Budgetary Dynamics of Depreciation Policy: Options for Reform

Depreciation policy—the rules which govern when businesses can deduct capital investment costs—is an important dimension of the business tax system, influencing investment incentives, the timing of government revenues, and the relative tax treatment of specific industries. Because the current-law regime of “bonus depreciation” is phasing out over the next few years, depreciation policy is likely to play an important role in discussions around the expiration of the Tax Cuts and Jobs Act’s (TCJA) individual tax cuts—especially when it comes to budget scorekeeping.

Revenue dynamics associated with changes in depreciation policy have significant implications for budget scorekeeping. Generally speaking, lawmakers are incentivized to propose temporary policy changes, rather than permanent changes, when those changes would increase the deficit. Doing so makes the budget cost appear lower for scorekeeping purposes—a benefit which is weighed against the gamble that future policymakers will not extend these changes.

But for temporary bonus depreciation (or any move towards accelerated depreciation schedules), the cost of permanent extension relative to the temporary score is much higher than for other policies. For a typical deficit-increasing temporary policy change, the cost of extension can be approximated using the average per-year cost. For example, imagine a temporary one-year tax credit expansion that reduces revenues by $10 billion. If extended permanently, the cost would be close to $100 billion over ten years.

With temporary bonus depreciation, however, the early-year costs are partially or fully offset by higher revenues later in the window. This is because temporary bonus depreciation merely shifts deductions from later in the budget window to earlier in the budget window, creating a negative-then-positive pattern of annual revenue impacts. In other words: the net ten-year cost is often close to zero, despite the fact that a permanent policy would reduce revenues on an ongoing basis (though by less than what the first few years would suggest). This means that the ratio of permanent cost to temporary cost is much higher for temporary bonus depreciation—i.e. temporary bonus depreciation is a “gimmick” as other budget analysts have pointed out in the past.

In this report, we present five policy experiments, and the associated conventional estimates, which underscore these budgetary dynamics and highlight differential impacts across industries:

- 100% bonus depreciation from 2025-2027.

- 100% bonus depreciation from 2025-2029 followed by a linear phase down from 2030-2034.

- Permanent 100% bonus depreciation.

- Permanent full expensing.

- Neutral cost recovery.

Please note: For readers who are new to depreciation or need a refresher, a full backgrounder is provided in this companion piece.

Budgetary Effects of Reform Options

In this section, we present five options for reforming depreciation policy. These options are crafted to highlight the budgetary tradeoffs that policymakers face—and the potential pitfalls associated with evaluating depreciation policy using only the conventional ten-year budget window. We use our depreciation model to estimate the effects on government revenues.

