How Would TCJA Reforms Affect the Time Burden of Filing Taxes?

Key Takeaways

-

Currently, it takes an estimated 13 hours on average to file taxes. Certain reforms can reduce this burden for most taxpayers.

-

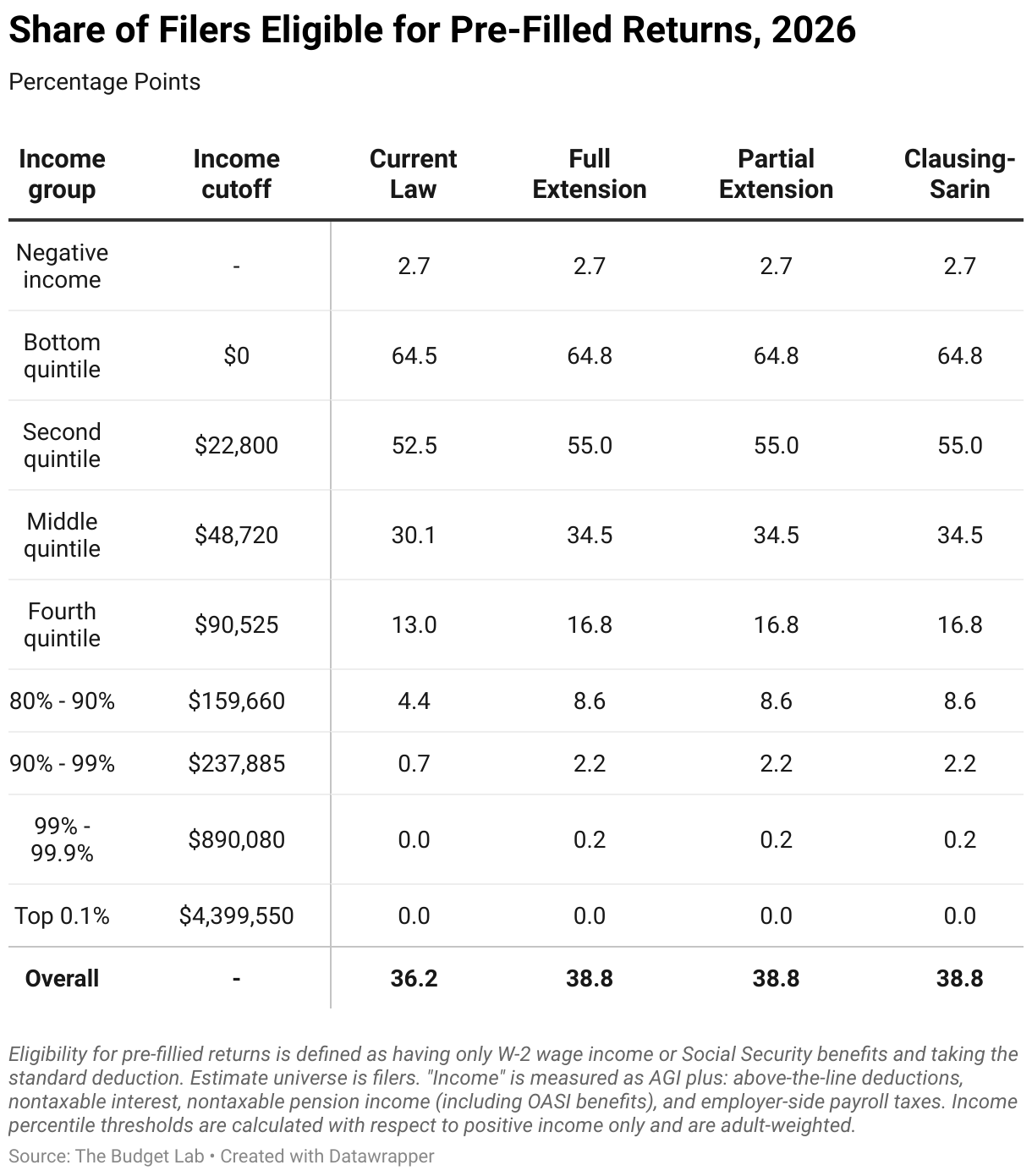

Nearly 40 percent of tax filers are candidates for a “pre-filled” option for filing taxes.

