How Do Individual Changes in Economic Behavior Affect Our Revenue Scores?

Key Takeaways

-

Expected changes in employment would have small budgetary feedback effects.

-

We project that each reform would modestly increase the future earnings of children, especially low-income children. By the 2050s, these effects feed through into income and payroll tax revenues.

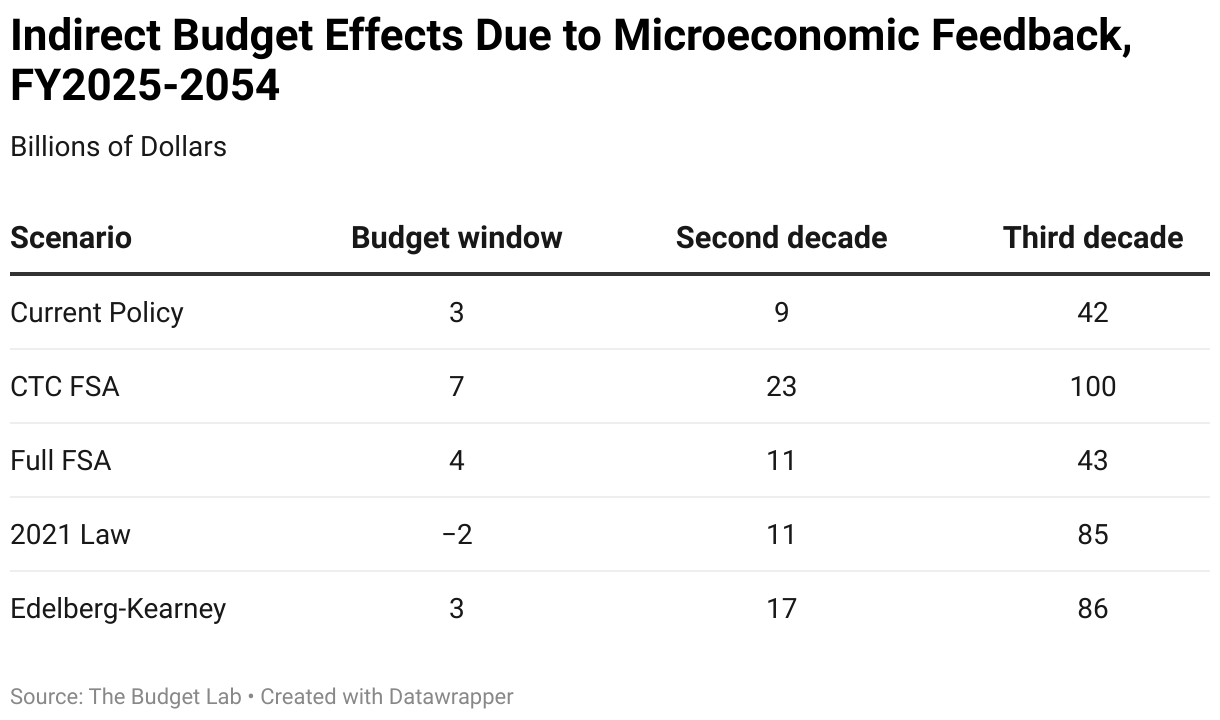

The cost estimates presented in our conventional scores do not reflect second-order revenue impacts of changes in parental employment or improvements in later-life outcomes. The table below presents the revenue change attributable to these types of behavioral feedback by scenario.

- The effects of a policy reform on children’s labor market outcomes take decades to fully manifest. As such, revenue feedback during the budget window mostly reflects changes in parental employment. During this period, only 2021 Law is expected to reduce employment and thus generates slightly negative revenue feedback, although for all plans the magnitudes of these impacts are relatively small.

- By the third decade, full cohorts of children who were fully exposed to a policy reform would now be adult workers. Here, long-run effects on children’s earnings outweigh short-run parental employment responses. Comparing 2021 Law to Current Policy in the third decade helps illustrate this point: despite creating second-order revenue losses through its employment effects, positive revenue feedback is expected to exceed that of Current Policy due to larger impacts on children’s earnings.

- While these results suggest that revenue inflows offset more than 10 percent of new outlays by the 2050s under certain reform scenarios, it is difficult to meaningfully compare concurrent outlays (which are spent on the current generation of children) with new revenues (which accrue due to policy interventions in prior generations). This is especially true of the reforms considered in this report, all of which are not indexed to inflation and thus fall in nominal cost over time due to real bracket creep, meaning that a crude contemporaneous comparison overstates the degree to which a policy “pays for itself”.1

Footnotes

- For example, if 2021 Law were indexed to inflation, the offset share of 2054’s direct cost would fall from 10 percent to 5 percent.