International Tax in the Age of Pillar 2

Introduction

The global tax landscape is at a critical juncture as countries begin implementing Pillar 2 of the Organization for Economic Cooperation and Development’s (OECD) and G20 Base Erosion and Profit Shifting (BEPS) project, which establishes a global minimum tax framework. The United States faces particularly complex decisions given its existing international tax regime, which includes the Global Intangible Low-Taxed Income (GILTI) rules, the Base Erosion Anti-Abuse Tax (BEAT), the Foreign-Derived Intangible Income (FDII) provisions, and the recently enacted Corporate Alternative Minimum Tax (CAMT). As other jurisdictions begin implementing Pillar 2's 15% minimum tax requirement, U.S. policymakers must evaluate various approaches to adoption, considering implications for U.S. tax revenue, business competitiveness, and international relations. This analysis examines potential scenarios for U.S. implementation of Pillar 2, ranging from U.S. not implementing while most other countries adopt to full adoption by the U.S., including the Undertaxed Profits Rule (UTPR). Each scenario presents distinct challenges and opportunities, affecting not only U.S. tax revenue but also corporate behavior, international competitiveness, and administrative complexity. Understanding these implications requires first understanding the proposed Pillar 2 framework and its interaction with the current U.S. international tax system, then evaluating how different implementation approaches would affect U.S. multinationals and foreign companies operating within the United States.

Pillar 2

Pillar 2 is a global minimum tax framework developed by the OECD/G20 that establishes a 15% minimum effective tax rate on large multinational enterprises (MNEs). The framework is based on three broad rules.

- First, the Income Inclusion Rule (IIR) requires parent entities to pay tax if their foreign subsidiaries' income is taxed below 15%.

- Second, the Undertaxed Profits Rule (UTPR) operates as a top-up tax when income anywhere in the corporate group is undertaxed.

- Finally, the Qualified Domestic Minimum Top-Up Tax requirement (QMDTT) taxes entities in the localities where they operate based on local profits.

The Pillar 2 system uses a country-by-country approach to implementing the three rules, meaning the 15% minimum must be met separately in each country where the MNE operates. This marks a significant shift in international taxation.

The system was designed to reduce tax competition between countries and reduce the incentive for entities to shift profits to low-tax jurisdictions. Implementation began in 2024, with various countries adopting the rules on different timelines. As more countries continue to implement Pillar 2, U.S. MNEs will face greater tax liabilities abroad. If the U.S. does not implement Pillar 2, these entities may face additional tax liabilities as other countries collect their share of undertaxed profits - resulting in forgone revenue for the United States. In other words, because there are now international minimum taxation requirements, MNEs will pay 15% tax rates to some country. It is just a matter of whether the United States is able to implement policies to capture some of that new revenue or not. We present potential scenarios below. For an explanation of how international taxation works under current law please see Budget Lab’s short background brief.

