The Potential Impact of IRS-ICE Data Sharing on Tax Compliance

Key Takeaways

-

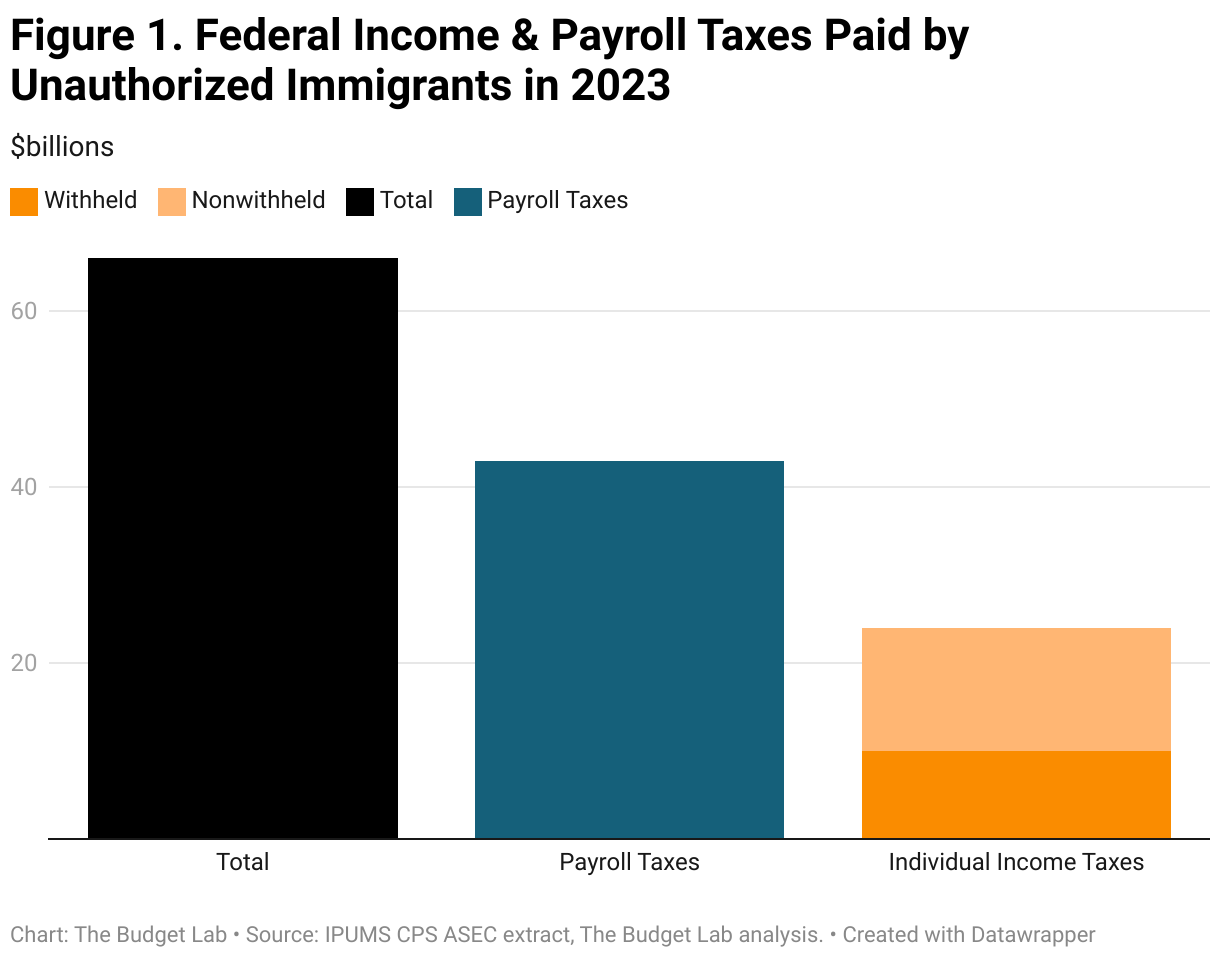

The Budget Lab estimates that unauthorized immigrants paid $66 billion in federal income & payroll taxes in 2023, about 2/3 of which was payroll taxes.

-

As a result of the proposed IRS-ICE agreement, unauthorized immigrants could become less likely to file taxes and/or move to jobs or pay arrangements less likely to withhold taxes.

