The Fiscal, Economic, and Distributional Effects of a 20% Broad Tariff

Key Takeaways

-

The Budget Lab modeled the total effect of an illustrative 20% broad tariffs. It is highly uncertain whether this is the policy that will be announced April 2.

-

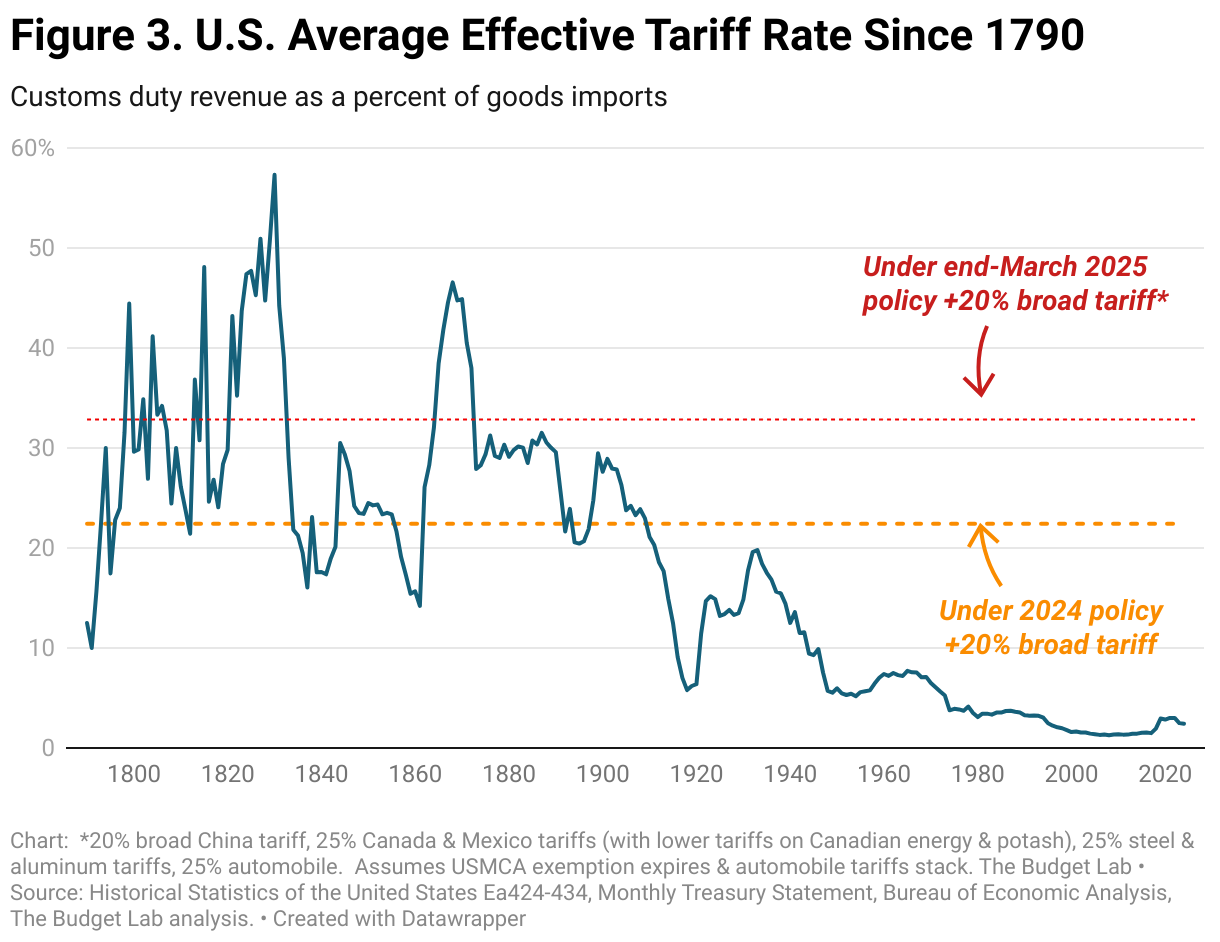

Including the other tariffs that have gone into effect this year, the average effective US tariff rate rises to 32.8%, the highest since 1872.

