The Fiscal, Economic, and Distributional Effects of 25% Auto Tariffs

Key Takeaways

-

The Budget Lab modeled the total effect of the planned 25% automobile tariffs.

-

Motor vehicle prices rise by 13.5% on average, the equivalent of an additional $6,400 to the price of an average new 2024 car.

-

The price level rises by 0.3-0.4%, the equivalent of an average per household consumer loss of $500 - 600 in 2024$.

-

If other countries retaliate, US motor vehicle & parts production shrinks slightly, by -0.04%, while auto production in China, the UK, and the EU rises. If other countries do not retaliate, real US motor vehicle & parts production is 13.7% larger in the long-run.

-

Even under the no-retaliation scenario, however, overall real GDP growth is 0.1 lower in 2025. In the long-run, the US economy is persistently 0.05% smaller, the equivalent of $12-16 billion annually in 2024$.

-

The automobile tariffs raise $600-650 billion over 2026-35 conventionally-scored, and $85-115 billion less if dynamic revenue effects are taken into account.

-

Tariffs are regressive taxes. Annual losses for households at the bottom of the income distribution would range between $450 – 550 in 2024$, averaged across families that both do and do not purchase an automobile.

Introduction

On March 26, the Trump Administration announced 25% tariffs on all imported automobiles and automobile parts, with certain exceptions for U.S.-made content in imports. This would come on top of the new 20% China tariffs, the 25% steel & aluminum tariffs, and the Canada & Mexico tariffs1 that have already gone into effect so far this year.

This analysis presents the fiscal and economic effects of the 25% auto tariffs in isolation. The Budget Lab (TBL) modeled these tariffs under two assumptions: “no retaliation”, in which the other countries do not levy any new tariffs of their own on U.S. auto exports, and “full retaliation”, where they levy reciprocal 25% tariffs on U.S. autos. TBL’s methodology largely follows prior tariff analysis.