Time burden

Types of income

Certain types of income create larger time burdens for tax-filing than others. For example, wages are relatively simple – there is a single bilateral relationship between employer and employee, and the recordkeeping is done on the employee’s behalf by the employer. For those who own businesses, however, time burdens are much higher. Net business income is the combination of many transactions across both revenues and expenses, and these transactions are spread between many – potentially thousands – of customers, suppliers, and employees. As such, recordkeeping time burdens and form-filing is much higher for this group than for those who only earn wages. Other types of income, like capital gains or dividends, fall somewhere in between these two extremes.

Types of expenses

Taxpayers can deduct certain expenses, such as charitable contributions and mortgage interest, by electing to itemize deductions. Tracking these expenses and filing additional schedules to claim deductions is a time-consuming process.

Demographic characteristics

Certain tax benefits, like the CTC and EITC, are available to parents of children. To qualify, parents or caregivers must show that certain criteria pertaining to the relationship and support of dependents are met. Understanding these rules and filing extra forms adds to time burdens.

The IRS estimates that it takes 13 hours for the average taxpayer to do their taxes. This figure includes the time costs of recordkeeping, understanding the law, preparing all required forms, and compiling all forms into a filed return.1 These estimates come from a model that the IRS has developed using survey data to establish statistical relationships between the time burden and aspects of the tax return.2 The IRS highlights a large difference between business and non-business filers: the former takes 24 hours on average to meet tax-filing requirements while the latter takes 9 hours on average. As highlighted by Marcuss et al. (2013), over half of the cost of filing is due to reporting of income, so it is unsurprising that the IRS finds business filers spend almost 2.5 times as long as non-business filers in preparing their taxes.

The tax code includes several elements aimed at reducing the burden of reporting income, such as safe harbors and information reporting. Hence, tax reforms aiming to simplify the tax system may lower the time burden by reducing the number of forms and/or removing the need for extensive recordkeeping.

To estimate the change in time costs under the counterfactual tax policy scenarios, we use a simple model of time burden based on the IRS estimates described above. First, we assume an average time burden for categories of income, deductions, and credits.

Then, we use our tax microsimulation model to project the change in the number of filers who would need (or elect) to report each category under a counterfactual reform. This model yields a metric on which we can judge tax reforms: to what extent does it affect time burdens across the income distribution?

One stated goal among proponents of the TCJA was that many families would be able to file their taxes on a “postcard.” The implication is that time burden would be lower either through information reporting (as is provided for W-2 wages) or fewer additional forms to file. As enacted, the TCJA reduced the number of itemizers by increasing the standard deduction and limiting certain itemized deductions. These changes reduced time burdens by limiting the number of families who need to track and report deductible expenses. On the other hand, the law increased compliance costs by introducing the QBI deduction, expanding the child tax credit, and more.3