-

The price level rises by 2.1-2.6% in the short run, the equivalent of an average per household consumer loss of $3,400-4,200 in 2024$.

-

US real GDP growth is 0.9-1.0pp lower in 2025. In the long-run, the US economy is persistently 0.3-0.6% smaller, the equivalent of $90-180 billion annually in 2024$.

-

World GDP is smaller in the long-run as well, though China’s GDP is largely unscathed.

-

The tariff raises $3.1-4.1 trillion over 2026-35 conventionally-scored, and $450-550 billion less if dynamic revenue effects are taken into account.

-

Tariffs are regressive taxes. Annual losses for households at the bottom of the income distribution would range between $1,900–2,400 in 2024$.

-

Food prices rise 3.7%, about double the recent rate of grocery inflation. Computers, clothing, and crops all see double-digit percentage price increases.

Introduction

On March 30, the Wall Street Journal reported that the Trump Administration was considering a 20% broad tariff on all imports as the substance of its planned April 2 action. It is still highly uncertain whether or not this constitutes the final proposal, however. This analysis presents the fiscal and economic effects of an illustrative 20% broad tariff in isolation, without considering the other tariffs that have gone into effect so far this year. The Budget Lab (TBL) modeled these tariffs under two assumptions: “no retaliation”, in which the other countries do not levy any new tariffs of their own on U.S. exports, and “full retaliation”, where they all levy reciprocal 20% tariffs on all U.S. exports. TBL assumed the 20% broad tariff stacked on top of all other tariffs already in place. Its methodology largely follows prior tariff analysis.

Results

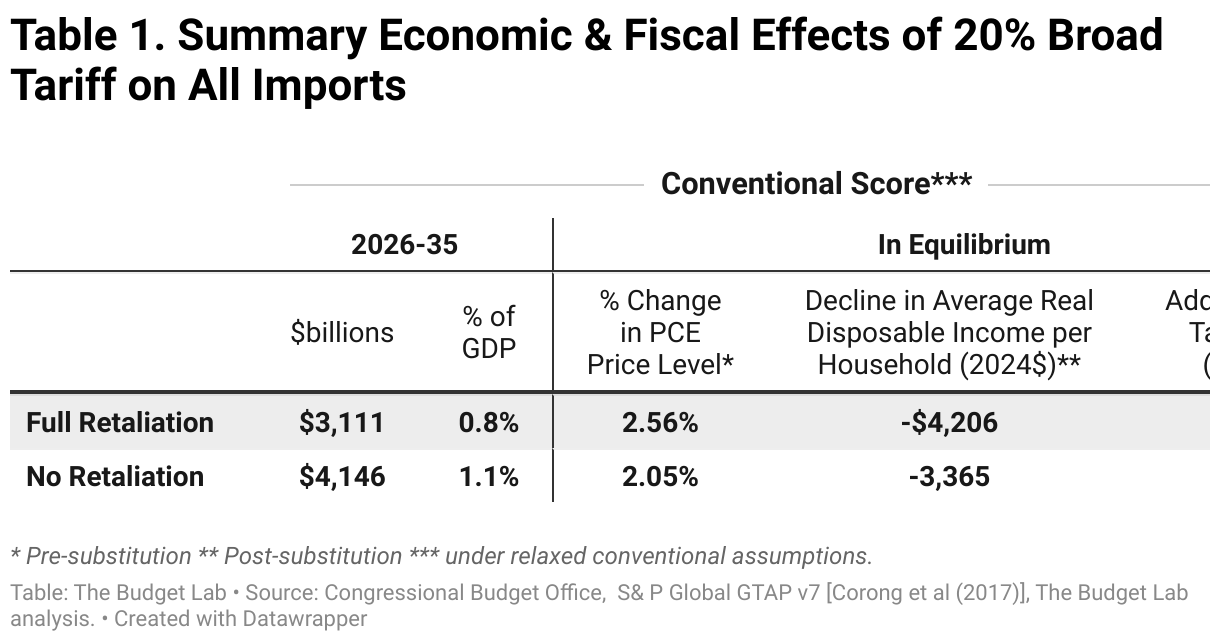

The table below summarizes TBL’s fiscal and economic results.