Results

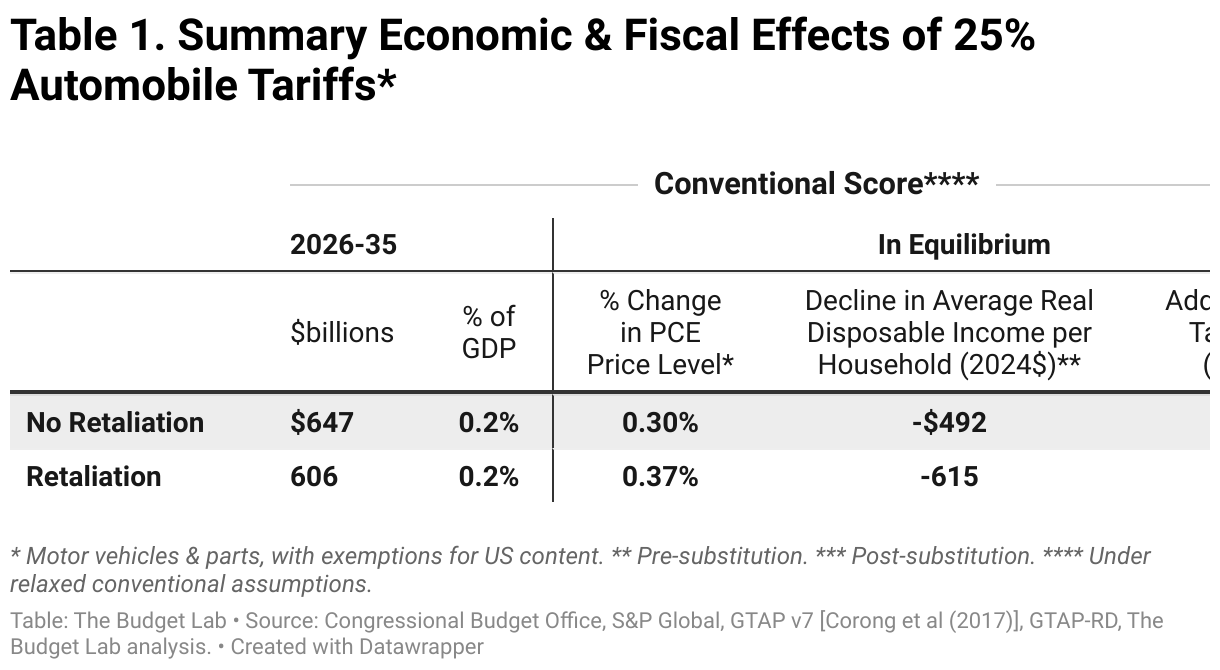

The table below summarizes TBL’s fiscal and economic results.

