Budgetary Effects of the May 2025 Tax Bill (Preliminary)

Key Takeaways

-

As written, the tax bill under consideration by the House would add $3.4 trillion to the debt over the 2025-2034 window and $15.3 trillion from 2025-2055.

-

If temporary provisions became permanent, the cost over the 2025-2034 window is $5.0 trillion and over the 2025-2055 window is $23.7 trillion. ($2.5 trillion and $13.5 trillion respectively, if possible tariff revenue is taken into account).

-

If the provisions become permanent, the debt-to-GDP ratio would hit 200 percent in 2055. The only countries that currently have a higher debt-to- GDP ratio are Sudan and Japan.

Summary

This report analyzes the legislation under consideration by the House Ways and Means Committee as part of the current reconciliation process. The proposals primarily extend and enhance the tax provisions in the 2017 Tax Cuts and Jobs Acts (TCJA) that are set to expire at the end of 2025. The proposals also include versions of several policies put forth by the President during the presidential campaign.1

This score reflects the provisions under the jurisdiction of the Ways and Means Committee, which will comprise the bulk of the bill. The Budget Lab will update our score in coming weeks with more details about the portions of the bill that are under the jurisdiction of other committees.

Note: this analysis looks merely at the conventional score for these proposals. In this analysis we do not look at the distributional implications of this proposal or its macroeconomic implications. We thus do not account for any additional growth (or slowing down of growth) that may emerge in the short-run or long-run from passing this bill, nor do we analyze the impact of the increased debt burden on interest rates. We are also narrowly focused on the tax provisions in the House Ways and Means Committee’s portion of the Budget Reconciliation process. Budget Lab is working on additional analyses on these topics and on provisions from other committees not included in the Ways and Means text.

There is important recent work that estimates the budgetary impact of the House legislation.2 Our estimates are within 8% (~300 billion) of the Joint Committee on Taxation’s own estimates in the ten-year budget window. But our focus is different: we are providing a longer-term lens on the likely impact of the proposed tax changes on the fiscal situation.

Because the tax provisions are designed to fit within the $4.5 trillion allowance set by the 2025 budget resolution, many are temporary in nature. Given how unusual it is for Congress not to allow these policies to be extended (as seen in the current debate over the expiring provisions from 2017), we also offer a long-term lens should those policies be extended permanently.

- The baseline cost of the bill as written, assuming temporary provisions actually expire, over the 2025-2034 window is $3.4 trillion and over the 2025-2055 window is $15.3 trillion.

- If tariff revenue reflecting the state of tariffs as of May 12th was included, the cost would be $913 billion over the 2025-2034 window and $5.1 trillion over the 2025-2055 window.

- If we assume that the temporary provisions become permanent (in other words if we assume that lawmakers keep extending these provisions), the cost of the bill over the 2025-2034 window years is $5.0 trillion and over the 2025-2055 window is $23.7 trillion.

- If possible tariff revenue was included, the cost would be $2.5 trillion over the 2025-2034 window and $13.5 trillion over the 2025-2055 window.

Note that the bill as written adds to the deficit in the outyears. This would not be consistent with reconciliation rules unless the Senate either rewrites the bill or changes how bills are evaluated as being consistent with reconciliation rules.

Analysis

Nominally, the purpose of the budget reconciliation is to extend the tax provisions established in the TCJA with more than 85% of the total net cost. These provisions include lower individual rates, increased standard deduction, a larger Child Tax Credit (CTC), and a deduction for qualified business income (QBI).

However, there are a substantial number of new tax-related provisions in the bill, including MAGA accounts, which would allow parents to give more money to their children tax-free, the removal of the excise tax on firearms, and an increase in the SALT limit to $30,000 (accompanied by income limits). It also includes several of the President’s campaign promises such as “no tax on tips,” “no tax on overtime,” and a larger standard deduction for older Americans (presumably to act as a version of “no tax on Social Security”). The bill includes offsets through repealing or phasing out Inflation Reduction Act energy credits, imposing new taxes on foreign corporations, and restricting ACA subsidies. The budget resolution included instructions for spending cuts, to help offset the tax cuts, concentrated in SNAP and Medicaid, which are not analyzed here as they are not part of the Ways and Means text.

Conclusion

The bill as currently proposed would substantially add to the deficit, even if accounting for possible tariff revenue. If we account for the likelihood that these provisions would become permanent, at the end of 30 years the debt-to-GDP ratio would be over 180 percent, even assuming substantial revenue from tariffs. For context, the only countries with a higher debt-to-GDP ratio currently are Japan and the Sudan. The debt-to-GDP ratio would be higher than that currently held by Singapore and Venezuela.