- Average aggregate price impact. A 20% broad tariff would raise consumer prices by between 2.1% (no retaliation from other countries) and 2.6% (full tit-for-tat retaliation) in the short-run, assuming no policy reaction from the Federal Reserve. This is equivalent to a loss of purchasing power of $3,400-4,200 per household on average in 2024 dollars. The primary difference between the scenarios is that the dollar appreciates when the US imposes unanswered tariffs, which offsets the impact to consumers somewhat but punctuates the impact on US exporters, whose goods become more expensive overseas with a stronger dollar. When other countries retaliate against the US with their own tariffs, however, they sterilize this dollar effect, and US consumers bear the full burden of the tariff.

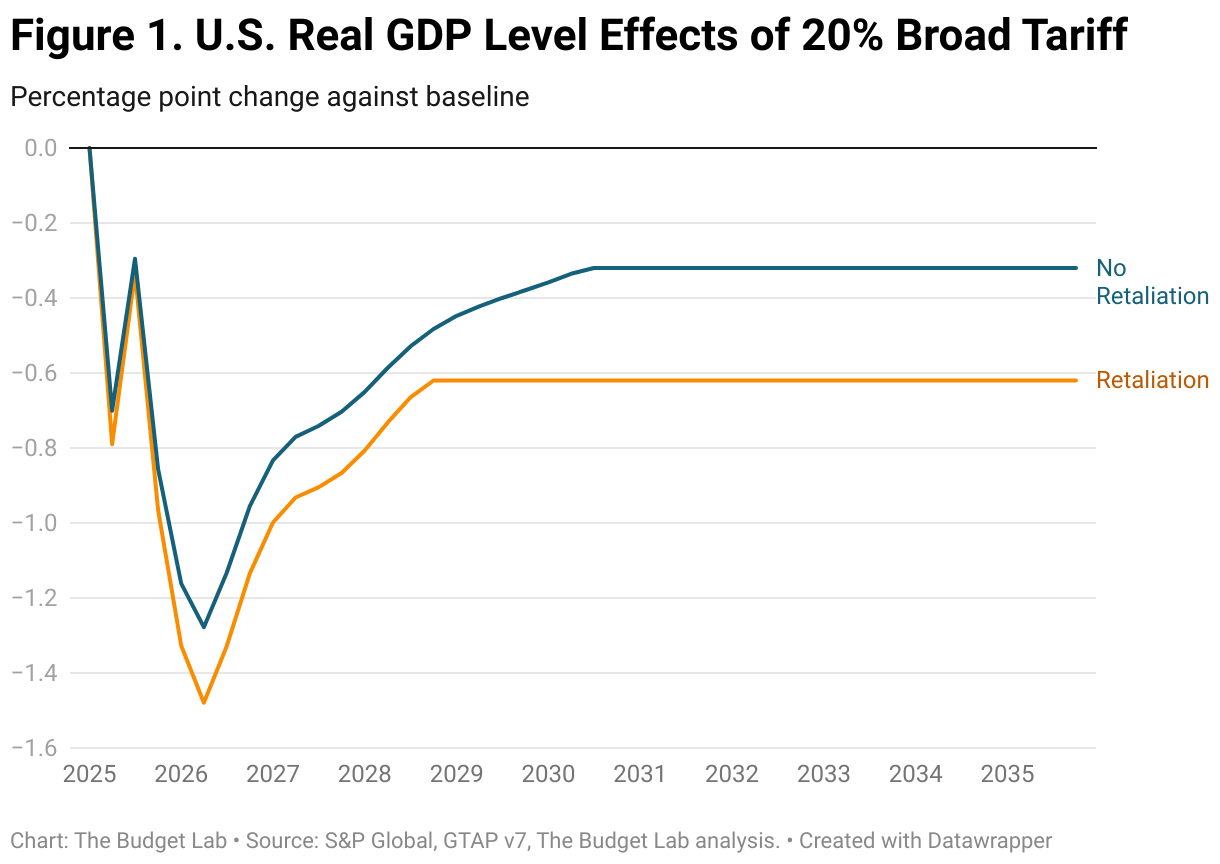

- US real GDP effects. The tariffs reduce the size of the US economy in both the short- and the long-run. US real GDP growth is -0.9pp to -1.0pp lower in calendar year 2025 and -0.1pp to -0.2pp lower in calendar year 2026 under the no-retaliation and full-retaliation scenarios, respectively. After 2026, the level of GDP begins to recover modestly as production and supply chains reoptimize. But in the long-run, US output is still -0.3% to -0.6% lower. That’s the equivalent of the US economy being permanently smaller by $90-$180 billion annually in 2024 dollars. In particular, real exports are lower in the long-run under both scenarios: -21% under no retaliation and -26% under retaliation. Exports fall even without retaliation because the dollar strengthens, making US goods and services less price competitive overseas.