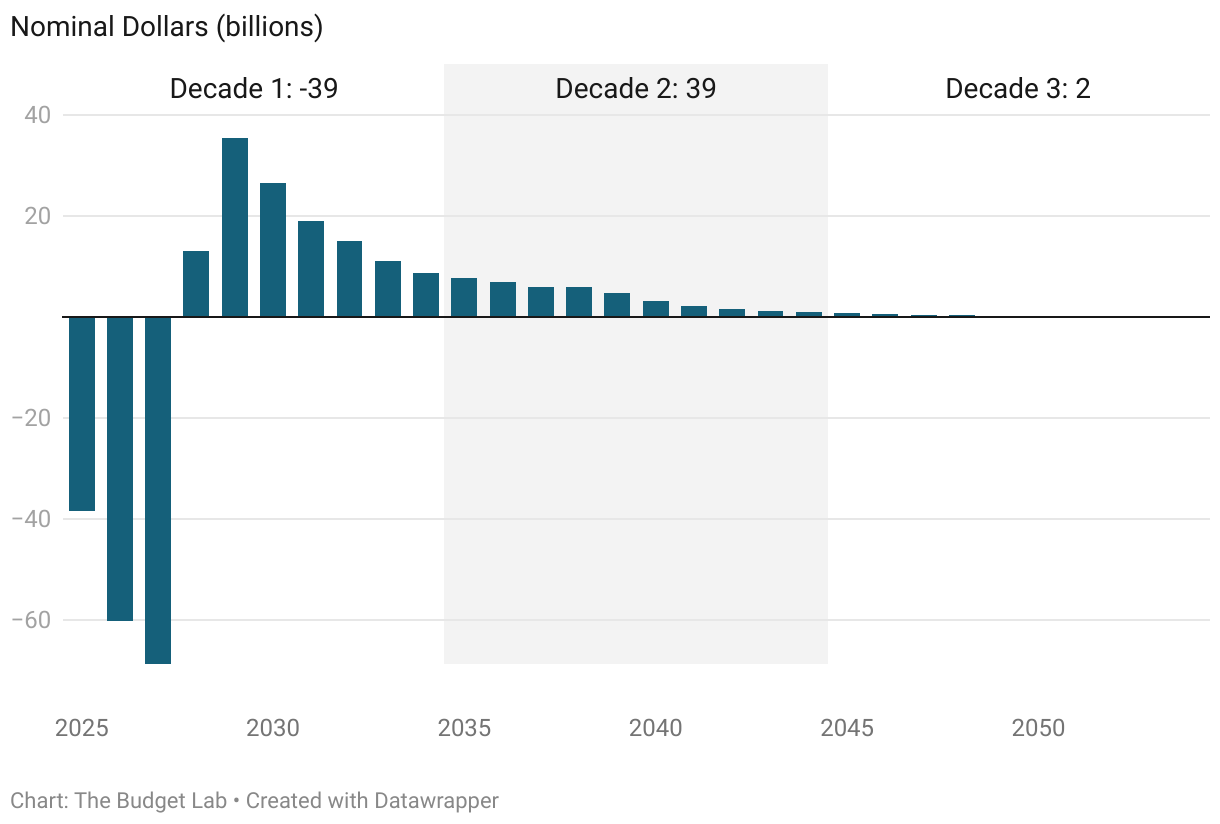

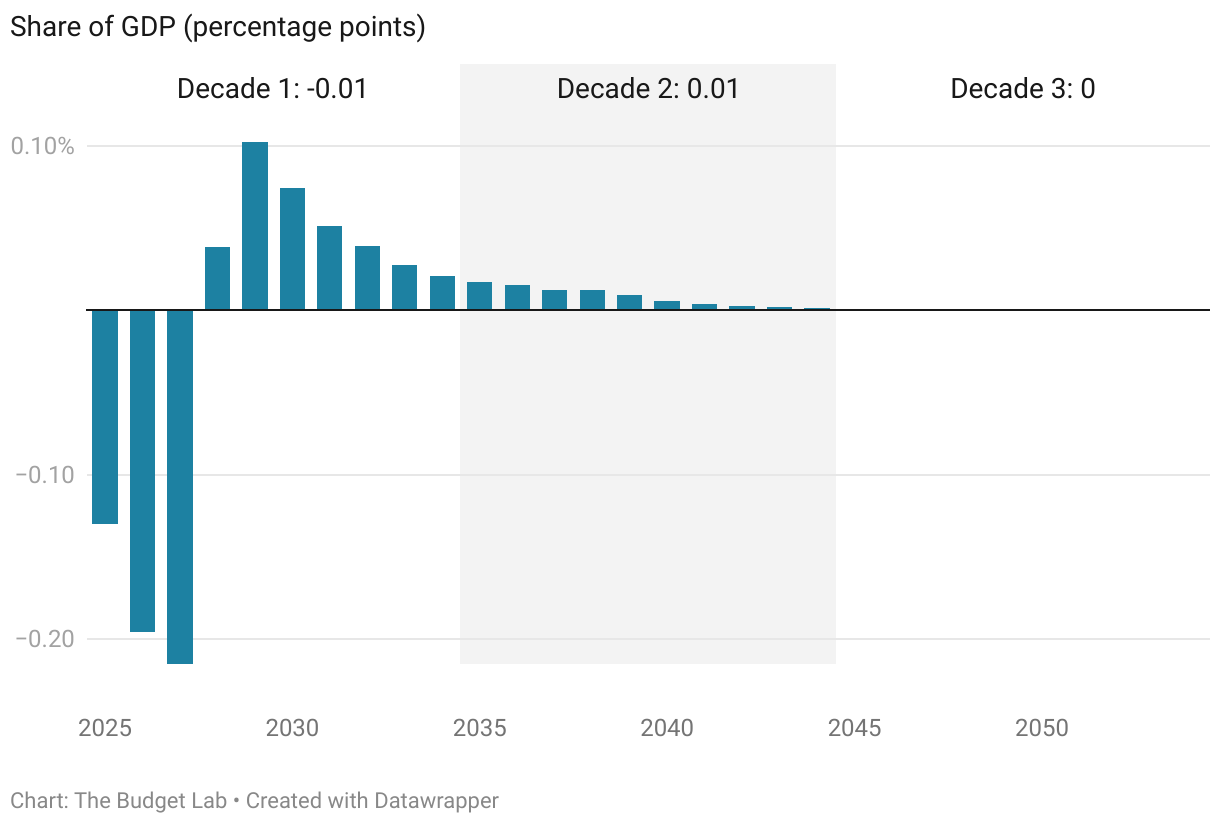

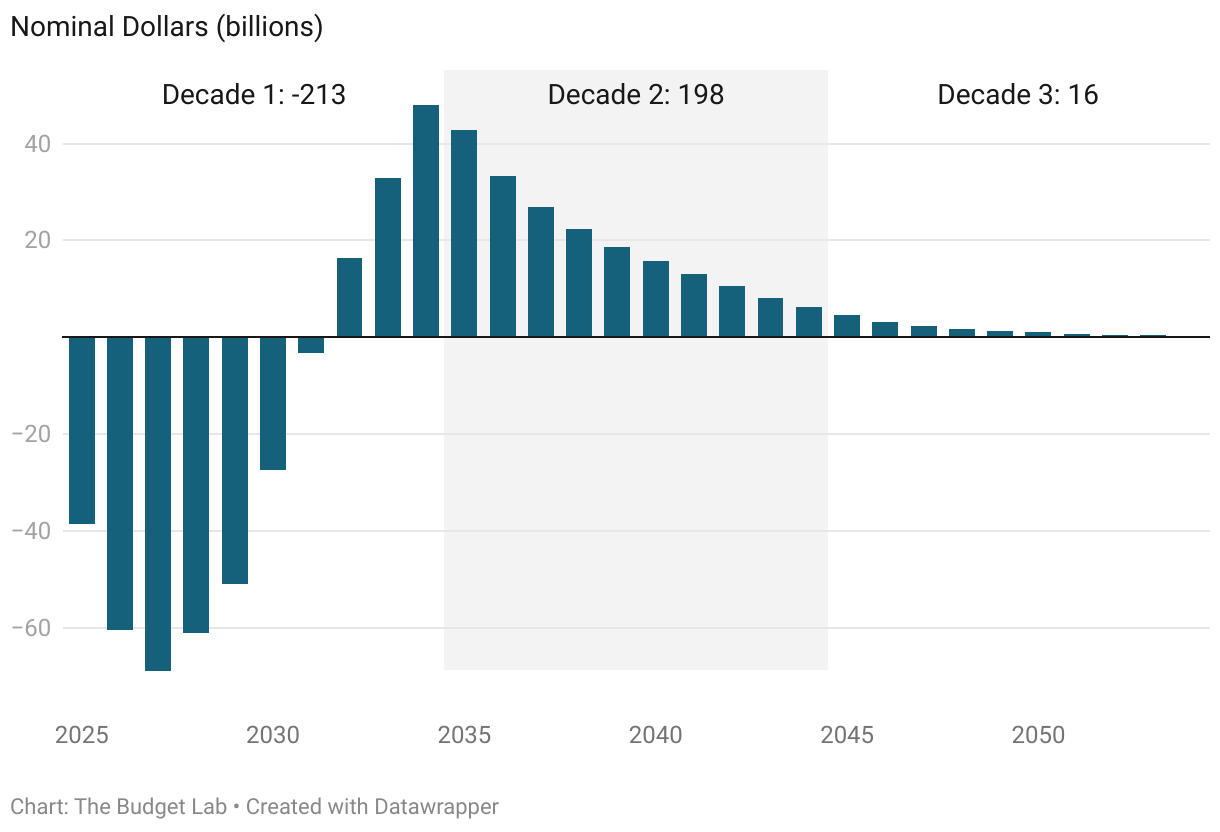

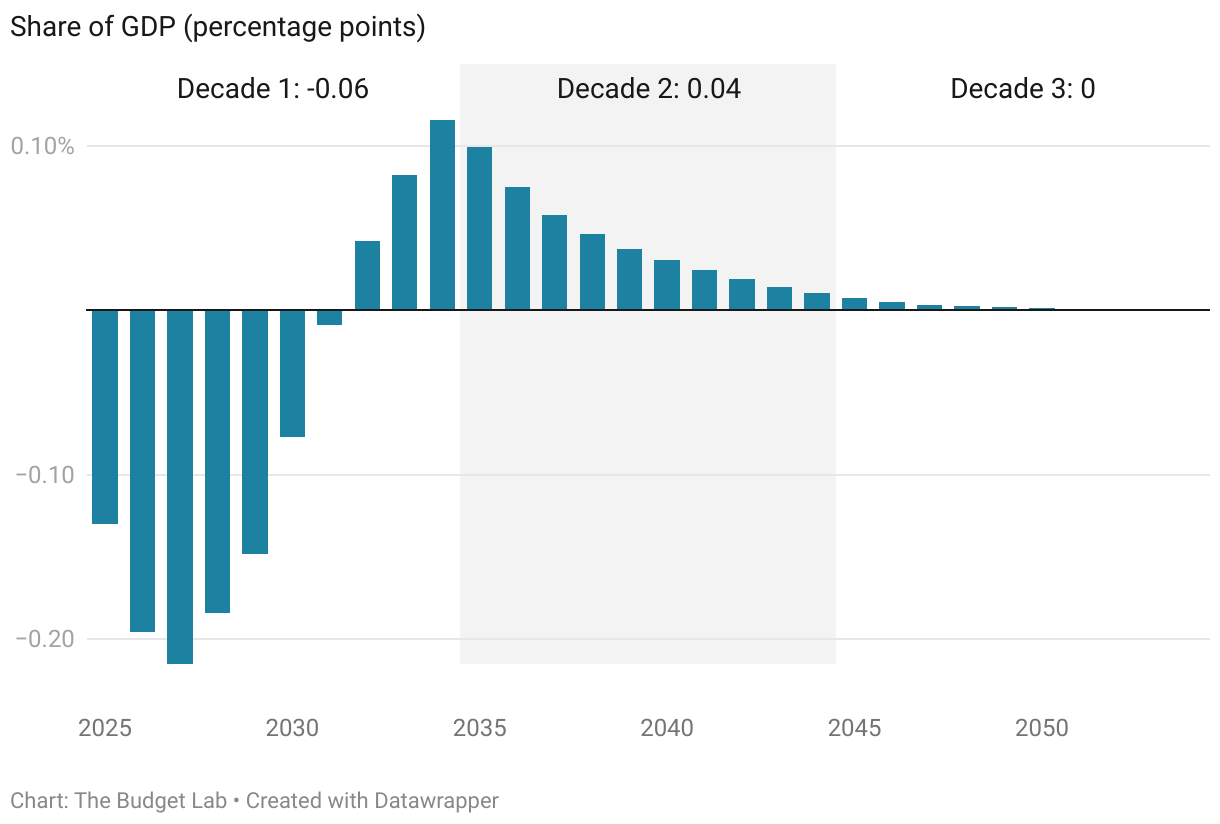

Options (1) and (2): Temporary 100% Bonus Depreciation

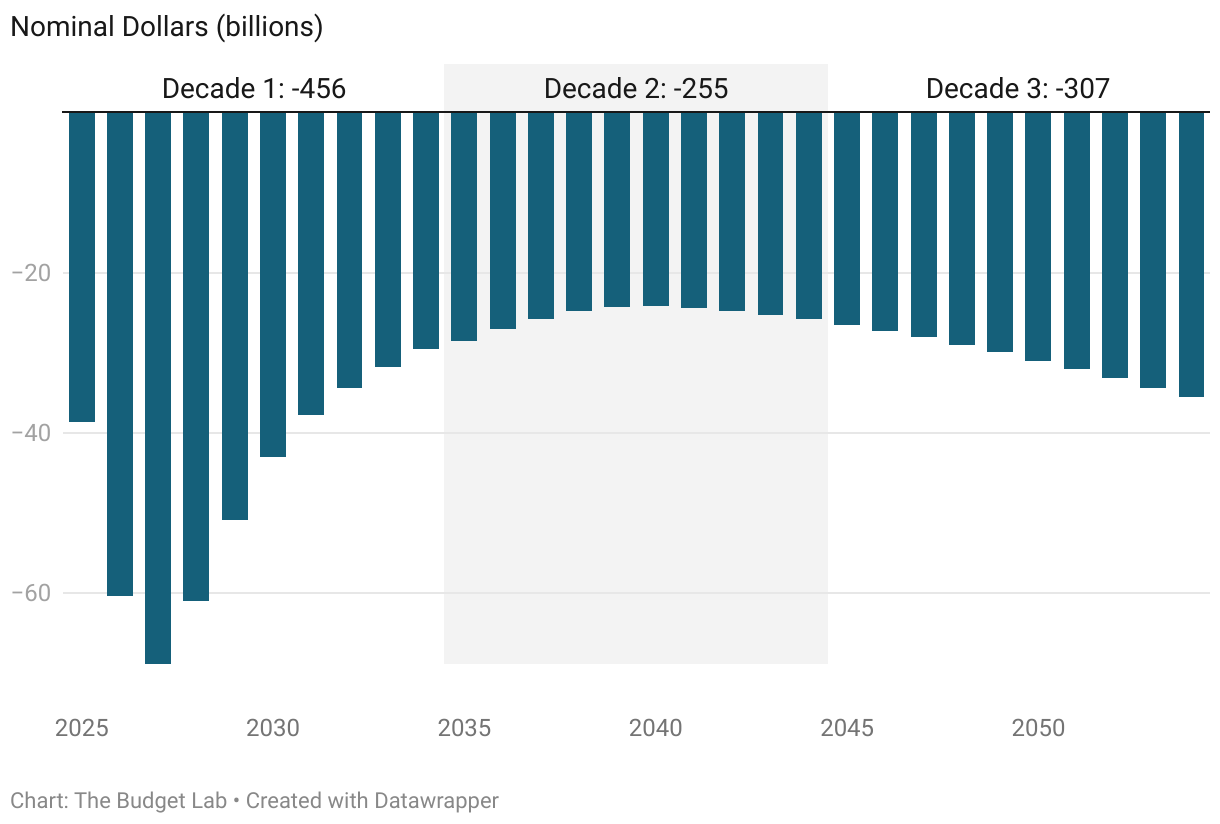

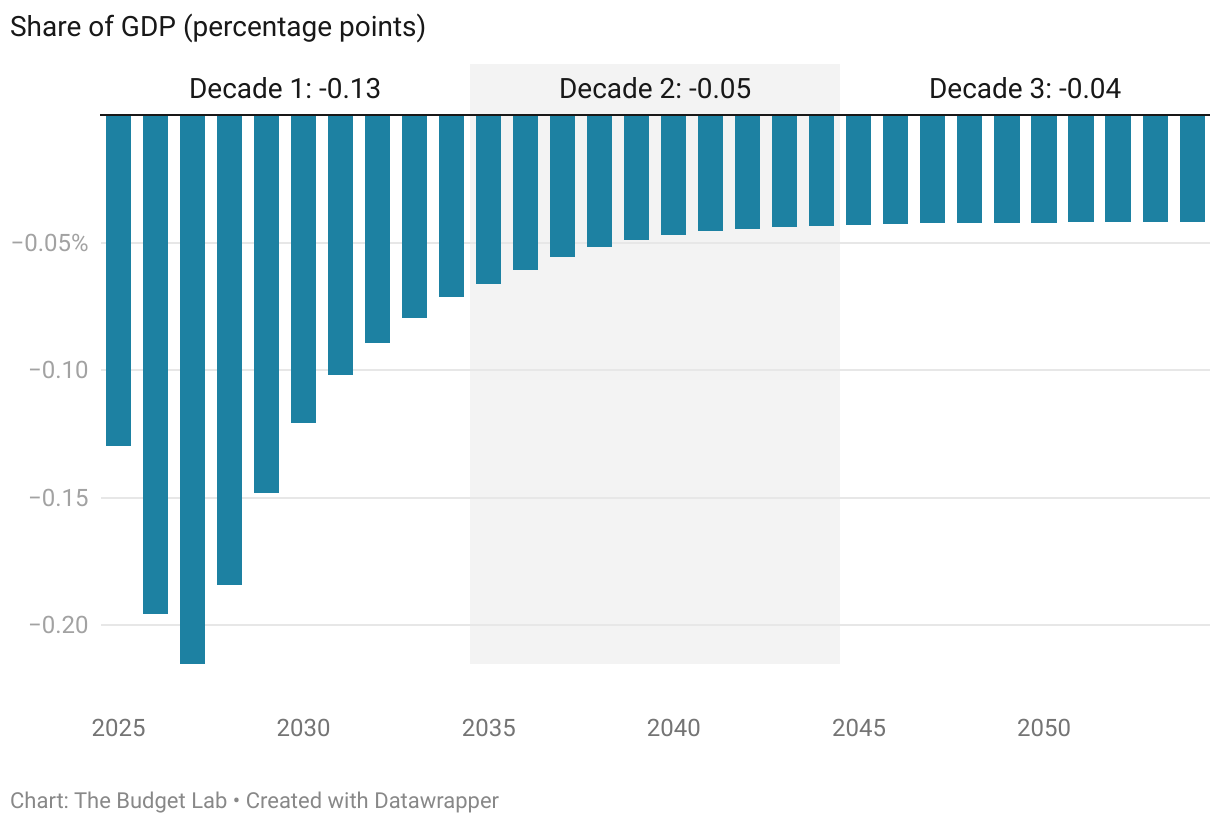

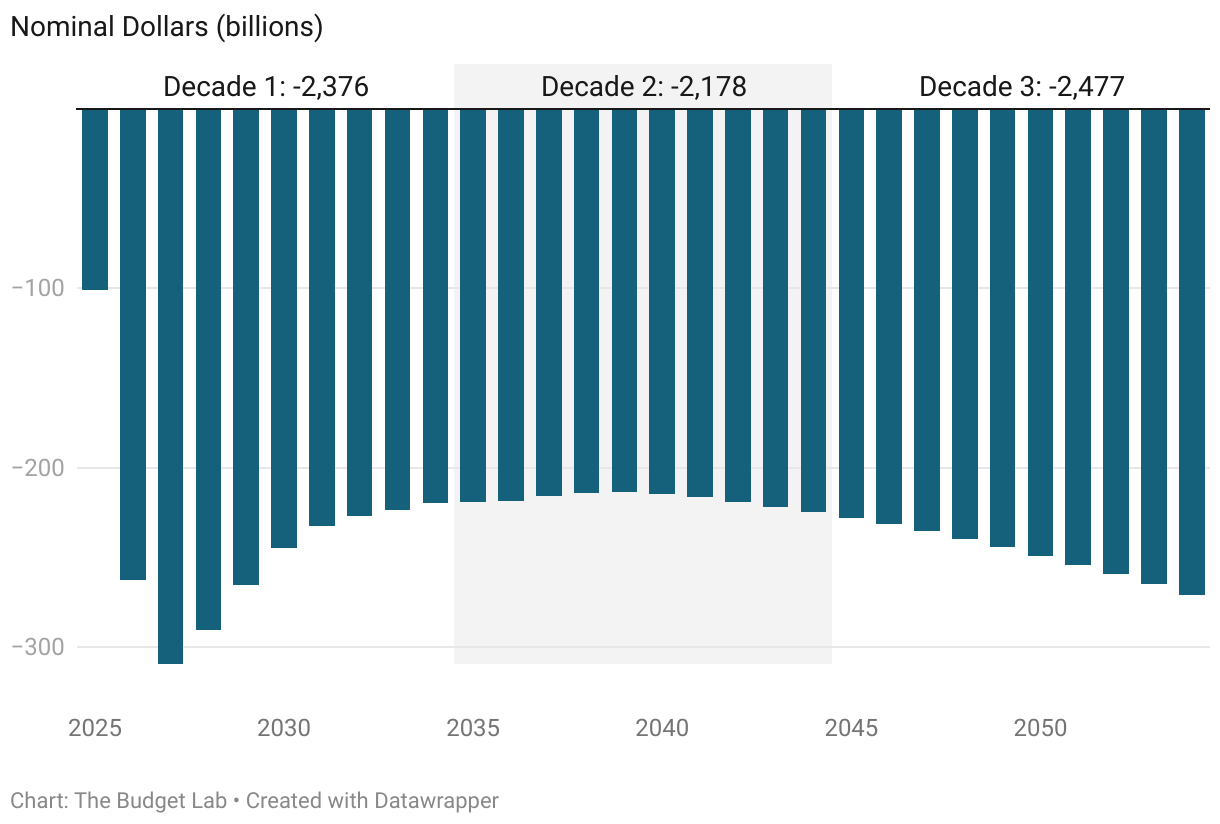

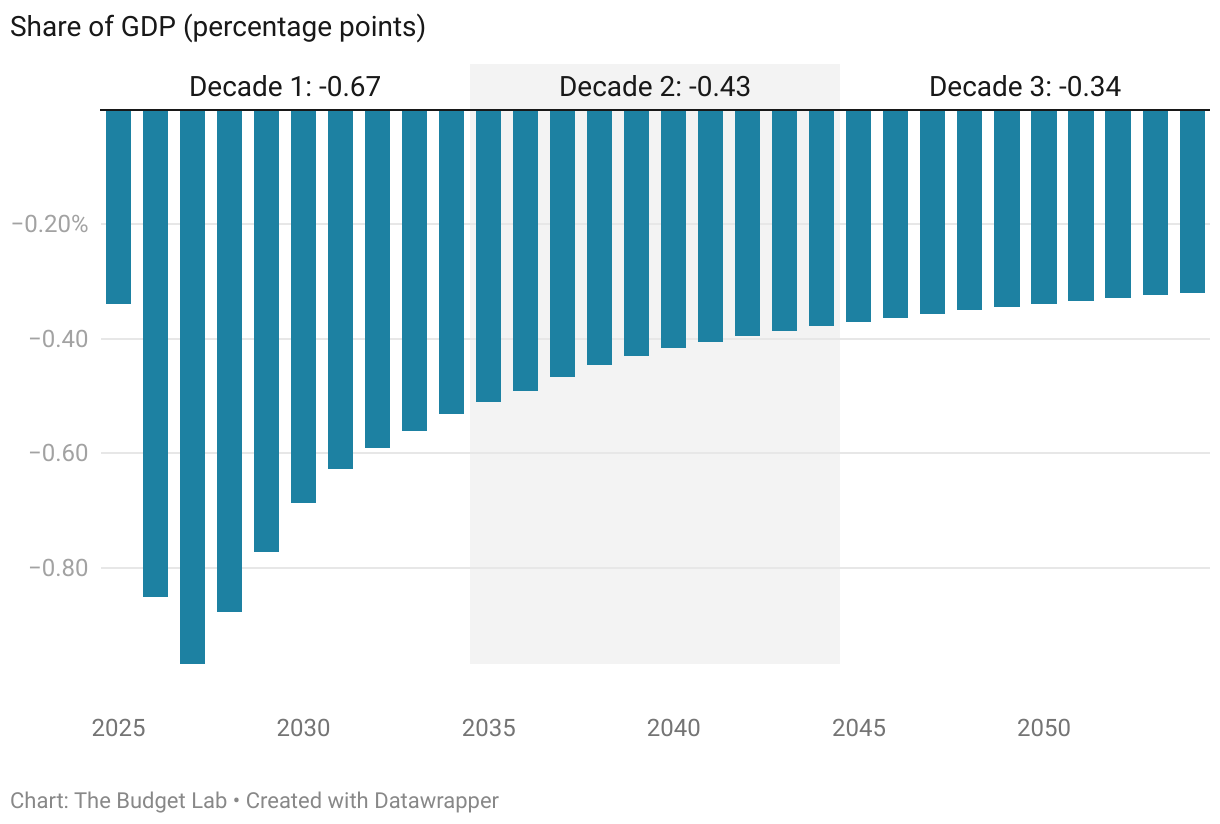

The first two options would re-instate 100% bonus depreciation, which is phasing down to 0% in 2027 under current law, on a temporary basis. Option (1) would allow 100% bonus depreciation for three tax years (2025-2027), after which current law—0% bonus depreciation—would resume. Option (2) would replicate the pattern introduced in TJCA: five years of 100% bonus (2025-2029), then a linear phase-down from 100% to 0% over the next five years (2030-2034).