-

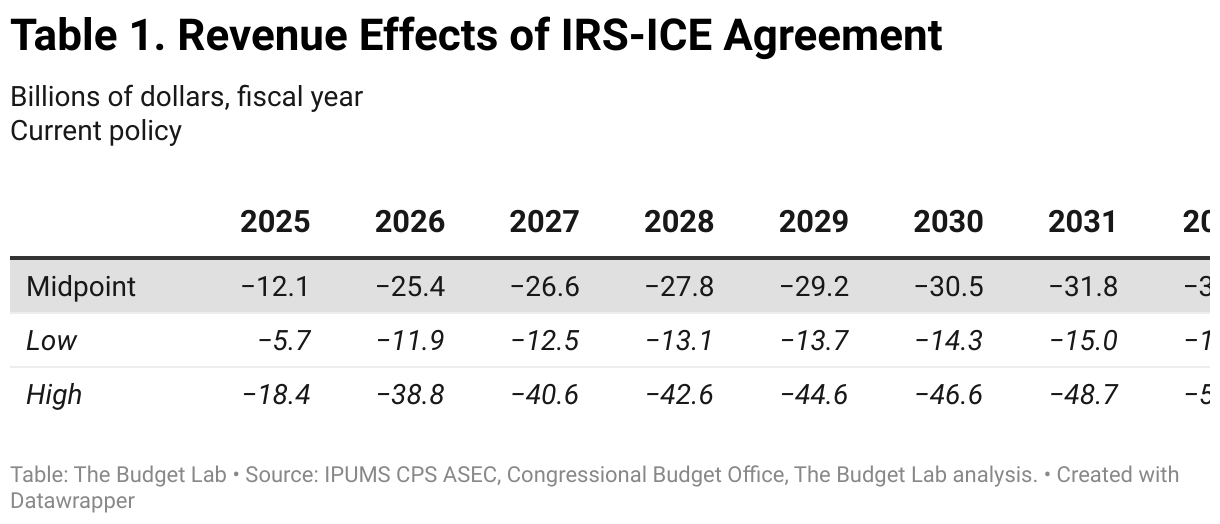

TBL estimates that the agreement could lead to a 0.5% loss in federal income and payroll tax revenue on average, or $25 billion in 2026 (central range of $12-39 billion) and $313 billion ($147-479 billion) over 2026-35. However, there is considerable uncertainty around this estimate as it is hard to gauge how taxpayer behavior will adjust and the extent to which adjustment will be feasible.

The Internal Revenue Service (IRS) has recently entered into an agreement with Immigration and Customs Enforcement (ICE) to allow immigration officials to use tax data to confirm the names and addresses of people suspected of being in the United States illegally, aiding ICE in its deportation processes.1 The IRS has historically made clear to the undocumented immigrant population that their tax information is confidential and would not be used in such ways. As a result, in addition to the economic and fiscal impacts of an increase in deportation, this action could be a decline in the share of unauthorized immigrant residents who file taxes, which would lead to a decline in federal individual income tax revenues and possibly payroll tax revenues. This analysis attempts to estimate the magnitude of this effect under different scenarios.

Background

Unauthorized immigrants pay a material amount in federal taxes. The Budget Lab estimates that in 2023, unauthorized immigrant workers paid $66 billion in federal taxes, with roughly $43 billion in payroll taxes2 and $22 billion in individual income taxes (see chart below; note that this does not include state and local tax payments). This is underpinned by the consistent finding that a majority of unauthorized immigrants likely pay federal taxes. The Congressional Budget Office (CBO) noted in a 2007 report that between 50-75% of unauthorized immigrants pay some combination of federal income and/or payroll taxes. Doing so minimizes the legal jeopardy of both the immigrant and their employer. In fact, North and Houstoun (1976) found that while 73% of unauthorized immigrants paid federal income taxes through withholding, only 32% filed a return. Since most Americans’ taxes are over-withheld, leading to a refund when they file, this suggests a strong possibility that many unauthorized immigrants already overpay federal taxes. Similar to this is the lifecycle overpayment of unauthorized immigrants, who often pay Social Security and Medicare taxes but are ineligible for benefits when they retire.

The IRS-ICE agreement could lead to a fall in the tax compliance rate among unauthorized immigrants if they become concerned that filing taxes could expose their personal contact information to law enforcement and be used to facilitate their deportation. The magnitude of this shift and its effect on federal revenues are highly uncertain, as there are several behavioral margins at play:

- The filing margin. Undocumented immigrants choose whether or not to file their individual income taxes. If immigrants become less likely to file individual income taxes as a result of this ICE – IRS agreement, the federal government would lose any non-withheld tax liability that still needs to be paid among payroll workers, and lose any self-employment taxes (SECA) and individual income tax liability among self-employed immigrants would otherwise file. Note that the sign of this effect is ambiguous: some filers could leave refunds on the table by not filing, and federal revenues would be otherwise higher in those cases.