While the impact on the deficit and the debt is not the only important factor to consider in evaluating the impact of this bill, our analysis shows that the impact of this bill on the fiscal picture of the nation would be substantial. Assuming temporary provisions expire, the bill's baseline cost of $3.4 trillion would make it the largest spending package in US history. For context, this price tag would surpass the inflation-adjusted cost of the CARES Act ($2.64 trillion) and the American Rescue Plan ($2.18 trillion).

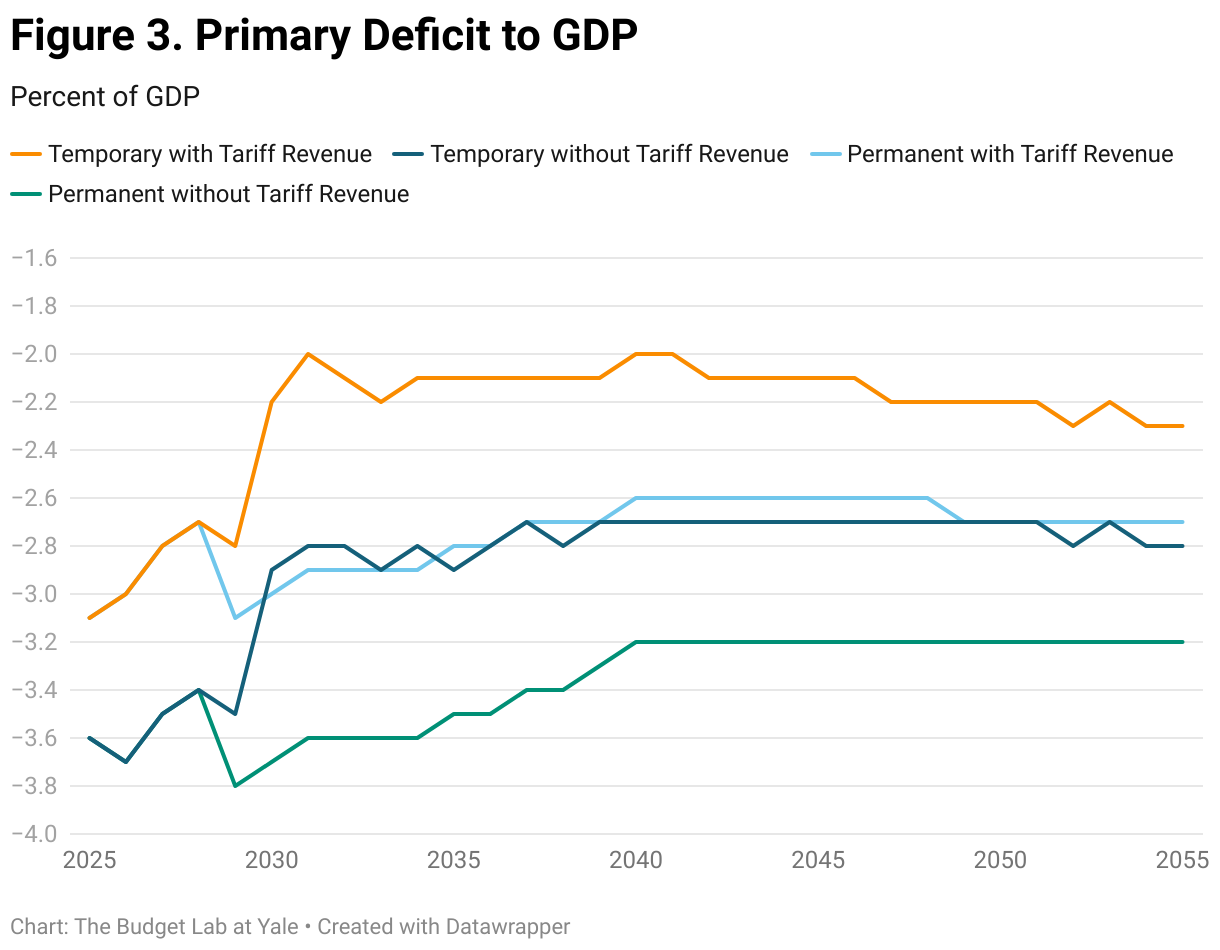

Figures: Effects on Debt and Deficits

Footnotes

- The Budget Lab does not attempt to summarize in this score all the provisions that are in the bill. For a summary from The Bipartisan Policy Center please see here.

- See CRFB, Bipartisan Policy Center, Tax Foundation, and Tax Policy Center among others.