Figures 1 and 2 plot estimated budget effects of these reforms over the next three decades. Both scenarios exhibit the basic revenue dynamic associated with temporary bonus depreciation policy. Depreciation deductions that would have been taken in the future are instead taken in the near term—as is true of all bonus depreciation policies, either temporary or permanent. But in the years following expiration, there are no residual bonus deductions to offset taxable incomes, leading to higher revenues in those future years. In other words, temporary bonus depreciation moves tax liability from the present into the future, with no long-run, steady-state effect on nominal revenues.

Figure 1. Estimated Budgetary Effects of Option (1), 2025-2034

Figure 2. Estimated Budgetary Effects of Option (2), 2025-2034

Option (3): Permanent 100% Bonus Depreciation

This option establishes 100% bonus depreciation on a permanent basis. There is no budget window “gimmick” to make this policy appear cheaper than it is, so revenues are permanently lower than they would be without the policy. For each year into the future, depreciation deductions are pulled forward from the future into that year. But it’s worth noting that these costs are larger in the short run than in the long run, relative to the size of the economy. In the short run, there is a one-off “transition period” when firms are deducting the costs of investments made under the new law and investments made under the old law. Over time, however, deductions attributable to the old law fade out, and the budget costs stabilizes as a share of GDP. This is yet another way in which the ten-year budget window biases against permanent bonus depreciation.

Figure 3. Estimated Budgetary Effects of Option (3), 2025-2034

Option (4): Permanent Full Expensing

This option would eliminate cost recovery altogether and require all investment to be immediately deductible in the same way that other expenses like wages or advertising costs are expensed.1 This scenario differs from 100% bonus depreciation for two reasons—factors which combine to generate much larger budget costs compared with option (3).

First, it would apply to all investment—not just the subset of investment eligible for bonus depreciation. Specifically, buildings and structures would be immediately deductible under this option, but not under options (1)-(3). This means that all investments, across all industries and asset classes, would face the same tax treatment.

Second, expensing would not be optional (which is the case under a system with 100% bonus depreciation). Firms would no longer be allowed to elect to depreciate property under the Modified Accelerated Cost Recovery System (MACRS), simplifying the tax code as firms would no longer need to track deduction over time or do calculations to optimize between choosing section 179, bonus, or MACRS.2

