How Would Each CTC Reform Affect Employment and Children’s Economic Outcomes?

Key Takeaways

-

Current Policy, Edelberg-Kearney, and the FSA reforms would increase the return to work. We expect these policies would modestly boost employment among low-income parents.

-

By eliminating the earnings phase-in, the 2021 Law reform option would weaken work incentives, leading to a projected slight decline in employment among low-income parents.

-

Each reform would deliver thousands of dollars annually to most low-income children. Based on the assumption that income accounts for some of the difference in child outcomes between low-income and high-income families, we project that the 2021 Law CTC reform option would boost future earnings by more than 1 percent for children who grow up in the bottom quintile.

In this section, we expand the scope of our scoring to allow for two different kinds of microeconomic feedback: (1) labor force participation changes in response to changes in work incentives, and (2) later-life productivity gains in response to cash assistance in childhood. These changes would not be included in a conventional score, which assumes that overall economic income is unchanged by policy reforms.

Effects on Labor Force Participation

Changes in tax policy can impact work incentives through two channels.1 One is the income effect, wherein people may decide to work less in response to tax cuts because they can maintain the same standard of living despite working fewer hours. Economists generally believe income effects are small for the range of policy reforms considered in this analysis.2

The other is the substitution effect: people may work less or quit working entirely if the return to additional work falls due to an increase in marginal tax rates. In other words, taxes affect the cost-benefit calculation of working versus not working. The precise degree to which workers respond to changes in the return to work – the “participation elasticity” – is a matter of academic contention, but there is consensus that certain subgroups of workers are meaningfully sensitive. Parents and lower-income earners are generally thought to be more responsive than workers who are childless and/or earn higher incomes. Recent academic disagreements over the extent to which the 2021 CTC would affect employment if made permanent were mostly a debate about appropriate participation elasticities.