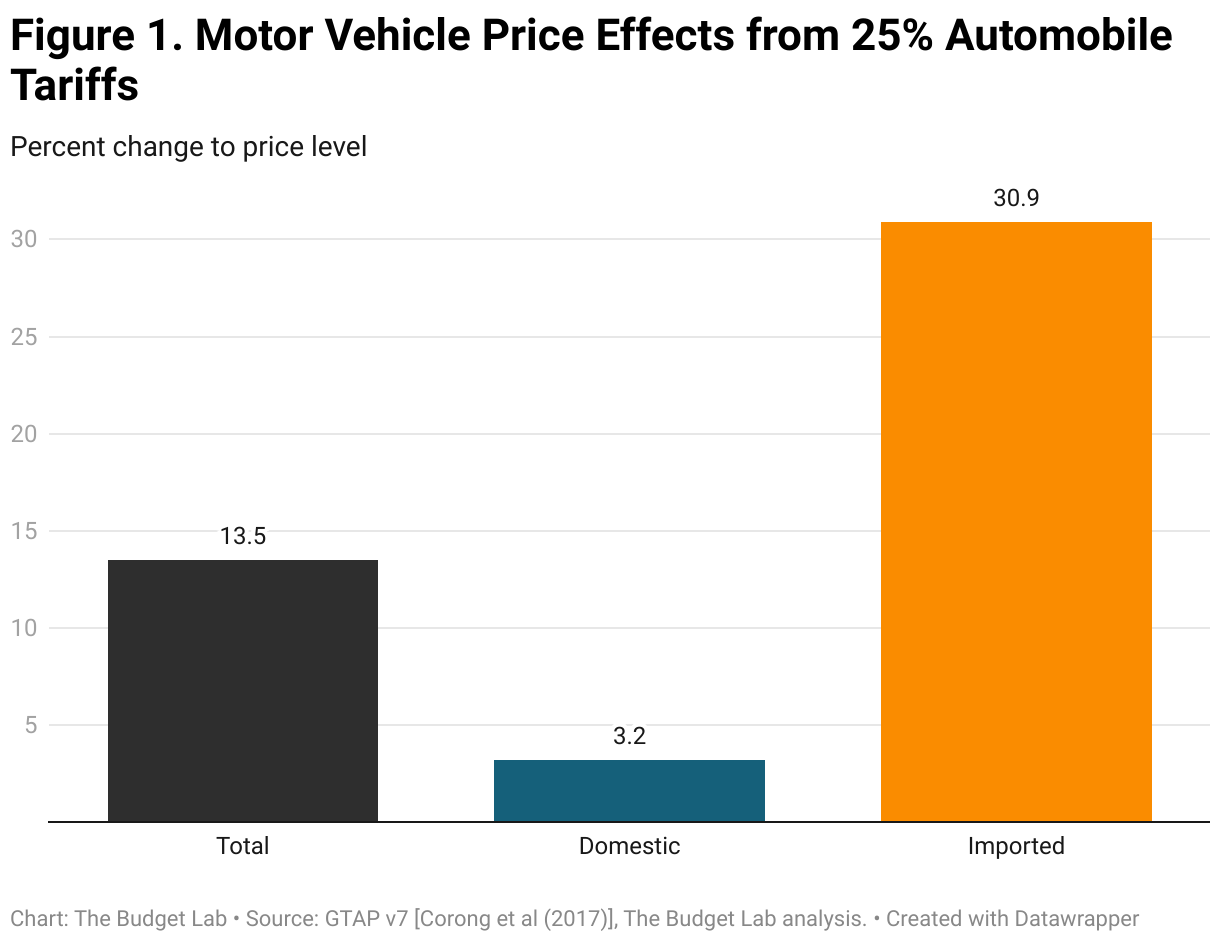

- Motor vehicle price impact. Automobile prices rise 13.5% overall on average as a result of the action (see chart below). Edmunds reports that the average price of a new car in the US was roughly $48,000 in 2024 Q3. The tariff effect would therefore be the equivalent of $6,400 added to the price of an average car. Imported models or domestic models with high import content could see increases higher than the average: imported models alone rise in price by 31% according to TBL’s modeling.

- Average aggregate price impact. The overwhelming effect on overall prices comes from the tariff’s effect on motor vehicle prices, unsurprisingly. In aggregate, PCE prices rise by 0.3% in the short-term under limited retaliation and by 0.4% under full retaliation, assuming the Federal Reserve does not respond (in either direction) to the tariffs’ economic effects. This is equivalent to a consumer loss of $500-600 per household on average in 2024 dollars.