Figure 4. Estimated Budgetary Effects of Option (4), 2025-2034

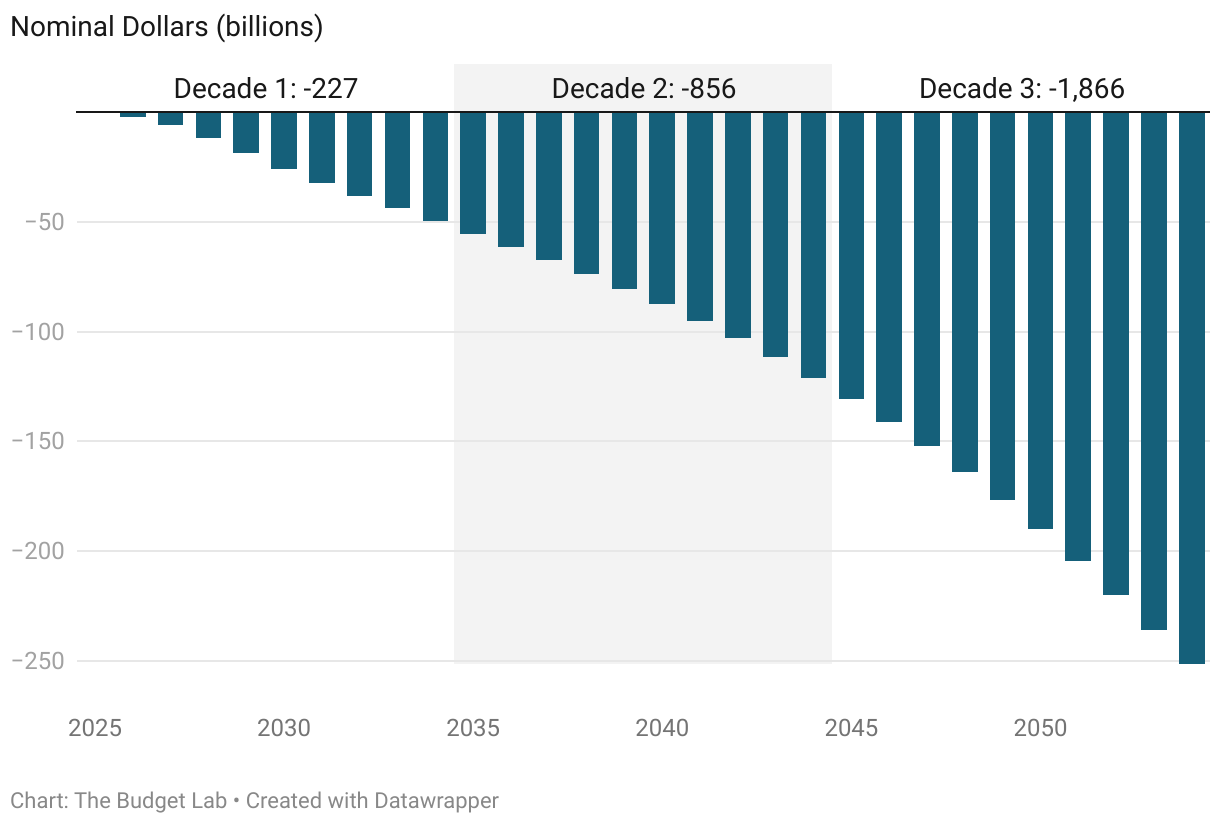

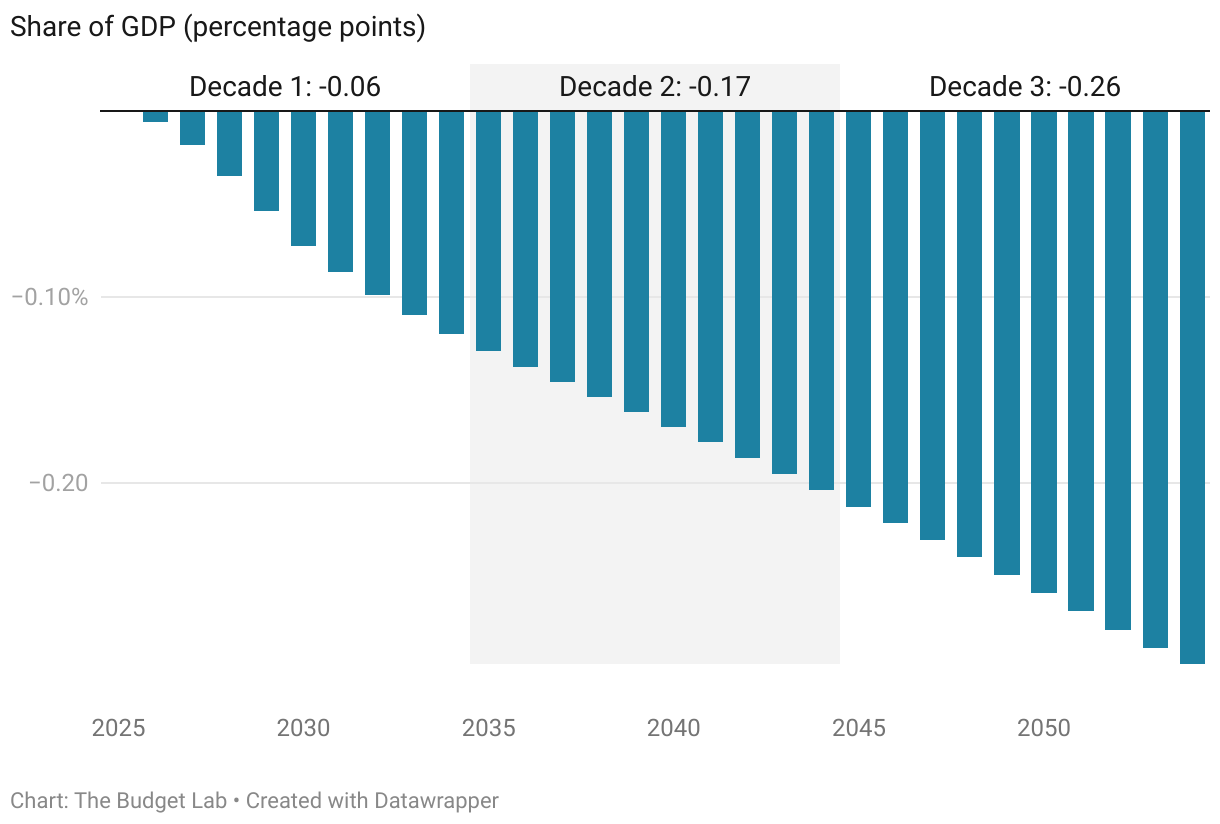

Option (5): Neutral Cost Recovery

Neutral cost recovery refers to any depreciation schedule that allows a firm to fully recoup the cost of its investment in present value terms.3 Option (5) achieves this by indexing MACRS depreciation deductions to the 10-year Treasury yield. In other words, this design sets depreciation schedules such that taxpayers are indifferent to receiving deductions today or in the future, assuming the government’s discount rate.4 This option is designed to provide tax treatment similar to full expensing without the large up-front, transitional costs associated with a one-time switch from depreciation to expensing. For that reason, neutral cost recovery appears cheaper over the ten-year budget window. But these savings, relative to expensing, are transitory, and budget costs actually exceed those of expensing over the longer run (although not in present value) if the indexation rate exceeds the growth rate in investment.