Pillar 2 Scenarios

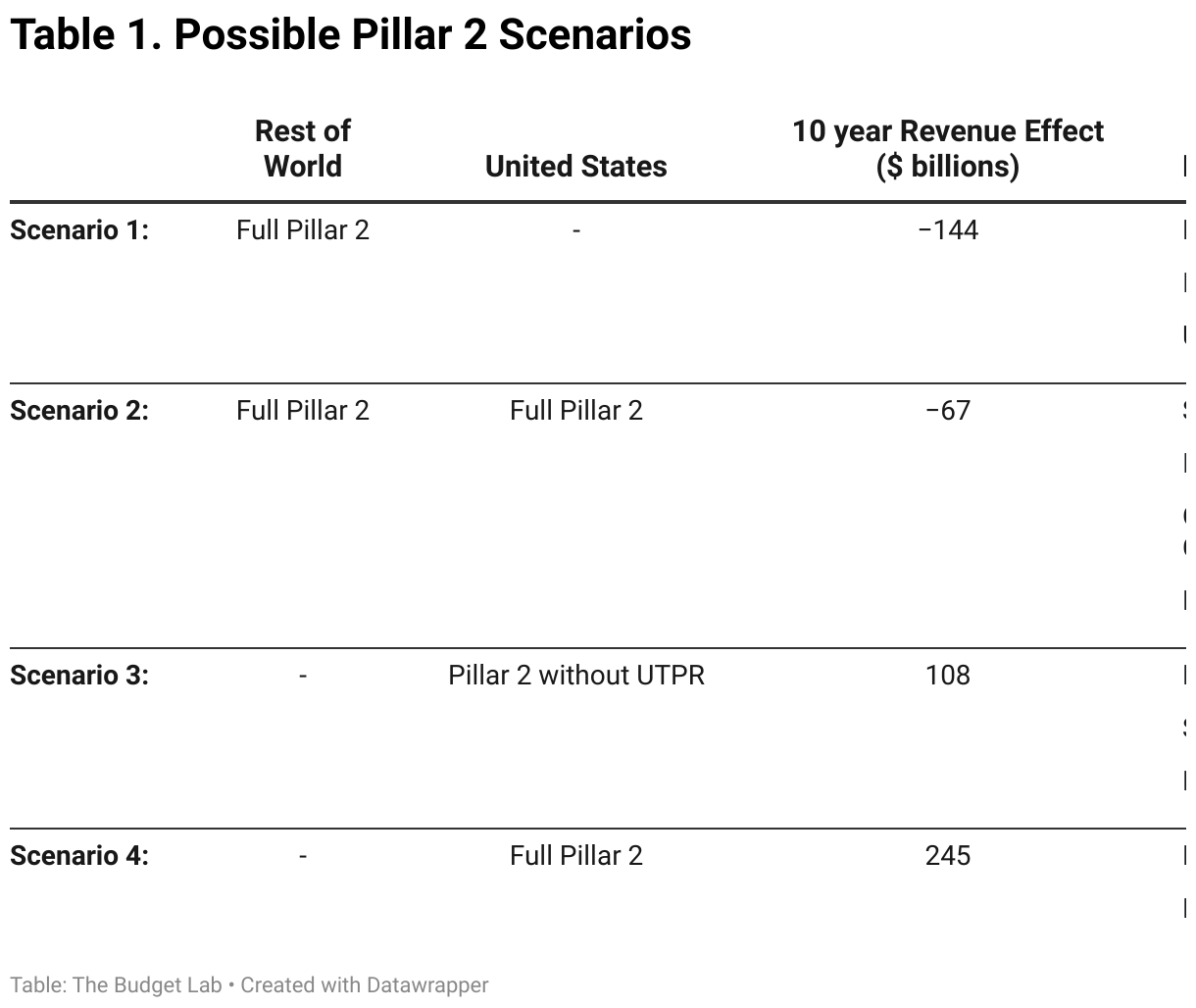

For our analysis of possible scenarios, we follow the possibilities outlined in the Joint Committee on Taxation’s (JCT) analysis of Pillar 2. There are four scenarios considered, with countries already compliant with Pillar 2 assumed to remain compliant; in the following, the rest of the world refers to countries that had not yet complied with Pillar 2 at the time of the JCT report: (1) The Rest of the World (ROW) enacts Pillar 2 while the U.S. does not; (2) ROW and the U.S. enacts Pillar 2; (3) ROW does not enact Pillar 2 while U.S. does enact Pillar 2 but does not enact a UTPR; and (4) ROW does not enact Pillar 2 while U.S. enacts Pillar 2 (with UTPR). An additional scenario is that neither the ROW nor the U.S. implement Pillar 2 which equates to current law. Table 1 summarizes the scenarios and key components.

Scenario 1: ROW Enacts Pillar 2

The most substantial impact under the scenario where the ROW enacts Pillar 2 but the U.S. does not is through the ‘top-up’ taxes. Other countries could collect additional taxes on U.S. MNEs undertaxed profits. This occurs because GILTI's effective rate (10.5% through 2025, then 13.125%)1 falls below Pillar 2's 15% minimum and foreign jurisdictions would have the right to collect the difference. This represents a direct transfer of tax revenue that could be collected by the U.S. Treasury to foreign governments.

U.S. MNEs would also face an increase in complexity and potential double taxation. The double taxation arises from the different definitions of income under the regimes. CAMT uses AFSI and it is unclear how CAMT would be treated internationally.

This uncertainty leaves the possibility that a U.S. MNE could pay CAMT and a foreign jurisdiction’s top-up tax. The MNEs would need to comply with both GILTI and foreign Pillar 2 rules. While the existence of GILTI alleviates the burden of top-up taxes relative to a situation where the United States had no minimum tax of its own, the global-blending under GILTI means that UTPR would still be collected on some low-taxed income of US MNCs.