- The withholding margin. Employers decide whether to employ undocumented immigrants “above-the-table” where taxes will be withheld, or pay them “under-the-table table” where no taxes are withheld or W-2s are provided to an employee. In response to the ICE-IRS agreement, the prevalence of undocumented workers that are employed “under the table” may increase as undocumented immigrants switch jobs to more informal arrangements or employers change their payroll practices. Relatedly but separately, undocumented immigrants may also become self-employed in increasing numbers, an arrangement that does not involve ongoing withholding. Either way, revenues unambiguously decrease along this margin, since presumably neither payroll taxes nor income taxes—withheld or filed—would be collected on the worker’s new informal earnings.

- The extensive margin. This is simply a question of what share of unauthorized immigrants and employers change their behavior at all. If none do whatsoever, then the effect on federal revenues of the agreement will be near zero (other than the fall in revenues resulting from any increased deportation operations, a distinct marginal effect not estimated here). If all do, the effect could be considerable.

Low and High Scenarios of Lost Revenue from the IRS-ICE Agreement

TBL estimates that the IRS-ICE agreement would cause federal revenues to be $12 billion for the remainder of fiscal year 2025, and $25 billion lower in fiscal year 2026. Over the next decade, revenues come in roughly $300 billion lower, roughly 0.1% of GDP on average (see table below), with a high estimate of just under $500 billion over the decade, and a low estimate of $150 billion. These are all current policy estimates that assume the Tax Cuts & Jobs Act of 2017 is extended over the next 10 years.

The fiscal effects are highly uncertain and depend strongly on the behaviors of unauthorized immigrants and their employers. To create its midpoint estimate, TBL averaged a “high” and a “low” scenario to capture the filing and the job switching margins. To capture the extensive margin—the likelihood that not all immigrants and employers would change their behaviors—TBL mitigated both scenarios by half. Note that this means the high and the low scenarios should be viewed more as rough central-estimate confidence bands rather than strict upper- and lower-bounds, since the extensive margin could in reality differ meaningful—higher or lower—than the 50% TBL assumed.

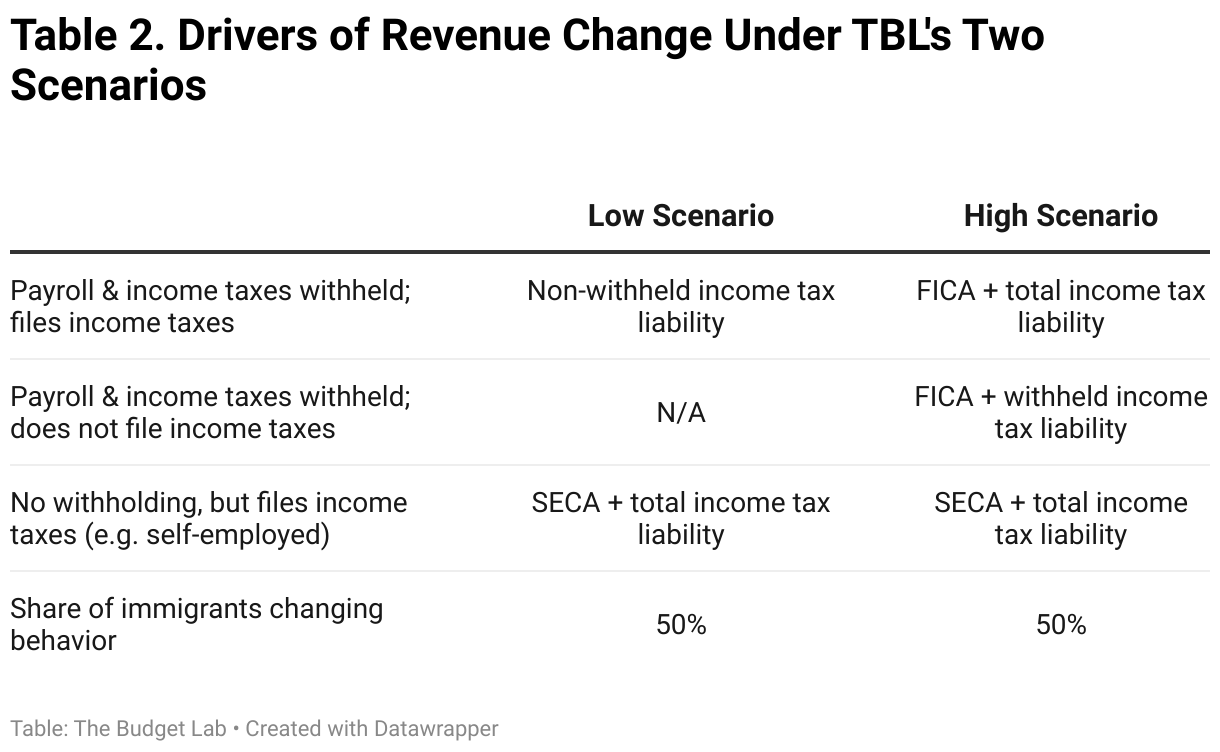

Low Scenario: Under the low scenario, the prevalence of undocumented immigrants working “under the table” does not change. Instead, half of them merely stop filing individual income taxes. Immigrant workers at payroll employers still have their FICA taxes and withheld income taxes collected; therefore, these portions of tax payments are not lost among such immigrants. The federal government only loses out on any individual income taxes owed at filing (and gets to keep any refunds due). The bigger effect comes from self-employed immigrant workers who file income taxes: if they no longer file, the federal government loses SECA taxes as well as the full individual income tax liability.