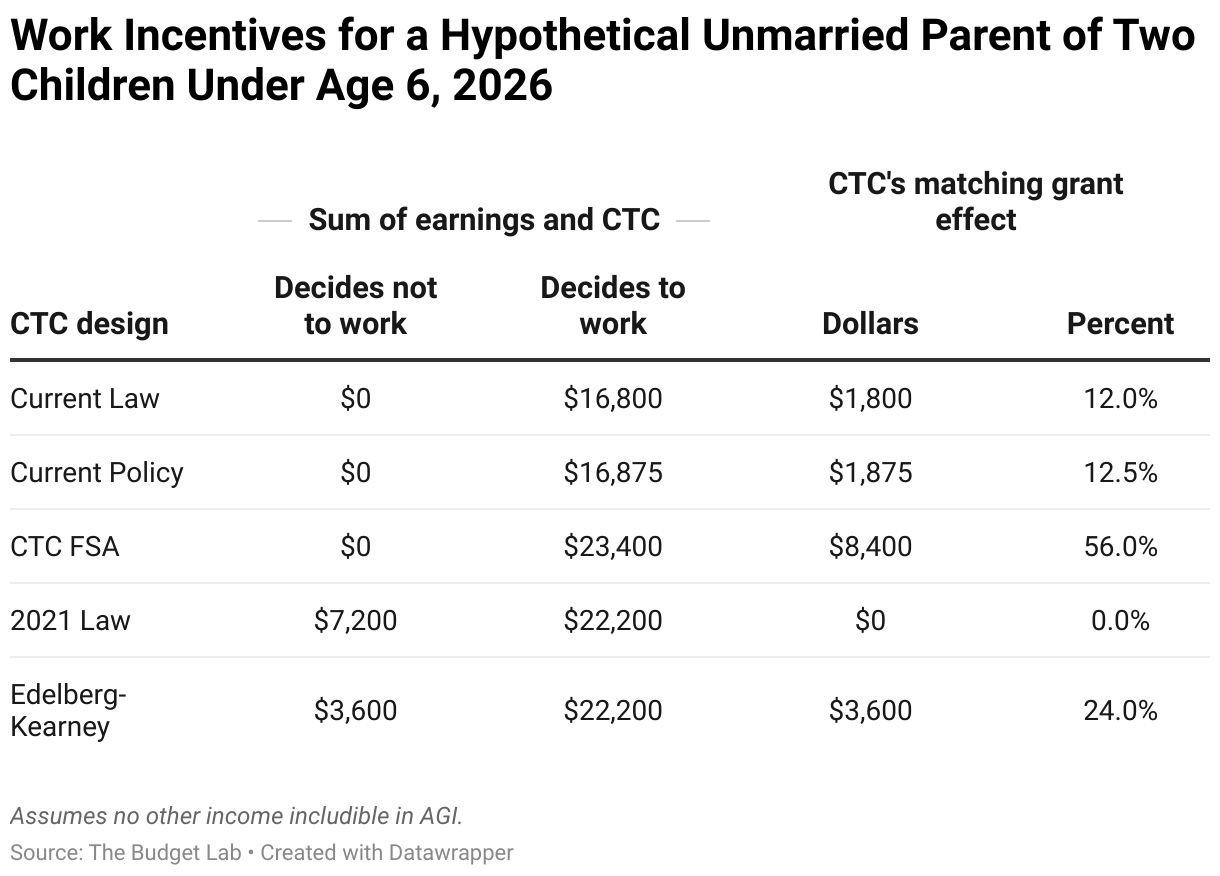

The reforms analyzed in this report vary in their impact on the return to work – and therefore, their projected impact on the decision to work. Consider an unmarried parent of two young children who is deciding whether to work a part-time job at $15 per hour. If they work 20 hours per week, they will earn about $15,000 annually before taxes. How would each reform option affect the decision whether to take this job?

The answer lies in phase-in rates, which create a “matching grant” effect: for every additional dollar of earnings over some range, the government will kick in an extra X cents, where X is the phase-in rate. For example, if the phase-in rate is 30 percent, take-home pay rises by $130 for every additional $100 earned at work. This matching grant effect increases the return to work in the same way that payroll taxes reduce the return to work. Programs that phase in with earnings are often called “wage subsidies” for this reason.

The following table reports the matching grant effect for our hypothetical parent of two under each CTC reform option.

- The FSA CTC provision would provide no benefits at $0 of earnings but make available the full credit value by $10,000 of earnings. This change creates a substantial matching grant effect, especially for parents of multiple children. In the case of the hypothetical parent of two, the FSA CTC would offer a sign-on bonus of $8,400.

- The FSA CTC expansion is proposed in the context of cuts to other programs that also strengthen the return to work for low-income parents. The hypothetical parent of two would see their EITC benefit fall from about $6,000 to just $2,000, meaning the matching grant effect under the full FSA would be smaller than suggested by considering the CTC provision alone.3

- Current Law and Current Policy have similar phase-in rules, and thus take-home pay would be similar under both scenarios for this parent. The fact that Current Policy offers a larger maximum credit value does not factor into this parent’s labor force participation decision at this income level.

- 2021 Law, on the other hand, does not phase in with earnings and therefore creates no matching grant effect. This means that, considered in isolation, the CTC would be neutral with respect to work: the parent would receive the full credit value independent of the decision to work. But by removing the existing work subsidy, moving from current law to 2021 Law would disincentivize work. In other words, effective marginal tax rates would rise under 2021 Law.

- Because the phase-in rate would rise to 30 percent – and despite the proposal offering some amount of income even if the parent chooses not to work – the matching grant effect under Edelberg-Kearney would be larger than under current law. This design structure reflects the proposal’s goal of alleviating deep poverty without disincentivizing work.