U.S. MNEs could conceivably also face higher effective rates than local domestic competitors in countries with Pillar 2 complaint systems in some circumstances.2 This could influence corporate structuring decisions and potentially encourage inversions or a general restructuring of global operations. The lack of U.S. participation could create significant administrative burdens as U.S. MNEs would need to maintain parallel tax calculations –one for GILTI and one for Pillar 2 obligations. The CAMT adds another level of complexity and compliance burden.

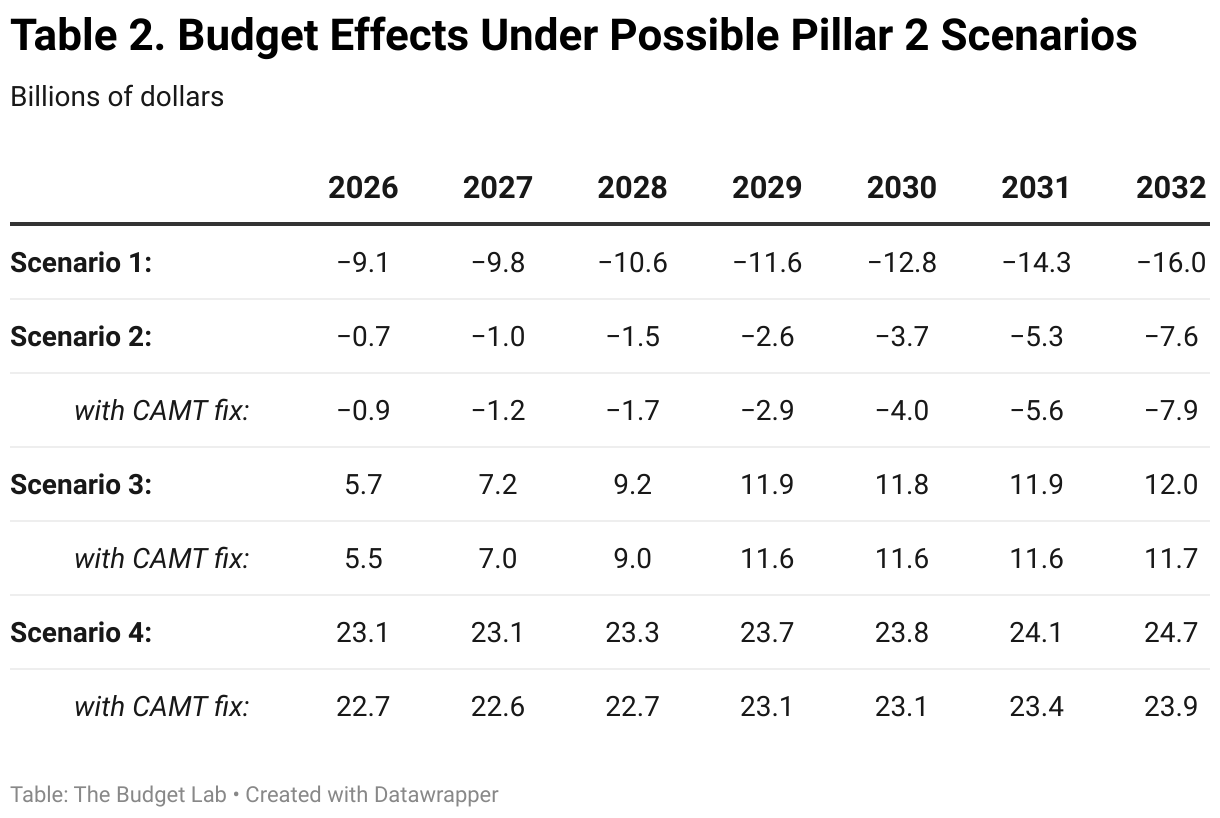

Table 2 shows the revenue the U.S. would forgo under this scenario. The loss in revenue represents the amount of revenue captured by foreign jurisdictions as they increase taxes on U.S. MNEs. Assuming an enactment date of 1/1/2026, the U.S. would lose $144 billion over the ten-year budget window. This revenue, as is the revenue presented below, is uncertain since it depends on the amount of profit shifting which we do not directly model.