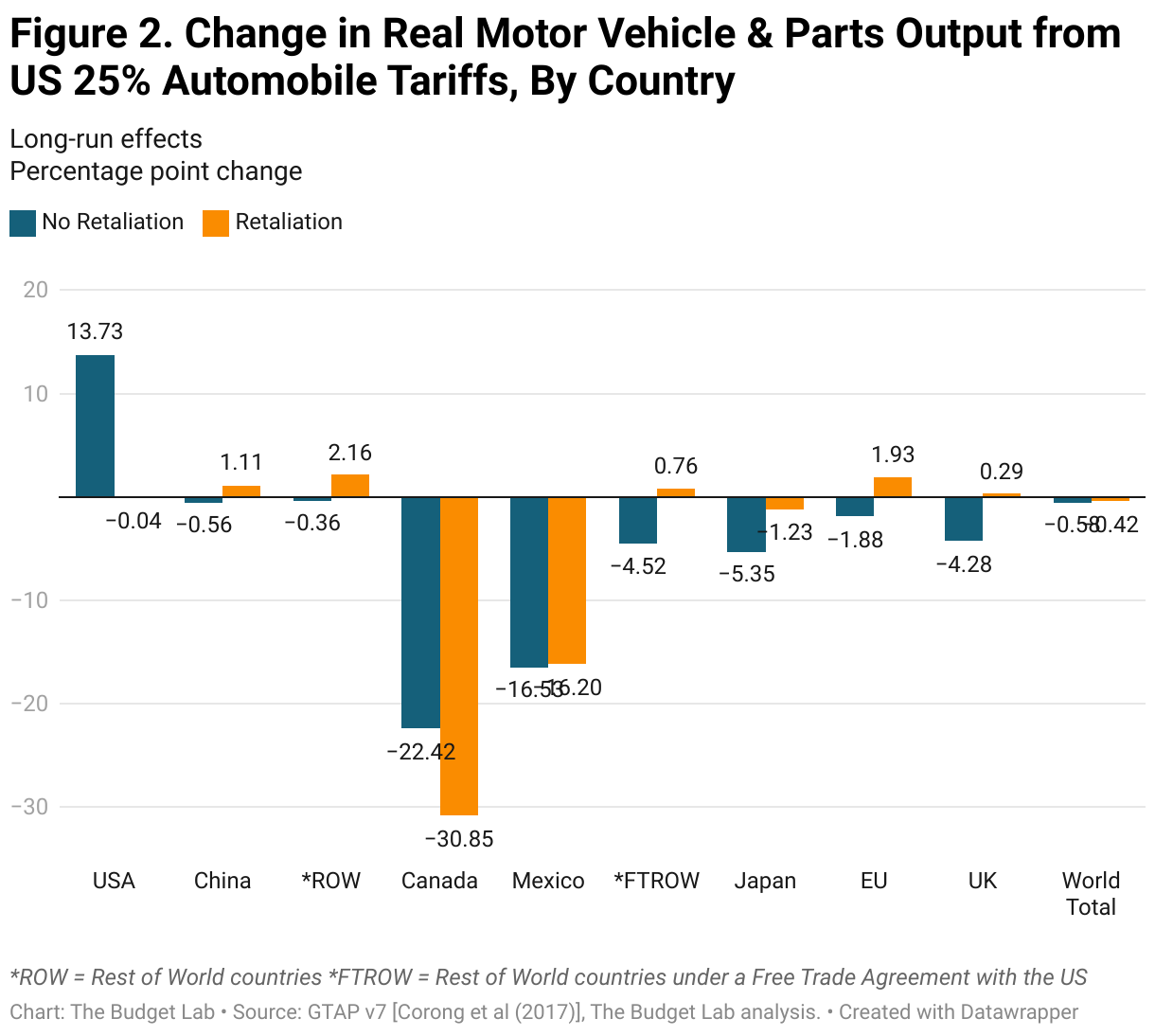

Motor vehicle output effects. One of the policy goals of the tariff is to revitalize US automobile manufacturing. Our modeling shows that, in the event other countries retaliate tit-for-tat to the US auto tariffs, the domestic US auto industry shrinks modestly, with output contracting by -0.04%, the equivalent of the 2024 US auto industry producing 4,000 motor vehicles a year less and shedding about 500 jobs.2 Not every country fairs poorly under an auto trade war: China, the EU, and the UK all see higher automobile output under the retaliatory scenario. In all however, world auto production contracts -0.4%.

If other countries do not retaliate to the tariffs at all, real (inflation-adjusted) US motor vehicle & parts production jumps by almost 14%. That would be the equivalent of the 2024 US auto industry producing roughly 1.3 million more cars and increasing employment by more than 150,000. Most of this represents production that has shifted from Canada and Mexico.