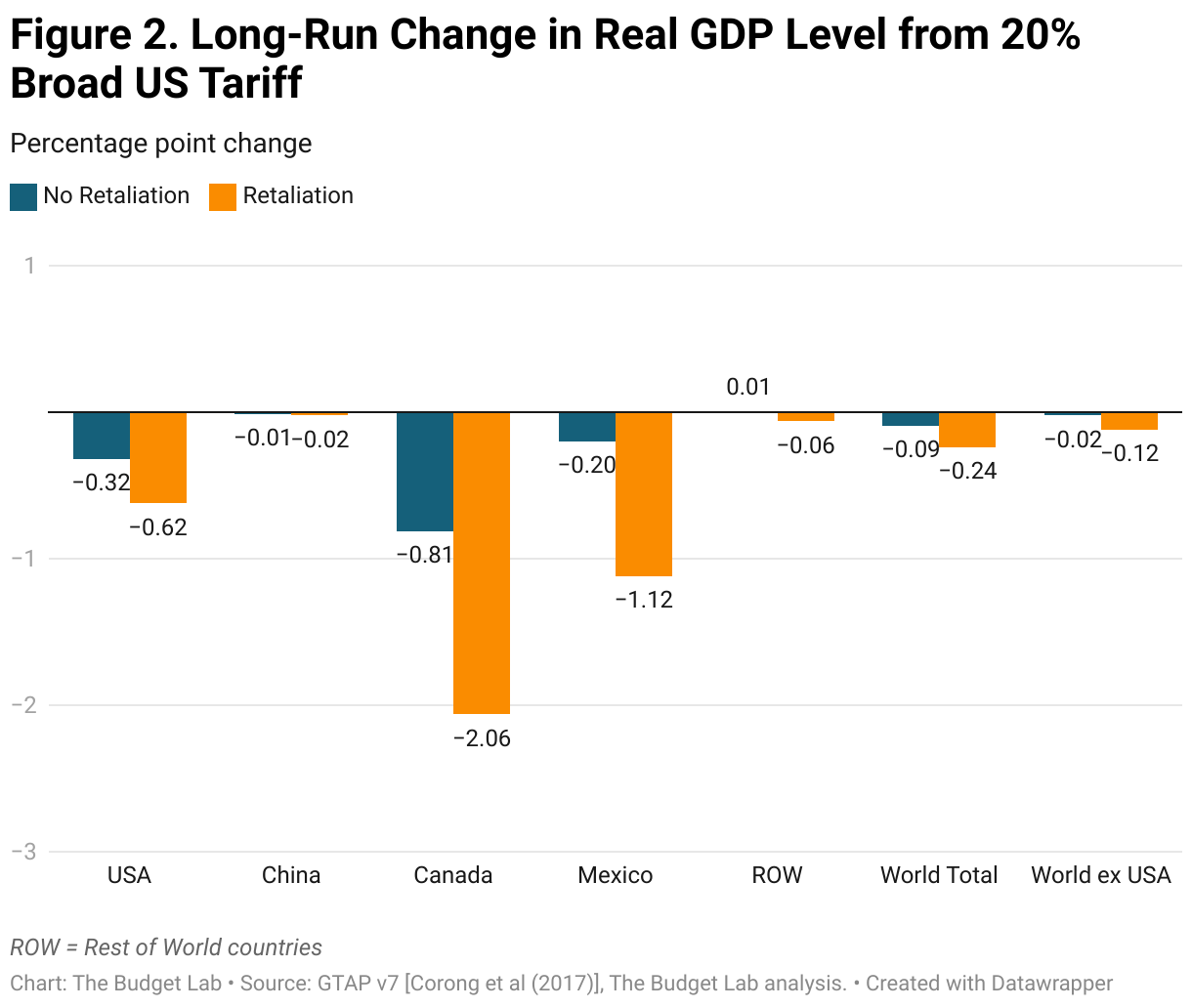

- Global long-run real GDP effects. Net-net, the world is worse off as a result of the tariffs. Our modeling shows that in the long-run, global output in 0.1-0.25% smaller under the no-retaliation and full-retaliation scenarios, respectively. Some countries fare better than others: China for example barely sees their output fall, by 0.01-0.02%, as they benefit from shifts in global trade and production, which offsets most of the negative effects of the tariffs on their economy. Canada and Mexico meanwhile see more economic pain. Canada in particular experiences more than twice the long-run output loss as the US does in either scenario (-2.1% versus -0.6% under retaliation; -0.8% versus -0.3% under no retaliation). The damage to Mexico’s economy is somewhat smaller: Mexico sees less of a GDP hit than the US does under no retaliation, but almost twice as much under retaliation.

- Fiscal impact & historical context. The 20% broad tariffs, were they to remain in place, would raise $3.1-4.1 trillion over 2026-35 conventionally-scored, with the lower end representing the full retaliation scenario.1 Given the negative output effects of the tariffs to date, there would be additional dynamic reductions in tax revenue as a result. Based on Congressional Budget Office rules-of-thumb, TBL estimates that these effects would range between $550 billion under full retaliation to $450 billion with no retaliation. Judged against 2024 policy, the new tariffs would have raised the average effective tariff rate to 22 ½%, the highest rate since 1910. Judged against where tariff policy stands at the end of March 2025 fully phased-in,2 the effective tariff rate rises to 32.8%, the highest since 1872.