Scenario 2: ROW & U.S. Enact Pillar 2

U.S. implementation of Pillar 2 mitigates the revenue loss faced under Scenario 1. It allows the U.S. to capture top-up tax revenue. It would likely require modifications to the GILTI system, including increasing the effective rate to 15% (already happening under current law) and implementing a country-by-country approach. In this scenario, we assume that GILTI is modified to comply with the requirement. There is uncertainty in the overall revenue effect under this scenario. The U.S. would likely see some profit shifting into the U.S., essentially reversing profit shifting that has occurred in the international landscape up until now, and therefore, an increase in revenue (since there is a reduced incentive to shift profits out of the country for tax reasons). The U.S. would also see an increase in revenue due to the implementation of the QMDTT. However, with the ROW also enacting Pillar 2, there is reduced amount of revenue to be collected under GILTI. Our calculations show a net loss revenue since the losses to other jurisdictions top-up taxes and reduction in GILTI revenue outweigh the increases.

Aside from the initial transition to this new regime, U.S. MNEs would face a lower administrative burden due to the coordinated international system. They would also operate under a more level playing field as all corporations would face the same minimum taxes.

Table 2 shows the revenue the U.S. would lose under this scenario. Assuming an enactment date of 1/1/2026, the U.S. would lose $67 billion over the ten-year budget window.

However, a potential pitfall in this world regime is CAMT. The interaction between CAMT and Pillar 2 introduces additional complexities and could result in double taxation risks due to the different tax base calculations and treatment of foreign income. CAMT calculates its 15% minimum tax using AFSI and treats foreign taxes as deductions rather than credits, while Pillar 2 uses its own distinct tax base calculation; CAMT also relies on a globally blended basis rather than on a country-by-country basis. This misalignment means a company could pay the CAMT in the U.S. but still face Pillar 2 top-up taxes in foreign jurisdictions. The potential for double taxation is particularly acute because CAMT payments may not be fully recognized as "covered taxes" under Pillar 2's calculations, meaning a company could face both CAMT liability on its global income and additional Pillar 2 top-up taxes in specific jurisdictions. As such, it may be necessary for guidance on coordination between these systems and potential legislative fixes to better align CAMT with Pillar 2 requirements.3 We estimate that legislative fixes slightly reduce revenue as the U.S. would receive less revenue from CAMT. Overall, the U.S. would lose $69 billion over the budget window in this scenario, almost exactly the same as in a regime without a CAMT fix.

Scenario 3: U.S. Enacts Pillar 2 without UTPR

In this scenario only the U.S. enacts Pillar 2 but does so without a UTPR. The U.S. would be able to collect higher taxes on U.S. parent companies' foreign operations through the IIR. However, without global implementation and no UTPR, foreign-parented groups could still benefit from lower tax rates in non-U.S. jurisdictions, potentially creating competitive advantages for non-U.S. multinationals. Without a UTPR, foreign companies could continue to shift profits to low-tax jurisdictions while operating in the U.S., while U.S. companies would face the higher Pillar 2 rates on their global operations through the IIR. This scenario could incentivize corporate inversions, increased use of foreign subsidiaries by non-U.S. MNEs, and shift investments to favor non-U.S. parent structures. The U.S. would increase revenue by $108 billion over the ten-year budget window. Allowing for a fix to the CAMT system would drop this to a $105 billion increase in revenue.

Scenario 4: U.S. Enacts Pillar 2

Full unilateral implementation of Pillar 2 by the United States, while other countries maintain their existing systems, would create significant complexities in the global tax landscape.4 U.S. multinationals would face a minimum 15% tax rate on a country-by-country basis through the IIR, while also subjecting foreign companies operating in the U.S. to potential tax adjustments through the UTPR. The U.S. would gain additional revenue from both U.S. multinationals' foreign operations and undertaxed foreign companies' U.S. operations. The U.S. would gain $245 billion over the ten-year budget window in this scenario. If this scenario was accompanied by a CAMT adjustment, the revenue increase would be $238 billion.