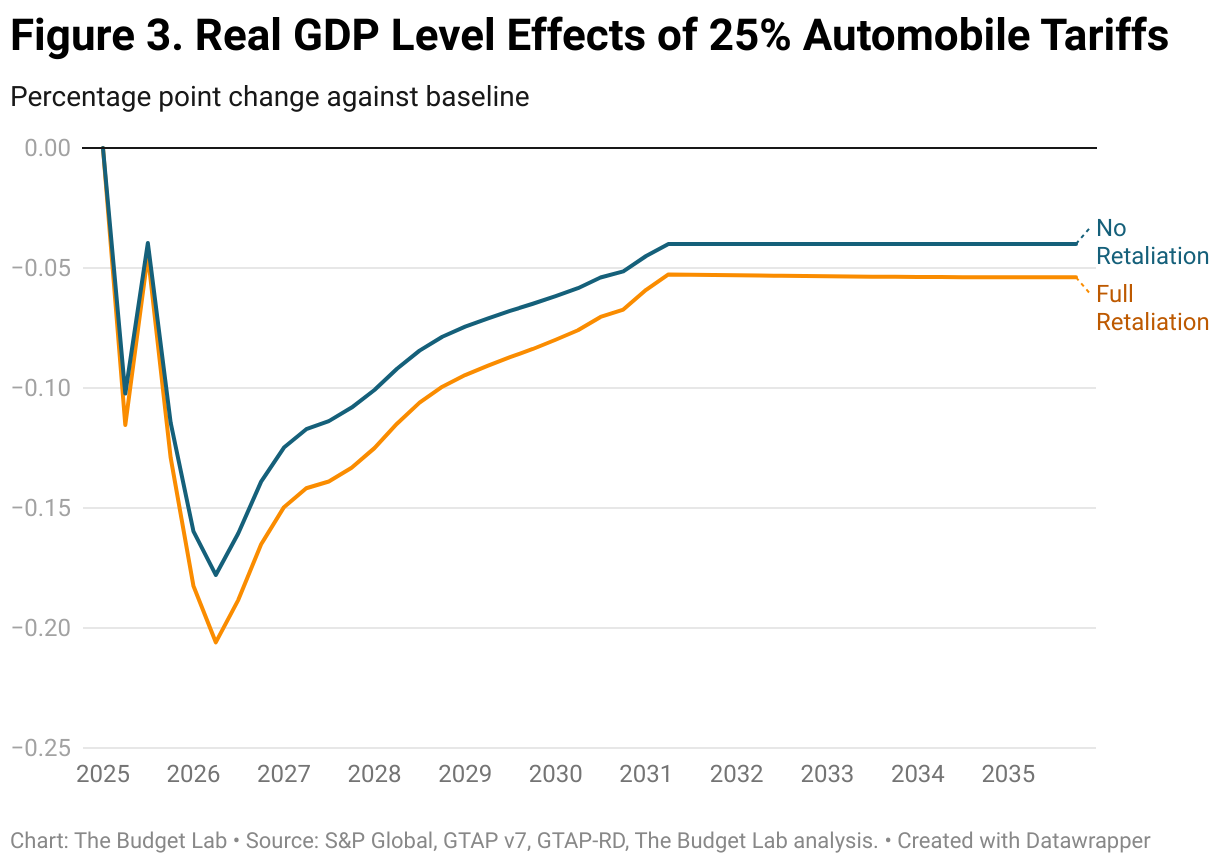

- Aggregate Output effects. Even under the no-retaliation scenario, however, the tariffs reduce the short- and long-run level of aggregate real GDP, implying that the no-retaliation gains to the US auto industry are offset elsewhere with lower output and job losses in other industries. This effect is more pronounced in the first two years after enactment. Real GDP growth is -0.1pp lower in calendar year 2025 and a few basis points lower in calendar year 2026. After 2026, the level of GDP begins to recover modestly as production and supply chains reoptimize. But in the long-run, US output is still -0.04% lower with limited retaliation and -0.05% with full retaliation. That’s the equivalent of the US economy being permanently smaller by $12-$16 billion annually in 2024 dollars. In particular, real exports are lower in the long-run under both scenarios: -1.8% under no retaliation and -2.6% under retaliation. Exports fall even without retaliation because the dollar strengthens, making US goods and services less price competitive overseas.

- Fiscal impact. The automobile tariffs are the equivalent of a rise in the effective tariff rate of 2.9 percentage points. Were they to remain in place, the tariffs would raise $600-650 billion over 2026-35 conventionally-scored.3 Given the negative output effects of the tariffs to date, there would be additional dynamic reductions in tax revenue as a result. Based on Congressional Budget Office rules-of-thumb, TBL estimates that these effects would range between $85 billion under limited retaliation to $115 billion with.