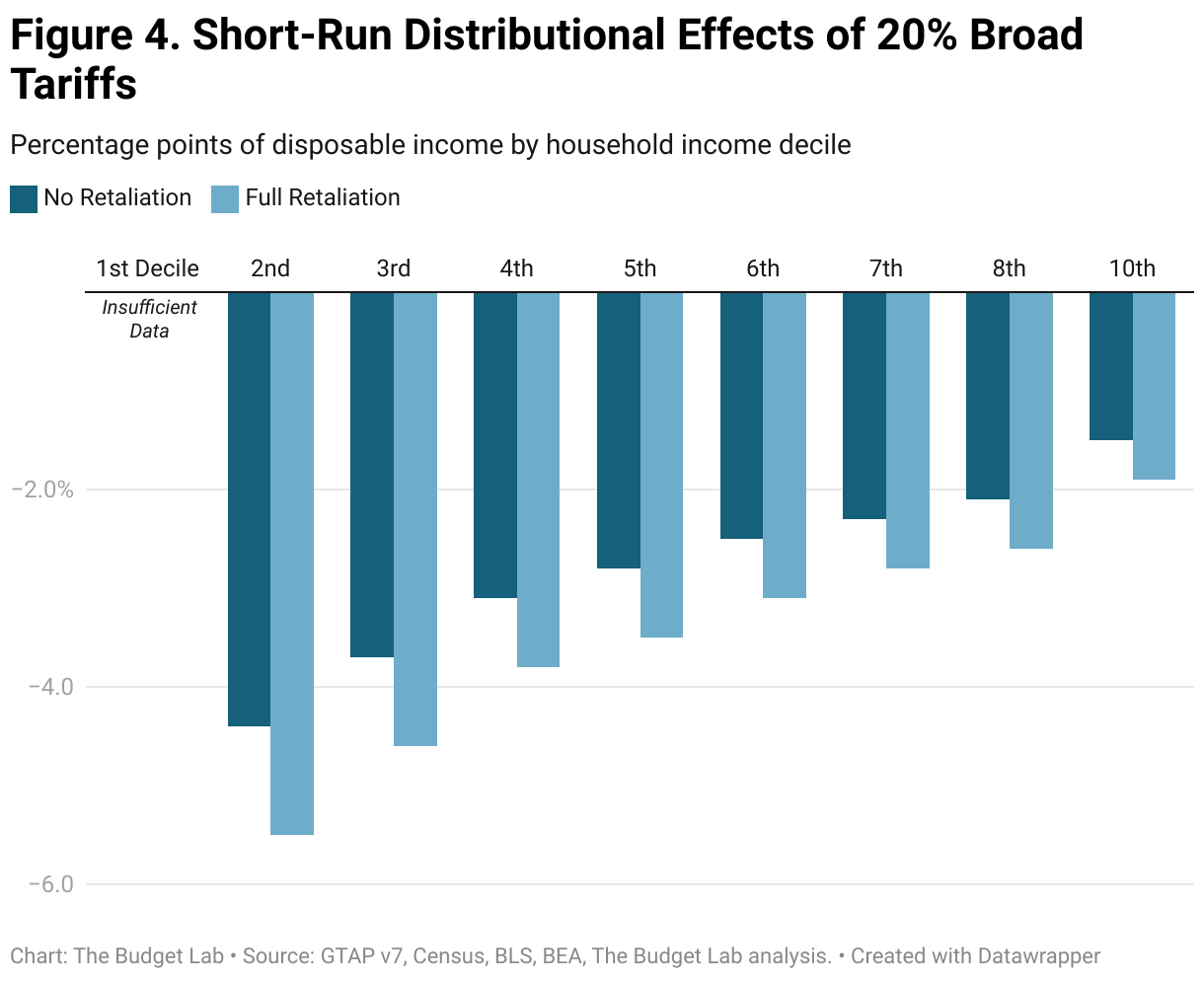

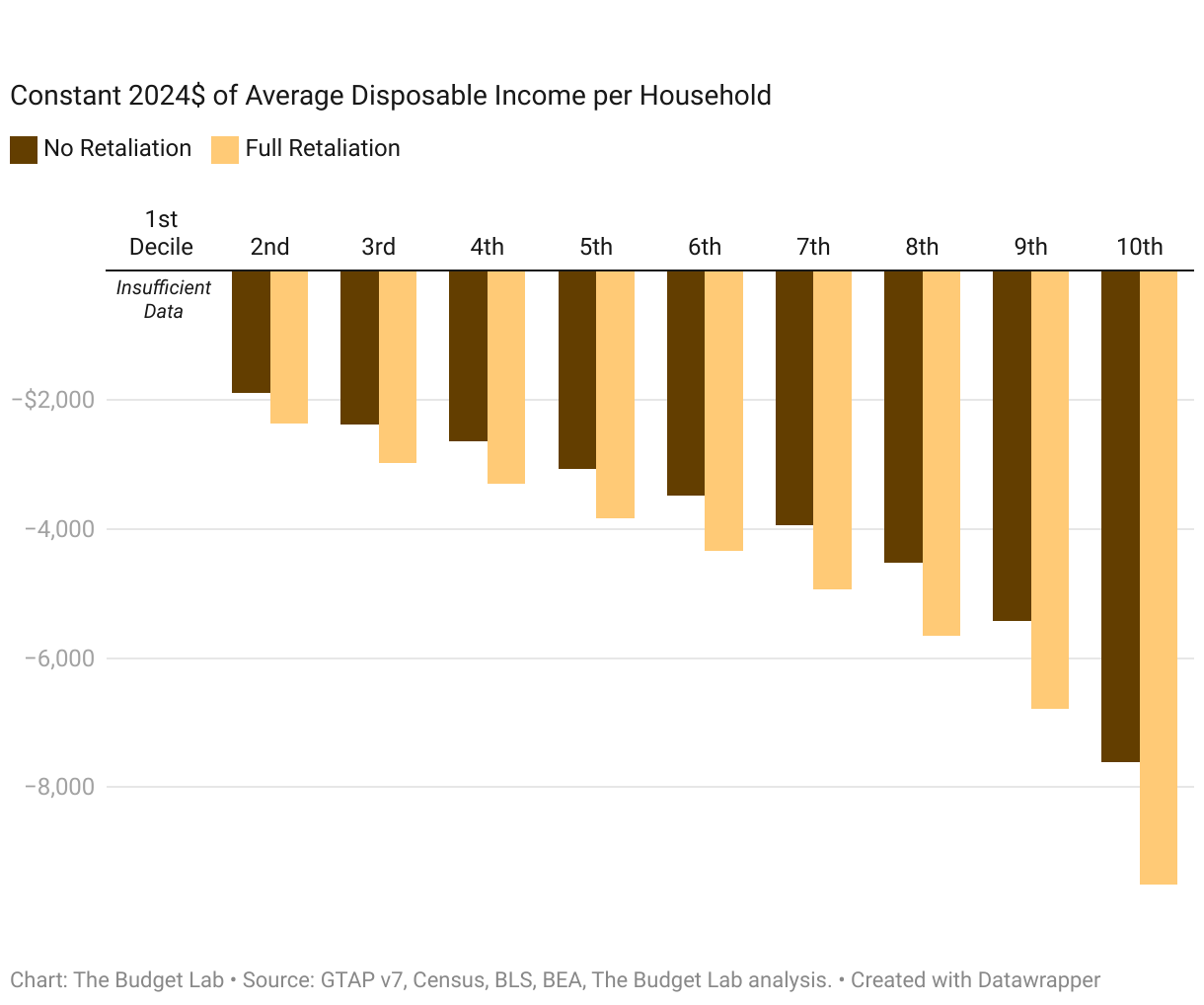

- Short-run distributional impact. Tariffs are a regressive tax, especially in the short-run. This means that tariffs burden households at the bottom of the income ladder more than those at the top as a share of income. The percent change in disposable income resulting from the broad tariffs is nearly 3x as much for households in the second decile by income as it is for households in the top decile: -5.5% versus -1.9% in the case of tariffs with full retaliation (see top panel of chart below). Because income rises across the distribution more steeply than the tariff burden falls, the tariff burden in dollar terms is higher at higher incomes (bottom panel). For a household in the second lowest income decile, the tariff proposal leads to consumer loss of $2,400 per household on average when other countries retaliate. For households in the middle, the burden rises to $3,800 per household on average, and for those in the top tenth, it averages $9,500 per household.