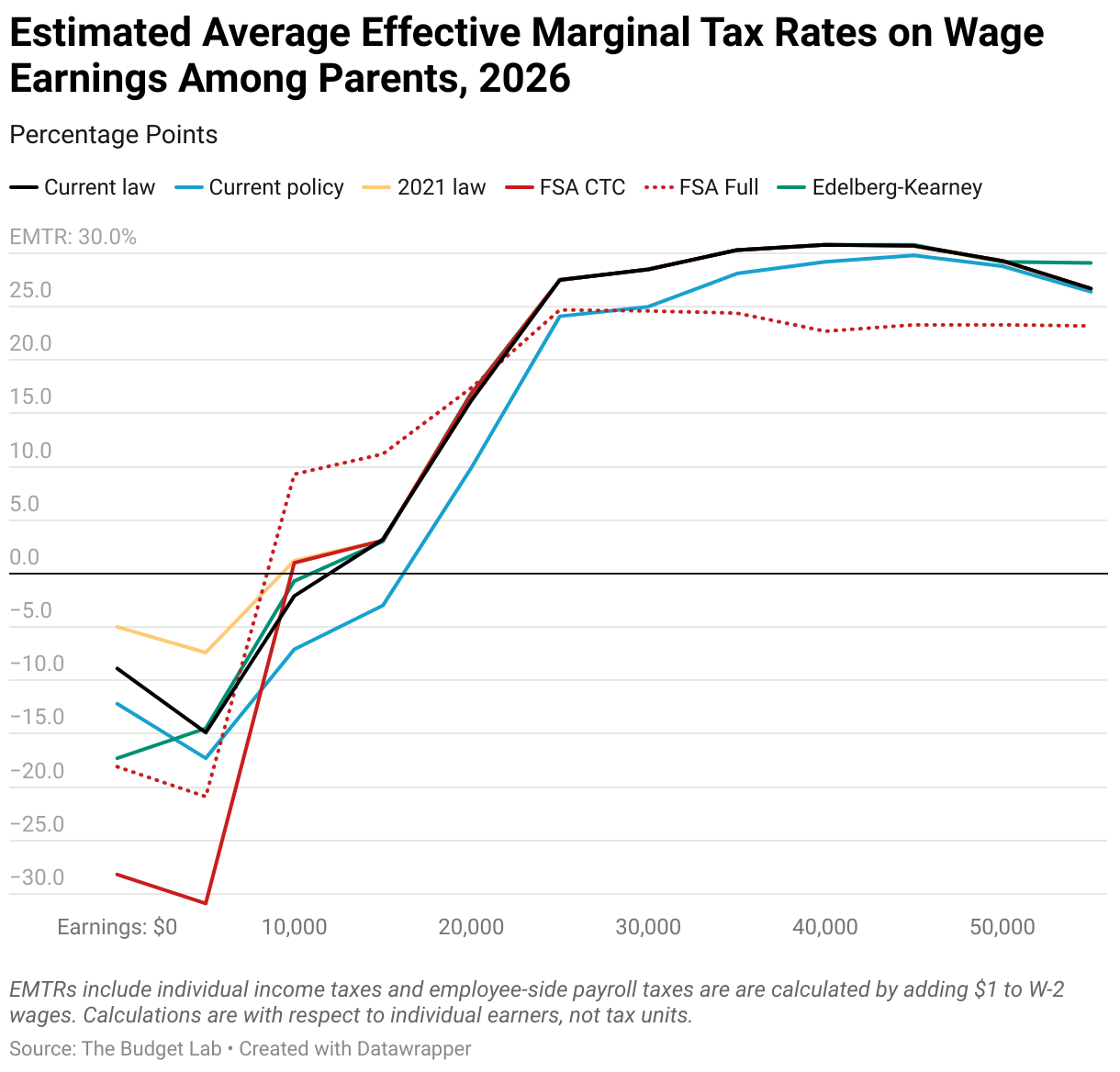

Differences in matching grant effects show up in effective marginal tax rates (EMTRs) on wages – that is, the additional tax paid on an additional dollar of earnings. The figure below plots average EMTRs, including payroll taxes, for parents by amount of earnings.

- Low-income parents generally face negative EMTRs under current law due to phase-ins for the CTC and EITC. As earnings rise and those credits plateau and/or begin to phase-out, average EMTRs quickly rise to levels associated with higher-income earnings.