High Scenario: Under the high scenario, half of unauthorized immigrants not only stop filing federal individual income taxes, the prevalence of “under the table” employment arrangements also increases. Unlike the low scenario, the federal government now loses payroll tax revenue from unauthorized immigrant workers in payroll jobs who shift behavior. It also loses all income tax revenue from self-employed immigrant filers and payroll immigrant filers, and loses withheld income taxes from payroll non-filers.

Methodology

TBL’s tax analysis starts with the 2024 Current Population Survey Annual Social and Economic Supplement (ASEC), which includes demographic and tax information for tax year 2023. TBL identifies likely unauthorized immigrants in the ASEC beginning with a modified version of the Warren & Passel (1987) methodology: a “subtraction” method where all foreign-born noncitizens are assumed to be unauthorized at first, with the unauthorized population then culled down using the following removal criteria:

- All immigrants arriving before 1980;

- Immigrants from Cuba;

- Residents who likely qualify for DACA given their age, birth year, age at US arrival, and current educational enrollment or attainment;

- Foreign-born full-time students;

- Recipients of Social Security, Medicare, Medicaid, or rental subsidy benefits;

- Lives in public housing;

- Is in the armed forces, is a veteran, or receives military insurance;

- Works in the public sector;

- Workers who, based on their occupation, are likely licensed or in the US on an H-1B visa; and,

- Has a spouse who is a legal immigrant or citizen;

TBL then adjusts the ASEC weights to account for various margins of undercounting, including:

- The Census/Bureau of Labor Statistics’ December 2024 population controls, wedged back to March 2024;

- A broad adjustment for unauthorized immigrant undercount of +13% for those arriving in the most recent year, with the adjustment declining by 7.5% for each year further back, per Miller (2021).

- A further adjustment for undercount among El Salvador, Guatemala, and Honduras recent arrivals, per Warren (2024).

TBL then converted the ASEC from being on a personal/household basis to being on a tax unit basis. The ASEC includes tax variables like individual income tax liability and tax credits; however, these are the output of Census’ own tax model, which has no special insight into tax compliance, rather than direct tax data from the respondent. TBL therefore used the literature review of CBO (2007) to assume that unauthorized immigrants had a 50-75% probability of having their payroll & income taxes withheld, and separately a 50-75% probability of filing their income taxes. To calculate withholding, TBL used the 2023 W-4 withholding parameters to calculate an initial estimate of each tax unit’s withheld wages based on each worker’s earnings, then preserved the rank ordering but adjusted values to match actual IRS tax season data for aggregate & average refunds in 2023 as well as the share of filers receiving a refund. TBL made the further assumption that unauthorized immigrants do not claim the Child Tax Credit or Earned Income Tax Credit as part of their returns, given the SSN requirements. TBL assumed that tax units owing money on their federal individual income taxes (that is, where withholding is lower than total federal income tax liability) have a roughly 1/3-lower chance of filing federal individual income taxes, using the findings of Rees-Jones (2017) as a proxy. TBL simulated each scenario mentioned in the text 1,000 times, with variation stemming from random draws of the withholding and income-tax-filing probabilities, and used the median outcomes as the basis for the its score. To produce TBL’s score, the 2023 results are grown by a mix of the Congressional Budget Office’s January 2025 projections of personal income, wages & salaries, and the projected increase in the foreign-born population relative to the overall population.

Footnotes

- The federal government has a long history of separating the collection of taxes from immigration enforcement efforts. This is why in 1996 the IRS created the ITIN—to enable individuals who do not have a SSN to still comply with US tax laws. In the nearly-thirty years since, leading immigration experts and organizations, including the American Immigration Council have underscored that the use of ITIN would not be used in immigration enforcement efforts, pointing to Section 6103 of the Internal Revenue Code which limits the ability of the IRS to release taxpayer information to other government agencies. Legal procedures have however always existed to disclose taxpayer data to law enforcement in non-tax criminal cases, usually involving a court order or, in the case of terrorism and national security, the authorization of a high-ranking official.

- This includes the employer’s share of FICA taxes as well as SECA taxes.