Figure 5. Estimated Budgetary Effects of Option (5), 2025-2034

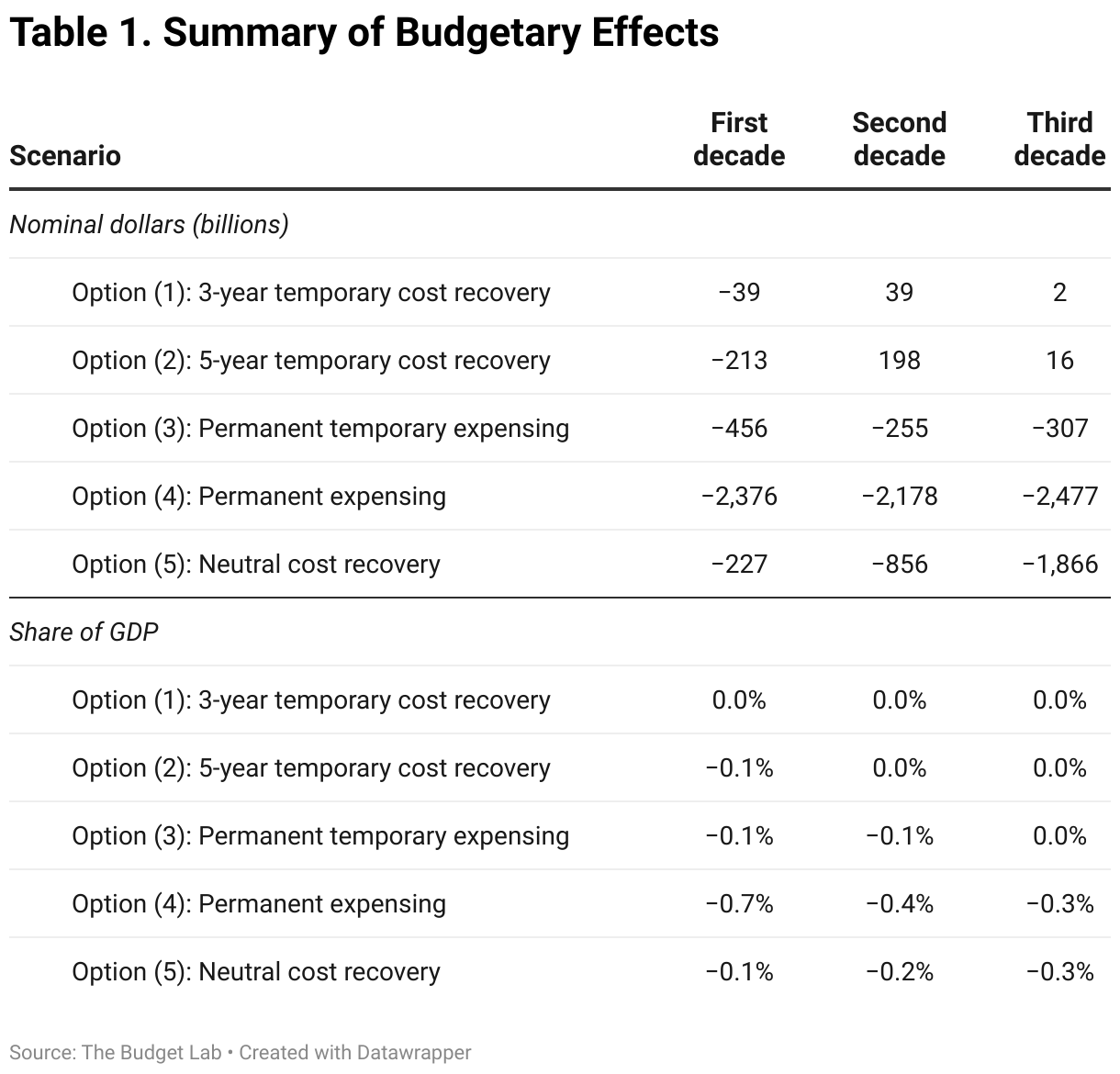

Table 1 summarizes the cost in nominal dollars as well as a percentage of GDP of the policy experiments. As mentioned above, the cost of temporary accelerated depreciation can be recouped within the budget window if designed properly. The table also makes clear that, in deciding between neutral cost recovery and full expensing, policymakers are trading up front cost for long run cost.

Effects of Reform Options by Industry

Businesses prefer deductions sooner rather than later due to the time value of money. The tax code offers a schedule of nominal deductions over time, but those deductions lose value due to inflation and opportunity cost. The longer the depreciation schedule, the more erosion in value due to these factors. For example, under MACRS, tractors are depreciated over three years whereas office buildings take 39 years. Assuming a 6.5% discount rate, one dollar of tractor investment nets 94 cents of future deductions in present value terms; one dollar of office building investment nets just 38 cents. In other words, taxes weigh more heavily on longer-lived assets like office buildings compared to shorter-lived assets like tractors.

This means that depreciation schedules do not affect all industries equally. Industries that disproportionately invest in long-lived assets, such as real estate, benefit most from a move towards faster depreciation schedules. But for industries with lots of investment 3- or 5-year property, the marginal impact is limited. Another factor is asset eligibility: investment in structures is ineligible for bonus depreciation.

Interest rate environment will impact the benefit of bonus depreciation relative to MACRS. When discount rates are lower, for example in the period following the Great Recession, the difference between the two shrinks; when interest rates are higher, for example during recent years as the Fed responds to above-target inflation, the difference is larger."