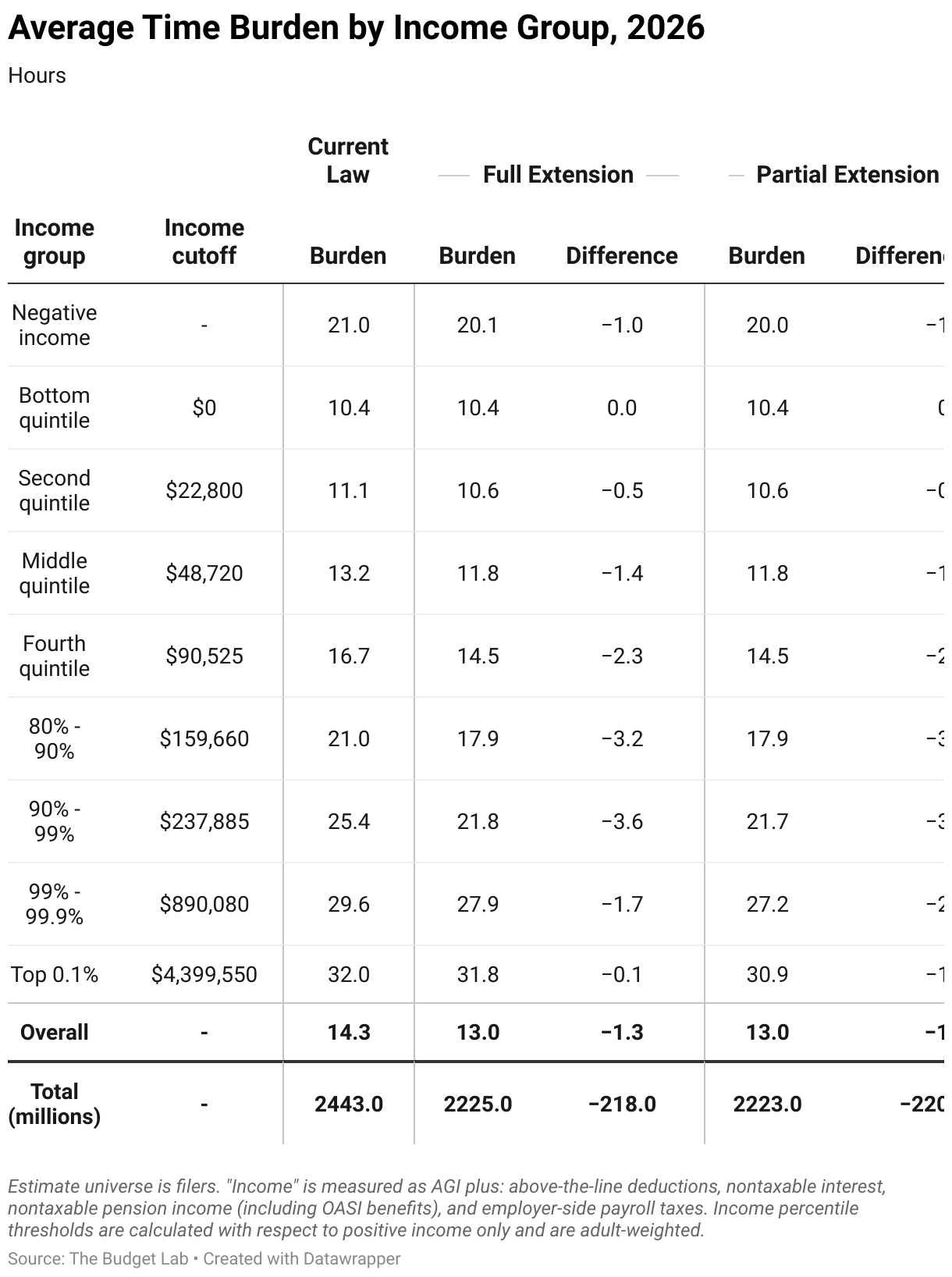

The table below presents the average burden in hours by income group under each reform option.

- Full Extension would leave tax policy unchanged from that of recent years, meaning that the average time burden should be roughly equal to the IRS’s 2022 estimate of 13 hours.

- Under current law, the standard deduction is scheduled to decrease, and certain restrictions on itemized deductions are set to expire. We project that in 2026, Full Extension would result in 13 percent of filers itemizing versus 30 percent under current law; this implies a reduction in compliance costs because it is time consuming to fill out and maintain records for Schedule A. These cost savings outweigh additional time costs associated with the QBI deduction, which expires under current law. On net, average time burden is about 1.3 hours higher under current law than under Full Extension.

- The Partial Extension reform is designed to mimic Full Extension for the bottom 99 percent of tax units by income. For those in the top 1 percent, who no longer qualify for the QBI deduction, time burden is estimated to fall on average. The overall average would remain unchanged.

- The Clausing-Sarin proposal would reduce burden beyond that of Partial and Full Extension scenarios by allowing the QBI deduction to expire entirely.

These estimates highlight the distribution of benefits from the QBI deduction. In the absence of extension of the QBI, very few income groups saw a drop in burden. The groups that did benefit are in the upper tail of the income distribution and likely benefited monetarily from the deduction even in the presence of the time burden. Much of the burden of the tax code is related to receiving benefits in return (CTC, itemization, QBI deduction, etc.). Individual taxpayers make tradeoffs between the extra filing burden and lower tax liability. However, there is a set of filers for which the time burden of filing taxes (and potentially paying a preparer) is possibly unnecessary.