- The FSA’s CTC provision and its phase-in structure deeply cuts average EMTRs for parents making below $10,000 – after which point the credit no longer subsidizes wages at the margin. However, the FSA’s EITC reforms increase EMTRs for most parents. The net effect is to increase work incentives at the very lowest end of the distribution but reduce them for those earning $10,000-$20,000.

- One interpretation of these findings is that the FSA strengthens the incentive to participate in the labor force, but among those already working part–time, it reduces the incentive to increase hours worked or move to a higher-paying job.

- Despite maintaining the current-law phase-in rate of 15 percent, Current Policy would slightly reduce average EMTRs among parents. By doubling the maximum value to $2000, fewer parents would have reached the end of the phase-in range among the earnings groups shown in the chart.

- By eliminating the phase-in entirely, 2021 Law would increase average EMTRs for low-income parents.

- The Edelberg-Kearney reform option would reduce average EMTRs on the first $5,000 of earnings by about 8 percentage points. This change is caused by its doubling of the phase-in rate.

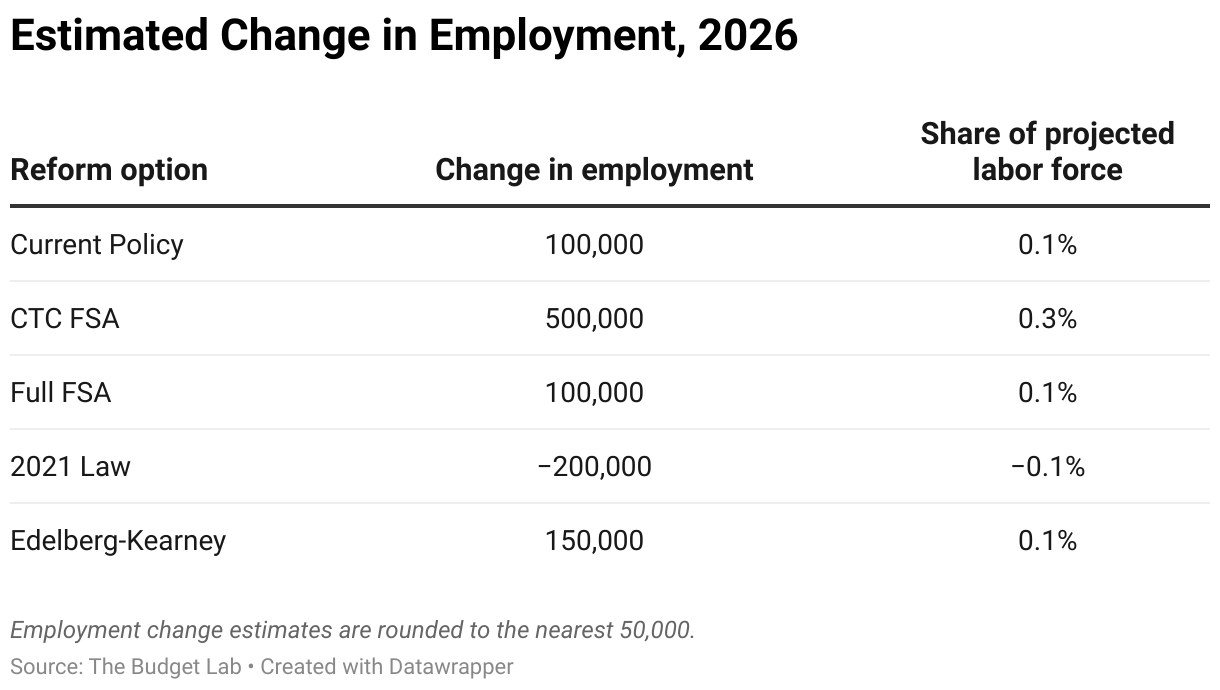

Next, we estimate how these changes in incentives would generate employment gains or losses. This analysis depends critically on assumed labor supply elasticities. Though recent work found no statistically significant impacts of temporary changes to the CTC on labor market incomes, a broader literature on participation elasticities suggests the response would not be zero in the case of permanent reforms. We adapt and extend an approach similar to that of Bastian (2023) in our tax microsimulation model; please refer to this page for a complete description of our methodology to estimate employment changes.