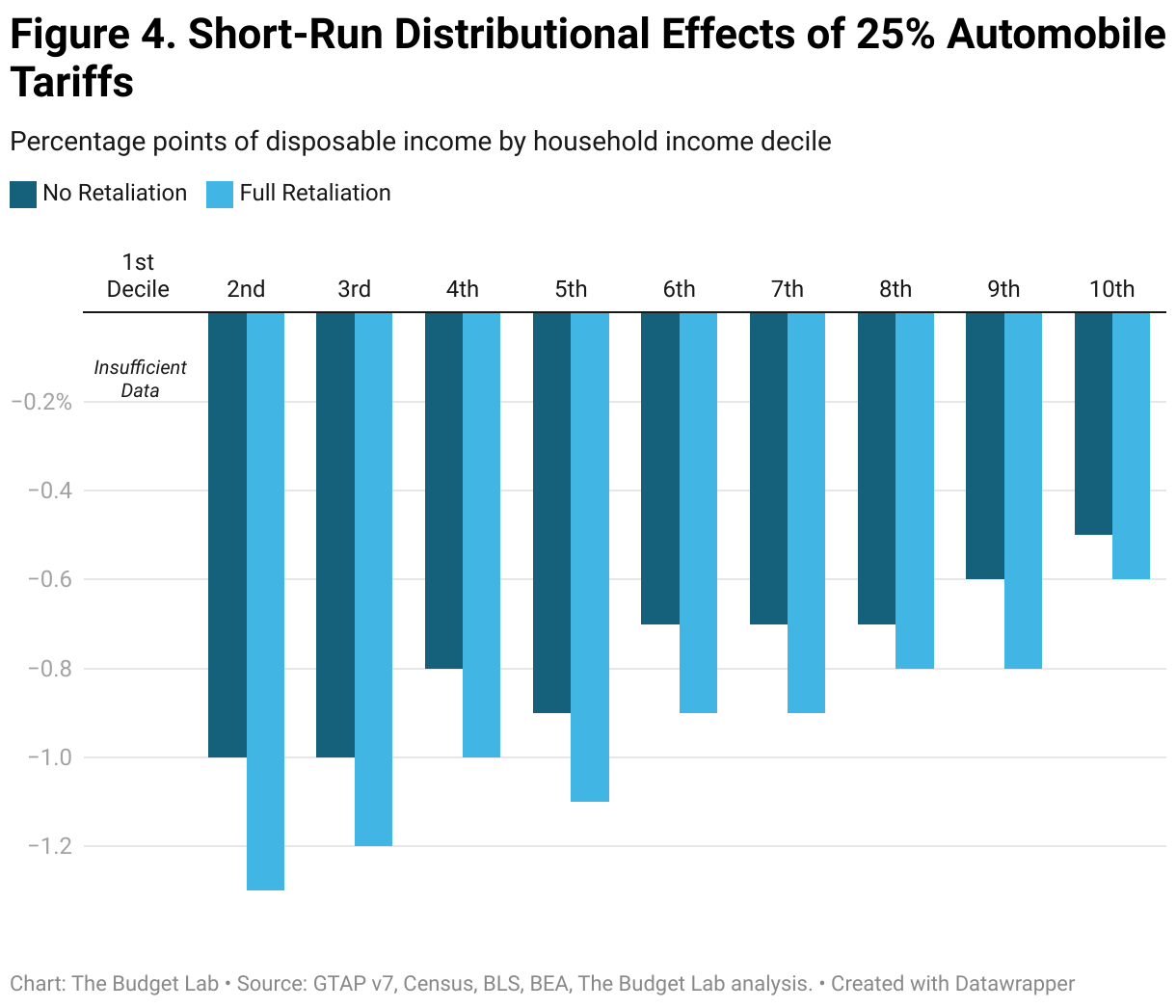

Short-run distributional impact. Tariffs are a regressive tax, especially in the short-run. This means that tariffs burden households at the bottom of the income ladder more than those at the top as a share of income. This holds true even with a narrow automobile tariff as well: according to the Consumer Expenditure Survey from the Bureau of Labor Statistics, net automobile purchases made up 6% of income for families in the 2nd decile of income but slightly less, 5.3%, for families in the top decile, suggesting families at the bottom are generally more exposed. Indeed, the percent change in disposable income resulting from the automobile tariffs is 2x as much for households in the second decile by income as it is for households in the top decile: -1.3% versus -0.6% in the case of tariffs with full retaliation (see top panel of chart below).