Additional Considerations

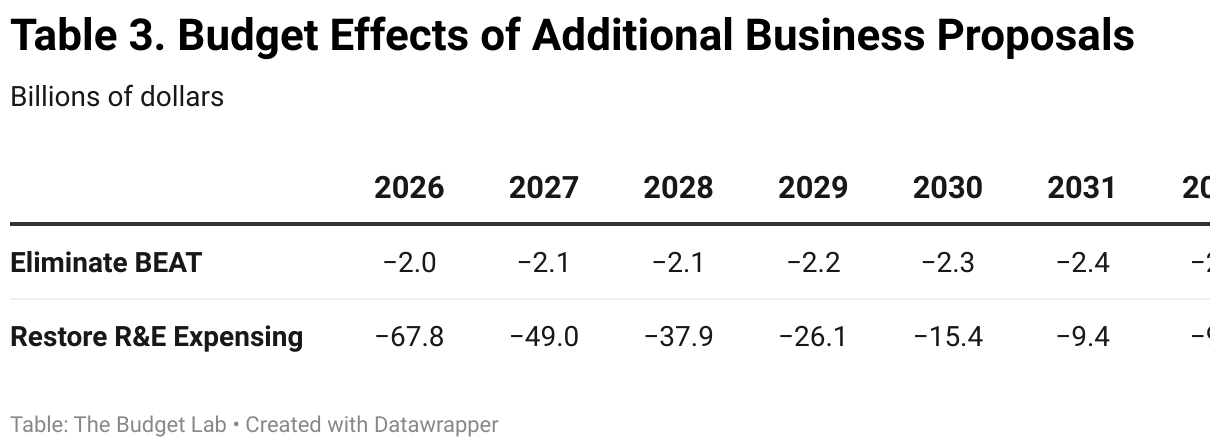

Since changes to current law are necessary to comply with Pillar 2, it is an opportunity to enact additional reforms. The BEAT was enacted as part of TCJA and aimed to discourage U.S. MNEs from shifting profits out the U.S. It acts as a minimum tax on large corporations. However, under any scenario where the U.S. enacts Pillar 2, the BEAT is unnecessary. The Pillar 2 components act towards achieving the goal of BEAT. As suggested by Clausing and Sarin (2023), BEAT could be turned off for GILTI payers. Turning off the BEAT would ease the burden on U.S. MNEs and subject them to a tax system more consistent to the rest of the world. This change would lose $14 billion over the ten-year budget window with year-by-year values shown in Table 3.

An additional proposal to ease the burden on corporate taxpayers is to restore the research and experimentation expensing to its pre-TCJA form. Under current law, companies are required to deduct investment costs over five years. The change made in TCJA resulted in increased costs for companies that spend money on research and development. Prior to the passage of TCJA, companies could deduct the full cost of research and experimentation. Reverting to the pre-TCJA version would remove a tax provision that puts U.S. companies at a disadvantage since no other country requires these expenses to be spread over time2. As seen in Table 3, this change would lose $243 billion over the ten-year budget window.

Conclusion

The complex interplay between potential Pillar 2 adoption scenarios and existing U.S. international tax provisions presents policymakers with challenging trade-offs that will shape the future of global taxation. As shown above, each implementation scenario carries distinct revenue implications, competitive considerations, and administrative burdens. Full implementation would maximize U.S. tax revenue capture. Global coordination on the Pillar 2 results in revenue loss (relative to current law) for the U.S. but carries the advantage of easing administrative burden and competitiveness concerns. A failure to implement Pillar 2, while other countries implement the changes, could result in significant revenue losses to foreign jurisdictions while creating compliance complexities for U.S. multinationals.

The business-friendly modifications explored—restoring immediate expensing for R&E and eliminating the BEAT—could mitigate some competitive concerns while promoting innovation and domestic investment.

In general, corporate tax reform involves revenue concerns but also concerns around long-term competitiveness, administrative feasibility, and international cooperation. This analysis will hopefully provide information that helps policymakers think through these trade-offs.

Footnotes

- The exact globally blended rates will depend on the distribution of activity across low-rate jurisdictions and the specific rates in those jurisdictions. Tax credits will also lower the effective rate.

- How much higher of a rate a U.S. MNE face depends on the proportion of profits being realized in the U.S. versus the amount non-U.S. firms realize in the U.S.

- Presumably, the CAMT could be adjusted to use the same concept of income as Pillar 2 and to be calculated on a country-by-country basis.

- It is important to note that some countries have already instituted Pillar 2 compliant tax systems.