of $1.5 trillion. As such, lawmakers adopted this provision as temporary in favor of other permanent policies. Temporary versions of accelerated depreciation that end within the government budget window necessarily cost less than permanent versions within the budget window. This relationship holds as some depreciation deductions are moved forward into the window and are not recovered until after the window.

Changes in depreciation policies necessarily change the timing of government revenues. For any asset that is depreciated, there are corresponding deductions over the life of the asset. For a 4-year lived asset, this means the government revenues are reduced by the full amount of the deductions in four years. In any year t, government revenues are reduced by the amount of depreciation deductions used to offset taxable income in that year. Those deductions are generated by investments from year t as well as investments put into place in previous years.

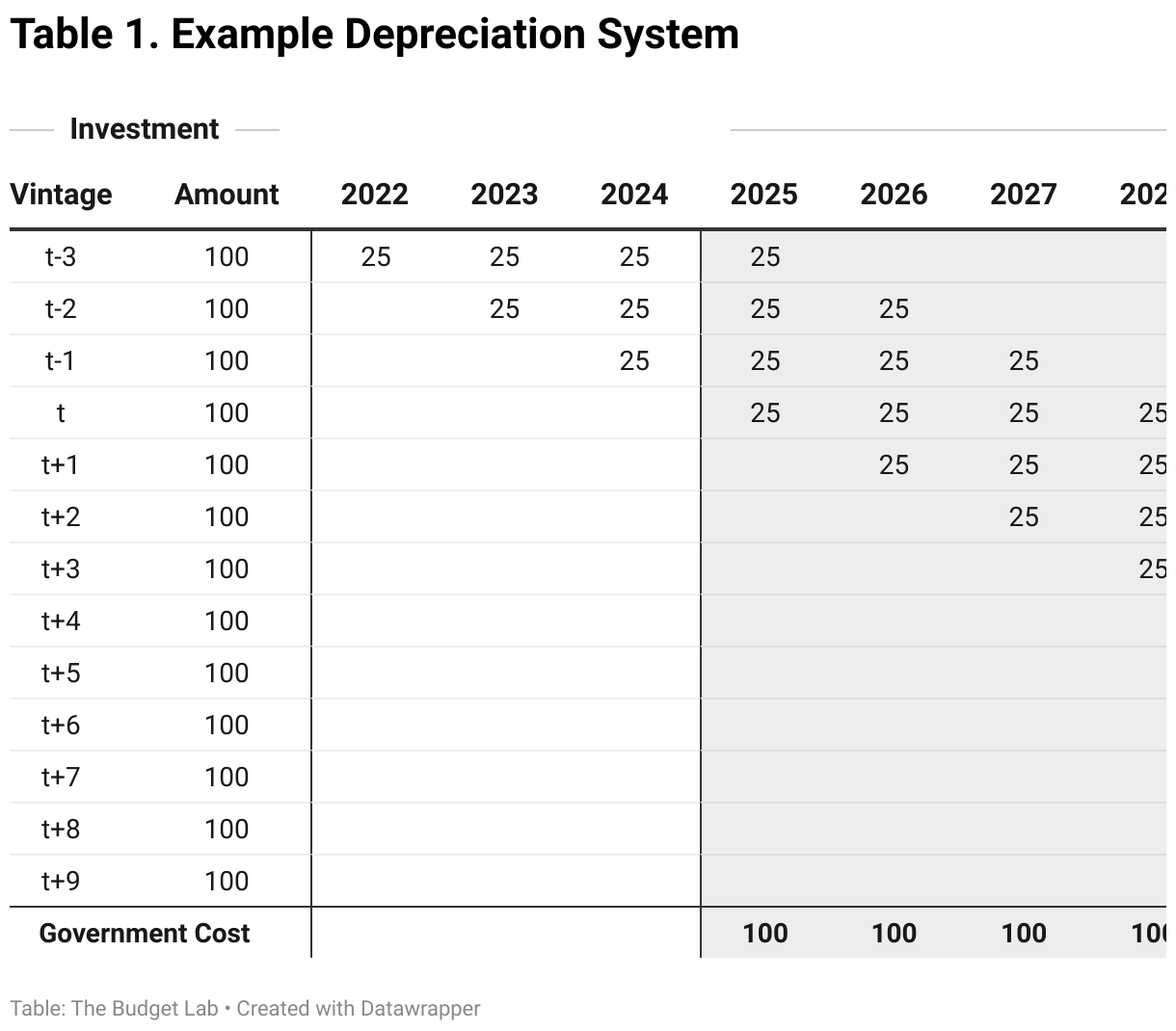

Consider a tax system that only has 4-year lived assets and straight-line depreciation. In year t, depreciation deductions are generated by new investments in year t as well as ‘old’ investment from year t-1, t-2, and t-3. In year t+1, depreciation deductions are generated by new investments in year t as well as ‘old’ investment from year t, t-1, and t-2. Table 1 illustrates this depreciation system with $100 worth of investment in each year. The government cost is $100 in each year.