Tariffs are more distributionally-ambiguous in the longer-run. Tariffs reduce both labor income and above-normal returns to capital, or rents. We assume that owners of capital hold rents rather than consume them in the short-run, but consume them over their lifecycle in the long-run. The implication is that the tariff burden is more regressive in the short-run and more evenly-distributed across households in the long-run

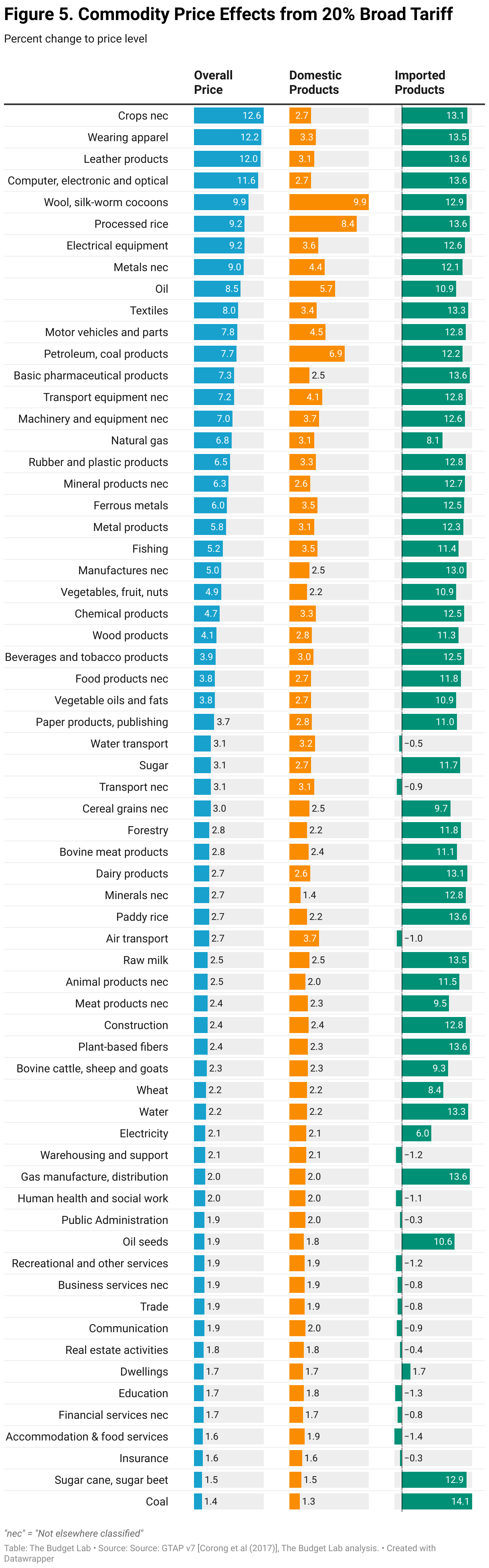

- Commodity price effects. The chart below shows how the 2.6% price level increase would look across individual commodities. Some high level takeaways:

- The products with the top seven price impacts in percent terms are either food (crops, processed rice), clothing, or electronics.

- Food prices on average rise 3.7%; for comparison, CPI food at home prices over the 12 months ending in February 2025 grew 1.9% (roughly half the tariff effect). Crop prices alone rise 12.6%. Fresh produce (“vegetables, fruits, and nuts”) rises 4.9%.

- Oil prices rise 8.5%; refined petroleum products like gasoline rise 7.7% in price.

- Auto prices rise 7.8% (TBL assumed the 20% broad tariff stacked on top of previously-announced auto tariffs). For the average new car sold in 2024, this would be the equivalent of an extra $3,700 to the price, with foreign cars and cars with high foreign content relatively more exposed.

Footnotes

- TBL employs a “relaxed conventional” assumption for the retaliation scenario, whereby foreign income is permitted to fall but US income remains fixed.

- That is, assuming the USMCA exemption for the Canada and Mexico tariffs expire.