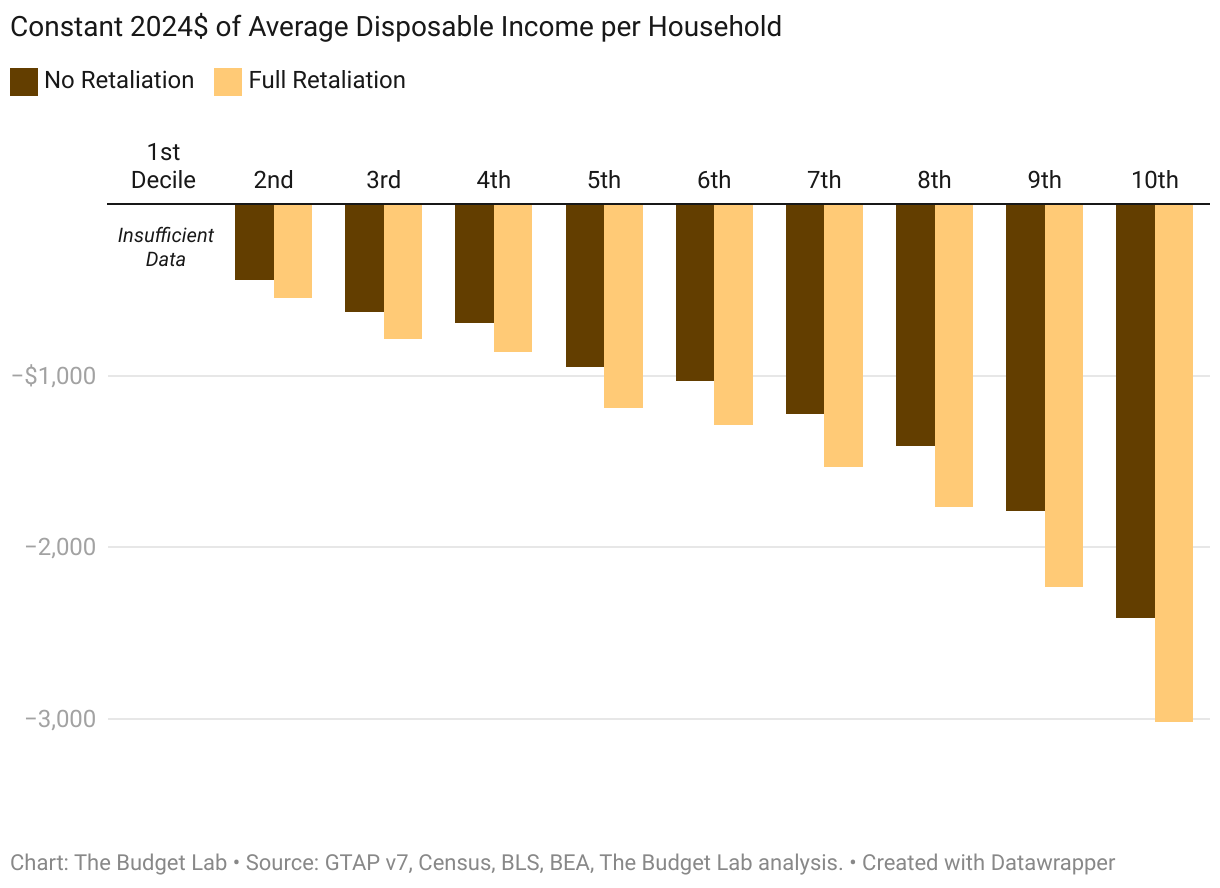

Because income rises across the distribution more steeply than the tariff burden falls, the tariff burden in dollar terms is higher at higher incomes (bottom panel). For a household in the second lowest income decile, the tariff proposal leads to consumer loss of $550 per household on average (across families that both do and do not end up purchasing a motor vehicle) when other countries retaliate. For households in the middle, the burden rises to $1,200 per household on average, and for those in the top tenth, it averages $3,000 per household.

Tariffs are more distributionally-ambiguous in the longer-run. Tariffs reduce both labor income and above-normal returns to capital, or rents. We assume that owners of capital hold rents rather than consume them in the short-run, but consume them over their lifecycle in the long-run. The implication is that the tariff burden is more regressive in the short-run and more evenly-distributed across households in the long-run.

Footnotes

- 10% on Canadian energy & potash, 25% on all other Canadian & Mexican imports other than automobiles and trade that qualifies under USMCA.

- Estimates based on Federal Reserve Industrial Production (IP) data, BEA’s real value-added by industry, and BLS employment requirements matrix.

- TBL employs a “relaxed conventional” assumption for the retaliation scenario, whereby foreign income is permitted to fall but US income remains fixed.