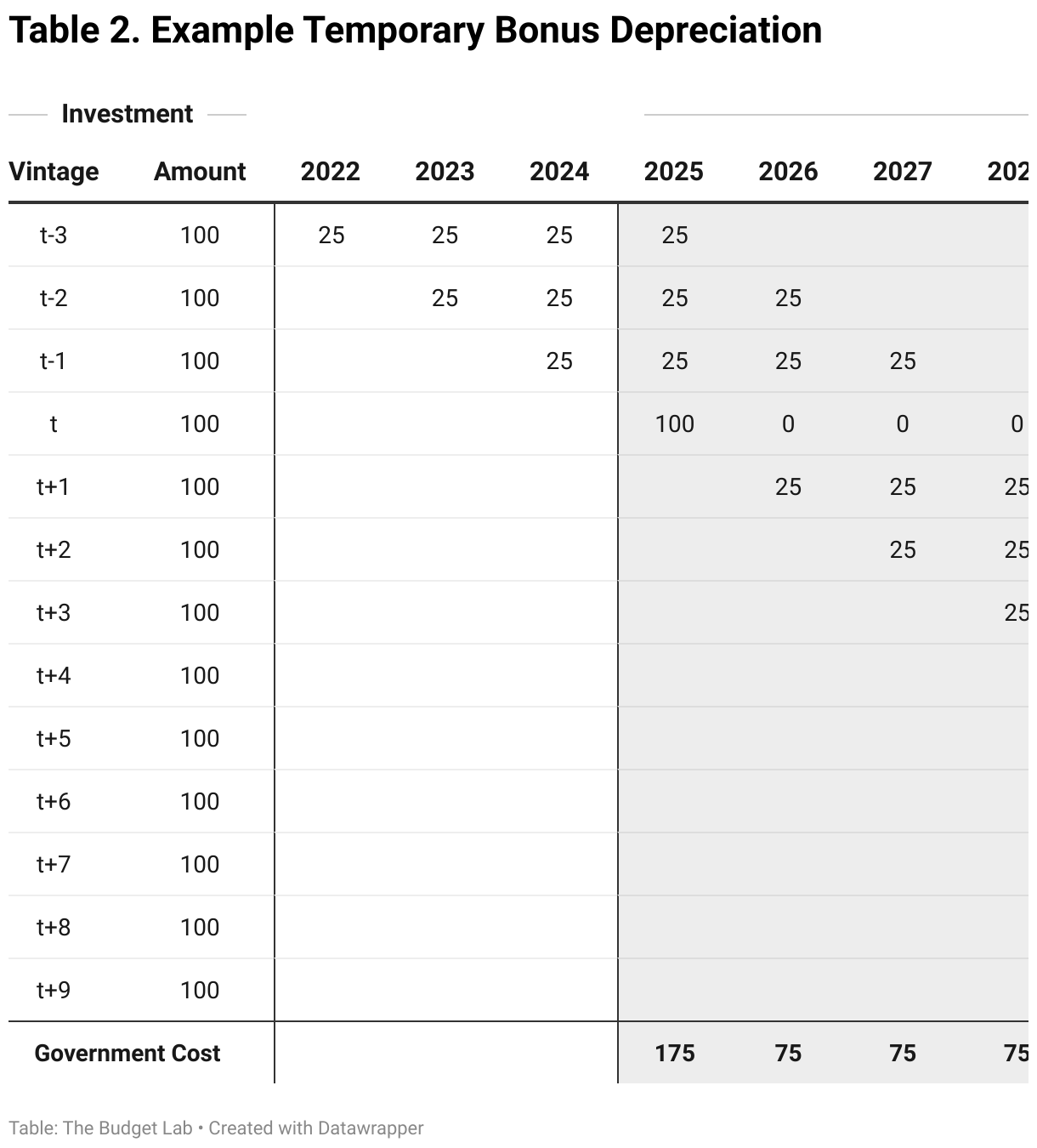

If a policy allows investments in year t to be fully expensed, government revenues are lower in year t than they would be under current law. However, in year t+1, government revenues are higher than they would be under current law. In fact, government revenues will be higher in every subsequent year until the end of the longest-lived asset put in place in year t. Table 2 illustrates this new depreciation system.

