Estimating the Time Burden of Tax Filing

This post is part of a broader series explaining the modeling assumptions underlying our estimates. See here for other posts on this topic.

Tax compliance is costly. Each year, Americans spend hundreds of millions of hours and billions of dollars on complying with tax law. These costs, which vary by type of taxpayer, take the form of recordkeeping, filling out forms, paying professional tax preparers, and more. By changing the number of forms that taxpayers have to file or by introducing new compliance requirements, tax reforms can affect the overall time burden of taxes. As such, when analyzing major tax reforms, the Budget Lab includes estimates of the change in the time burden of taxes.

Our model for estimating time burden is based on IRS data. With each set of tax form instructions, the IRS includes an estimate of how much time the form will take to prepare. These time burden estimates are broken out into four categories: recordkeeping, understand the law, preparing the form, and compiling/transmitting documents. These estimates come from an IRS model, operated by the Research, Applied Analytics and Statistics Division (RASS), which uses tax filer survey to establish statistical relationships between specific forms and overall time burden.1 In other words, this exercise helps answers the question: “how many hours does it take to comply with this specific aspect of the tax code?”

Currently, the IRS model reflects increased electronic filing, and the time burden estimates are only disaggregated by business/nonbusiness filer and the aforementioned categories.2 Using prior versions of the model, IRS produced detailed time burdens by individual tax form.3 This detailed table forms the basis of our model of time burden. We also incorporate information provided by RAAS directly to our staff—namely, the time burden associated with tax provisions introduced in the Tax Cuts and Jobs Act (TCJA). When estimating the time burden effects of more fundamental reforms for which no specific forms exist, such as repealing Head-of-Household status or preferred tax rates on capital gains, we look to similar parts of the tax code when making assumptions about the associated time burden.

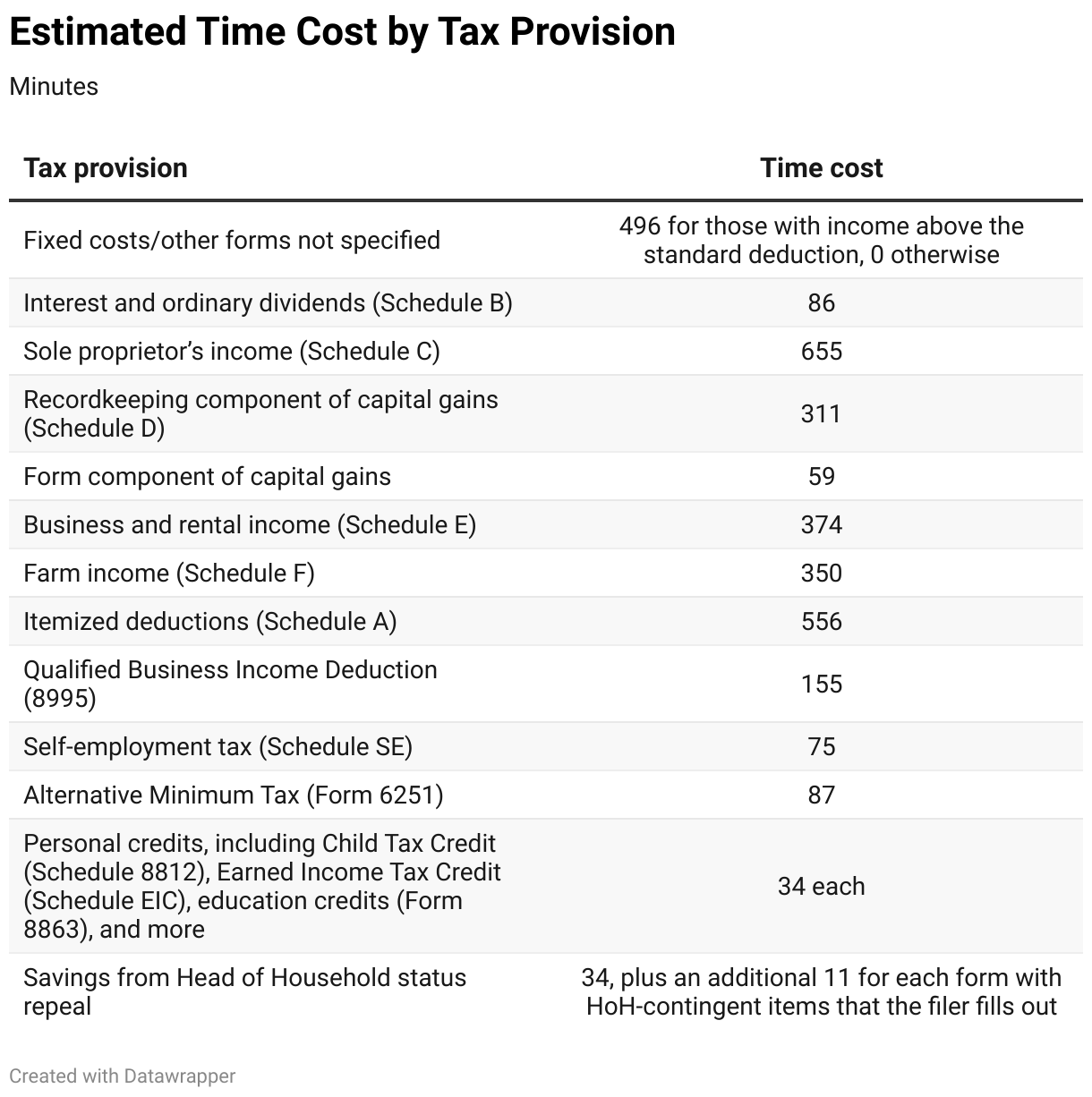

For a given tax policy scenario, our tax microsimulation model projects the number of 1040 filers with different kinds of income and different required forms to file. We then estimate the time burden for each filer using the following linear model of time burden. Finally, we aggregate filer-level estimated time burdens into an overall average.

The fixed cost of 496 minutes is estimated as the residual difference between the provisions we explicitly model and the IRS-reported average of 13 hours in 2022.

Our approach has several important limitations. One is that individual forms are assumed to have only additive effects on time burden; in reality, there is some overlap in the recordkeeping involved for certain forms. For example, because some of the line items on Form 6251 correspond with those of Schedule A, the joint burden of filing both forms may be less than the sum of each unconditional average. A second simplifying assumption is that the residual fixed cost does not vary with policy reforms; some of this time burden reflects specific forms which can change if tax law is changed. Finally, the underlying data is somewhat dated. Advances in computing and investments in IRS taxpayer services may have reduced time costs in recent years. For these reasons, our model’s estimates involve a fair amount of uncertainty, especially when analyzing more fundamental tax reform plans.

This page was most recently updated on June 20, 2024.

Footnotes

- IRS researchers also use the IRS burden surveys to monetize the burden of filing taxes. See IRS Publication 5743. Alternatively, Benzarti (2020) uses a representative sample of tax returns to estimate the monetary burden of filing around itemizing or using the standard deduction. Benzarti, Youssef. “How Taxing Is Tax Filing? Using Revealed Preferences to Estimate Compliance Costs.” American Economic Journal: Economic Policy, November 2020, 12(4): 38-57, https://www.jstor.org/stable/10.2307/27028630

- See page 108 of the 2023 1040 instructions: https://www.irs.gov/pub/irs-pdf/i1040gi.pdf

- See page 75 of the 1040 instructions for 2004: https://www.irs.gov/pub/irs-prior/i1040--2004.pdf