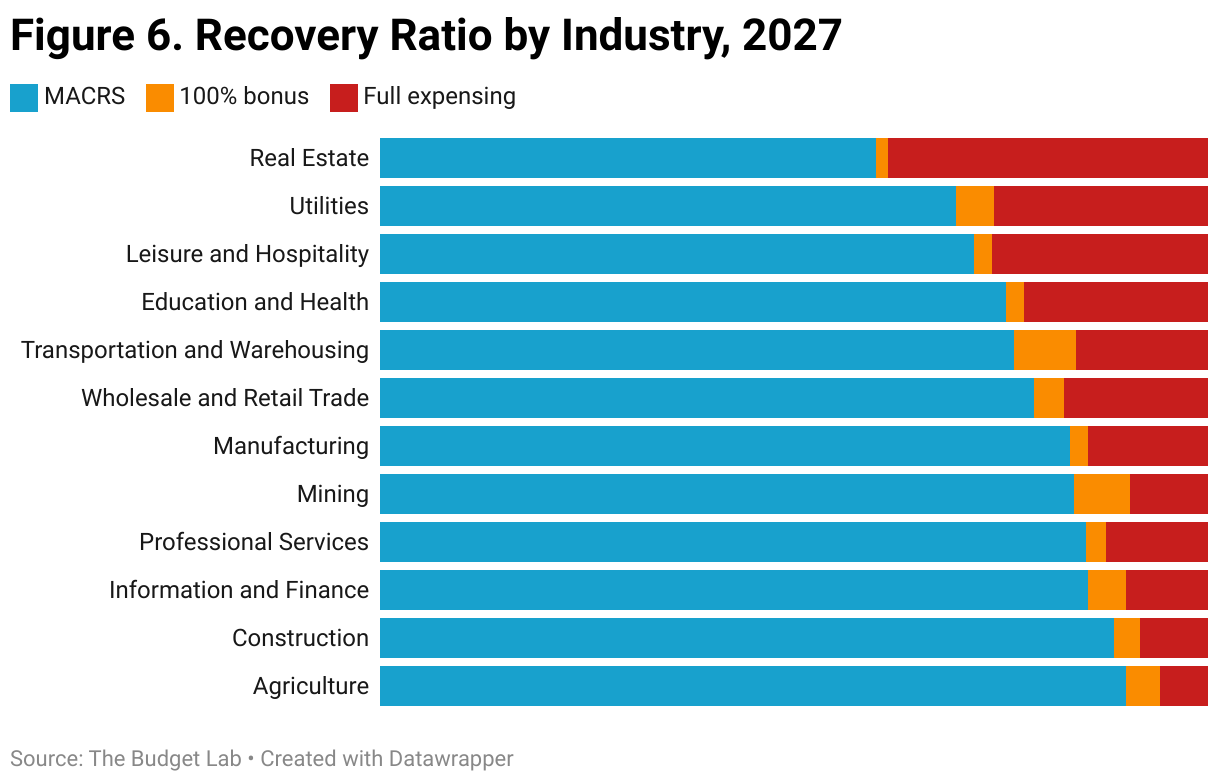

Figure 6 summarizes these factors by looking at the average cost recovery ratio—the present value of depreciation deductions—across industries. It shows ratios under MACRS in 2027, when bonus depreciation is fully phased out. Then, it shows the increase in cost recovery ratios if 100% bonus depreciation were reinstated. The remaining distance to a 100% ratio represents the impact that moving to full expensing would have.

MACRS is least generous to the real estate industry, given its disproportionate investment in residential and commercial buildings with multi-decade asset lives. 100% bonus depreciation is also not much help for this industry because structures are ineligible. On the other side, service-sector industries like professional services and finance tend to invest in short-lived assets, so recovery ratios are comparatively high under MACRS. The same is true of agricultural businesses and construction. Bonus depreciation is most helpful to transportation and warehousing and the mining industry.

Estimated Effect on Investment

Discussion around accelerated depreciation policies each involve the effect on investment. A dynamic score would illustrate the tradeoff between cost and investment in the clearest way. This type of score allows for changes in investment and subsequently, GDP. A conventional score, like those presented above, does not include increases in investment. Allowing for increases in investment violates the fixed GDP convention under which the Congressional Budget Office (CBO) operates for conventional scores.

That said, researchers have been able to estimate the relationship between accelerated depreciation and investment by using past periods of accelerated depreciation. This literature reports that 100 percent bonus depreciation increases investment on eligible assets by 10 to18 percent relative to ineligible assets.5 Smaller effects (~2%) are reported for special 179 depreciation which has a narrower base and involves extra reporting by firms. It is important to note that these estimated effects do not reflect the effects of full expensing. The latter policy has never been in place in the US and therefore, projecting the increase in investment due to this policy will necessarily include an adaptation of elasticities estimated over other policies or use a dynamic macroeconomic model.

Researchers have also noted that the circumstances of firms play an important role in the effectiveness of these policies. A significant factor is whether the policy creates immediate cashflow for the firm. That is, firms with NOLs are less likely to react to the change in allowances and therefore, diminish the effect of the policy. Additionally, the choice of policies should consider the economic conditions in place. In times of diminished demand, accelerated depreciation policies are likely to have a smaller impact (closer to the 2% end of the range) on investment. The expectation that temporary policies are permanent also affects the size of the increase in investment. For permanent policies, there is no incentive to move investment forward to take advantage of the additional allowances. However, a policy that is expected to be temporary will have a larger effect as firms move investment forward. This result is also noted in the literature. However, the largest change in investment is likely to occur when firms do not have NOLs, and they receive the full cost of investment in depreciation deductions.

Of the policies presented above, full expensing and neutral cost recovery are likely to have the largest effect on investment given the policies exactly offset the cost of investment. Any difference in outcomes between these two policies is likely to be due to the difference in timing of the cost. The effects of truly temporary bonus depreciation policies are likely to be on the lower end of the estimated range. This is because the largest effects coincided with the recession. The current economic environment is not a recession, and temporary provisions will have little effect (aside from pure timing shifts). Permanent bonus policies will lead to larger investment and have a greater effect than the temporary policies.

Conclusion

Ultimately, the choice of depreciation policies will weigh the desire to lower tax rates on new investment with the appetite for an increase in the deficit. Temporary policies that allow for immediate expensing on certain assets have low costs and can net to zero within the budget window. However, those low costs are particularly misleading if the temporary policy is made permanent through extensions. Permanent policies that allow the same have larger upfront costs, but those costs can be addressed by indexing depreciation deductions to reflect the present value of those deductions. Permanent policies also have the advantage that the cost stabilizes as a share of GDP over time- a fact often hidden by ‘budget-window’ conventions.

Footnotes

- To avoid negative tax rates, this policy would require the additional coordinating policy of disallowing net interest deductions.

- Kitchen and Knittel (2016) found that only between 40 and 60 percent of firms eligible to use bonus depreciation actually used it between 2002 and 2014.

- Full expensing is technically an instance of neutral cost recovery because the firm receives the tax savings immediately.

- Firms likely face higher borrowing costs than the government, though these vary by firm and investment. This version of the policy can be thought of as neutral with respect to the risk-free return.

- See Zwick, Eric, and James Mahon. 2017. "Tax Policy and Heterogeneous Investment Behavior." American Economic Review, 107 (1): 217–48; Kitchen, John, and Matthew Knittel. October 2016. “Business Use of Section 179 Expensing and Bonus Depreciation, 2002-2014" Office of Tax Analysis Working Paper 110; Ohrn, “The effect of tax incentives on U.S. manufacturing: Evidence from state accelerated depreciation policies,” Journal of Public Economics, Volume 180, 2019; Gravelle, Jane. October 2014. “Bonus Depreciation: Economic and Budgetary Issues,” Congressional Research Service Report.