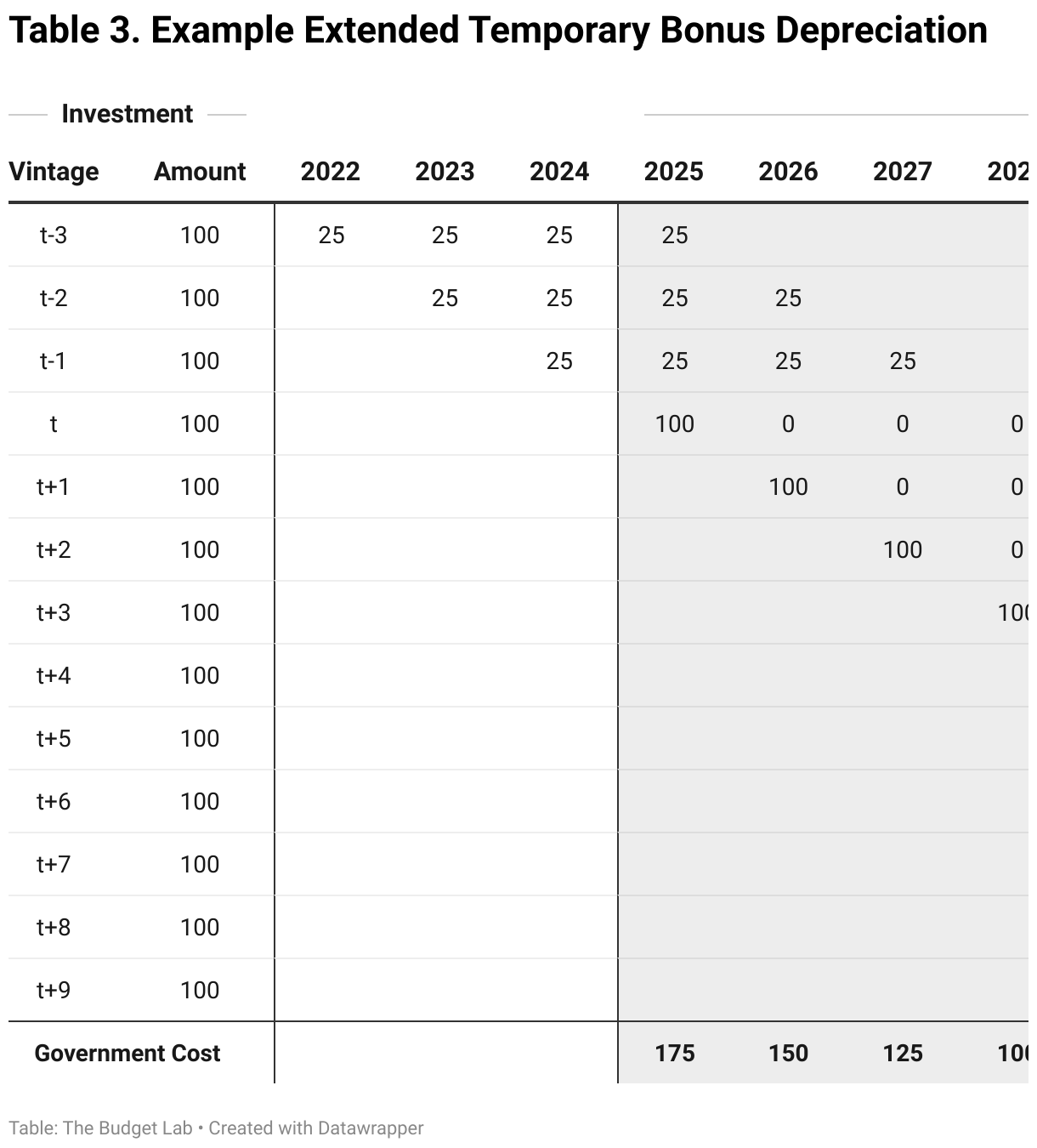

It is also the case that the increased deductions in earlier years will be made up by higher revenues in later years as long as the temporary policy ends within the depreciation period of the asset, in this case 4 years. Table 3 illustrates the last year of a temporary policy that nets to the same revenue as regular straight-line depreciation within the budget window.4

Legislative History of Depreciation

In the wake of the 1980 recession, President Reagan presented a “Program for Economic Recovery” to Congress. The Act established the Accelerated Cost Recovery System (ACRS) to lower the effective tax rate on depreciable investments. In ACRS, there are only six depreciable investment classes with recovery periods and cost recovery established in the code. Prior to this time there were over 100 asset classes and taxpayers were largely allowed to determine depreciable lives, salvage values, and accounting methods.