Number of potential pre-filled returns

The time burden of tax filing is highly variable across taxpayers. For filers who only receive income subject information reporting, the government already has the information needed to fill out their tax returns.4 These are filers who do not file any extra schedules, do not need to comply with complicated rules, and are not required to engage in extensive recordkeeping – they receive only W-2 wages and/or Social Security earnings, both provided on information returns (W-2 and SSA-1099, respectively).This makes this set of tax filers ideal candidates for “pre-filled” returns, with minimal burden on the taxpayer. Such filers make up almost 40 percent of filers under any of the options presented in this analysis. In other words, the government can pre-fill 40 percent of returns, obviating the need for this group to file their taxes. The IRS is currently piloting a program called Direct File that allows residents in 12 states with similarly relatively simple returns to file directly with the IRS, although these returns are not pre-filled.

The burden of filing taxes for these individuals lies solely in filling out the 1040 with information that the government already has in its possession. Wages are already reported to Social Security Administration and the IRS. The tax filer is only verifying the information the government already has in its possession. The government could provide a prepopulated 1040 with a high degree of success.5

The table below shows the share of simple filers in each income group. These simple filers are largely unaffected by the policy changes we are examining, except for the change in the standard deduction. As such, there is little difference across policy scenarios.

Footnotes

See page 108 of the 2023 1040 instructions: https://www.irs.gov/pub/irs-pdf/i1040gi.pdf

IRS researchers also use the IRS burden surveys to monetize the burden of filing taxes. See IRS Publication 5743. Alternatively, Benzarti (2020) uses a representative sample of tax returns to estimate the monetary burden of filing around itemizing or using the standard deduction. Benzarti, Youssef. “How Taxing Is Tax Filing? Using Revealed Preferences to Estimate Compliance Costs.” American Economic Journal: Economic Policy, November 2020, 12(4): 38-57, https://www.jstor.org/stable/10.2307/27028630

The IRS reported in 2022 that the average burden for individuals was 13 hours. This number is estimated from the IRS’s Taxpayer Burden Model. In earlier versions of the model, IRS reported the time burden by specific form. Using the older model in 2004, the average time burden was slightly higher at 13 hours and 35 minutes. In our effort to quantify the burden of the different policy scenarios, we rely on these detailed time burdens as well as reported changes in time burden because of the TCJA. We generate burden amounts for each tax unit by adding the time to file the forms the tax unit files. The equation is:

BURDEN = 404.15 + A∗(556) + B∗(86) + C∗(655) + D∗(370) +E∗(374) + F∗(350) + SE∗(75) + EIC∗(34) + AMT∗(87) + CTC∗(34) + QBI∗(155)

Where the letters represent schedules and forms, and the numbers are the minutes required to file the form. The 404.15 minutes (about 6 and a half hours) is the baseline amount for individuals that do not file one of the forms listed in the burden equation. It is constructed using the IRS reported average of 13 hours in 2022.Guyton, John, Pat Langetieg, Pete Rose, Brenda Schafer, Sherri Edelman, Andres Garcia, and Molly Stasko. Taxpayer Compliance Burden. Publication 5743 (Rev. 4-2023) Catalog Number 93812U, Department of the Treasury Internal Revenue Service, February 2023, https://www.irs.gov/pub/irs-pdf/p5743.pdf

As noted above, Marcuss et al. (2013) asserts that information reporting can be viewed as an easing of time burden on taxpayers. Marcuss, R.D., G. Contos, J.L. Guyton, P. Langetieg, B. Schafer, and M. Vigil. “Income Taxes and Compliance Costs: How Are They Related?” National Tax Journal, December 2013, 66 (4), 833–854. https://www.journals.uchicago.edu/doi/10.17310/ntj.2013.4.03

Goodman, Lucas, Katherine Lim, Bruce Sacerdote and Andrew Whitten. “Automatic Tax Filing: Simulating a Pre-Populated Form 1040.” NBER Working Paper 30008, 2023, https://www.nber.org/papers/w30008