This system was modified by the Tax Reform Act of 1986 (TRA86). As part of the goal to simplify the tax code, the Department of Treasury presented an option for depreciation that eliminated the issues with ACRS namely, incorrect inflation adjustments, taxing alternative investments at different tax rates, and complexity. However, this recommendation was faulted for not providing strong enough investment incentives. A House-passed version created ten classes of assets with longer recovery periods and replaced straight-line depreciation with declining balance allowances. A compromise between these two proposals created the Modified Accelerated Cost Recovery System (MACRS). This system has remained in place since TRA86 with changes on the edges.

Depreciation has also been used as a policy tool by lawmakers to direct specific investment. Lawmakers have used depreciation allowances to induce taxpayers to invest in specific types of assets. For instance, in the Tax Reform of 1969 (TRA69) special depreciation allowances were enacted to benefit the construction of pollution control facilities and low-income rental housing (later changed to Low-Income Housing Tax Credit as part of TRA86). The Revenue Act of 1971 established special depreciation allowances for child-care facilities and job training facilities.

Lawmakers have also used depreciation allowances to help small businesses through Section 179 special depreciation. This depreciation policy allows taxpayers to fully expense investment. The amount is limited to a maximum amount that is phased out dollar for dollar if the investment exceeds a maximum amount and the deduction amount cannot exceed the taxpayer’s total income. It was established in the Economic Recovery and Tax Act of 1981 and expanding it in 2003 in the Jobs and Growth Tax Relief Reconciliation Act (JGTRRA), extending it American Jobs Creation Act (AJCA) of 2004. It was also expanded in 2007, 2008, 2010, 2012, 2013, and 2015 in the Small Business and Work Opportunity Act, Economic Stimulus Act, American Recovery and Reinvestment Act, Small Business Jobs Act, Tax Increase Prevention Ac, and the Protection Americans from Tax Hikes Act, respectively.

As part of the most recent tax reform bill (TCJA), bonus depreciation was increased to 100 percent for eligible assets. Under this provision, taxpayers could deduct immediately the full cost of new investments. However, after 2022, the amount of bonus depreciation decreased from 100 percent to 80 percent in 2023 and 60 percent in 2024. It continues to decrease by 20 percentage points until it phases out completely in 2027.

Under current law, taxpayers compute depreciation allowances using IRS determined lives and methods. Assets are determined to belong to a “class.” The class determines the useful life of the asset which includes 3-year, 5-year, 7-year, 10-year, 15-year, 20-year, or 25-year and 27.5 years and 39 years for residential rental property and nonresidential rental property, respectively. The IRS produces detailed tables to determine an asset’s class. The depreciation deduction is then determined by using either straight line or declining balance that switches to straight line method. Once the depreciation schedule is defined, the taxpayer can take additional bonus depreciation. For 2024, the bonus depreciation amount is equal to an additional 60 percent of the remaining depreciation allowances for the asset. As mentioned above, the bonus amount decreases by 20 percentage points until it reaches zero in 2027. The taxpayer can also elect to use section 179 depreciation. Under current law, the section 179 deduction limit for qualified assets is $1.22 million and the phase out threshold begins at $3.05 million.5

Conclusion

Depreciation policy is likely to play an important role in upcoming discussion surrounding the expiration of TCJA provisions. Understanding how depreciation works and how it has been treated in the tax code historically is important for policymakers to make informed decisions.

Footnotes

- Matthew Knittel, Corporate Response to Bonus Depreciation: Bonus Depreciation for Tax Years 2002-2004, U.S. Department of Treasury, Office of Tax Analysis Working Paper 98, May 2007

- Prior to passage of the TCJA, taxpayers could carry NOLs two years back. The Coronavirus Aid, Relief, and Economic Stability (CARES) Act allowed firms to carryback losses in tax years 2018, 2019, and 2020 for up to five years.

- See Congressional Research Service report “Bonus Depreciation: Economic and Budgetary Issues”, October 17, 2014, Zwick, Eric, and James Mahon. 2017. "Tax Policy and Heterogeneous Investment Behavior." American Economic Review, 107 (1): 217–48; and Ohrn, “The effect of tax incentives on U.S. manufacturing: Evidence from state accelerated depreciation policies,” Journal of Public Economics, Volume 180, 2019.

- Firms that ‘exit’ or ‘die’ are likely to claim deductions but would not survive to the point where the government would receive higher revenues. This fact may affect whether the net revenue is equal.

- The section 179 limitations are indexed for inflation. Any deduction that is not used because of the income limitation can be carried over to future years.