The following table presents our estimates of the change in overall employment, rounded to the nearest 50,000 workers. We find that the FSA reforms, Current Policy, and Edelberg-Kearney reforms would have similarly modest, positive impacts on employment, while 2021 Law would slightly reduce overall employment.4 The CTC provision of the FSA generates the largest employment gains, though its stronger work incentives are mostly outweighed by the proposal’s EITC cuts. To put these numbers in context, the average monthly increase in the labor force from December 2011 to December 2019 was around 110,000 people.

Effects on Child Outcomes

To what extent does cash assistance for families with children – particularly low-income families with children – improve economic outcomes for those children when they grow up? The answer has important budgetary implications. If policy interventions today can increase the productivity and wages of the next generation, some fraction of the up-front costs will be offset by higher income and payroll tax revenues in the future.

Additional income in childhood might impact later-life outcomes through various channels including improved nutrition and health, better education, the ability to move to higher-opportunity geographic areas, and more. Recent policy research has attempted to quantify the benefits of a 2021 Law-style CTC expansion by using empirical evidence on the relationship between cash or near-cash assistance to lower-income families.

To account for these potential effects in our budget scores, we take a somewhat different approach. The basis for our simulations is descriptive evidence on intergenerational mobility – the observed relationship between parent’s income and child’s eventual income. Specifically, we measure the impact of a reform in terms of parent income rank, then adjust future labor market outcomes of affected children to partially reflect those of children in the counterfactual parent rank. A complete technical description of our methodology can be found here.

To summarize our approach, consider children in the 2026 birth cohort who, under a sample CTC expansion proposal, will receive an extra $5,000 per year until they turn eighteen. We estimate the effect of the CTC on 2050 earnings for the 2026 birth cohort as follows for each simulated earner in 2050 under current law:

- We use the 100-by-100 rank-rank mobility matrix from Chetty et. al (2014) to impute a parent income percentile. For example, for bottom quintile child earners, the median imputed parent income percentile is the 35th percentile, with half of imputed parent income percentiles lying below the 35th percentile and half lying above.

- We use the parental income distribution to convert the $5,000 payment to parent income percentiles Δp. For example, at the 15th parent income percentile during the 2026-2042 years receiving the CTC, Δp = 5: the child’s parents would have earned at the 20th income percentile if their parents would have earned $5,000 more while all other parents’ incomes were held fixed.

- We increase the child’s earnings by 0.34 * 0.2 * Δp child earnings ranks, as measured in the status quo child earnings distribution. The parameter 0.34 equals the cross-sectional relationship between child income rank and parent income rank. The parameter 0.2 equals our chosen estimate of the causal share of the child-parent rank-rank cross-sectional relationship. For example, for a child at the 20th percentile in the 2050 current law wage earnings distribution with an imputed parent at the 15th percentile, we increase the child earnings by $100, which is equal to the dollars in the 2050 current policy income distribution represented by 0.2 * 0.34 * 5 child ranks.

The 20 percent assumption is informed by our conversations with researchers who work on intergenerational mobility and poverty issues, and our assessment of the academic literature, in which some papers find no impact of cash or cash-like resources during childhood on later life outcomes, while other papers find large impacts. This assumption implies that incremental cash during childhood has substantial impacts on children’s later-life outcomes, but that 80 percent of the correlation between parent and child income is not attributable to income alone.

Compared with our other estimates, the results in this subsection are considerably more uncertain. This exercise involves strong assumptions and depends on multiple data imputation steps. Still, we believe it functions as a useful starting point for a discussion about plausible magnitudes.

Our estimation procedure involves several strong assumptions, including those that can lead to overestimating the positive revenue feedback of the CTC. First, we do not estimate capital crowd-out and resulting impacts on wages due to a deficit-financed CTC. Second, our 20 percent causal estimate is a general equilibrium parameter that includes wage adjustments due to skill increases, but we do not vary the 20 percent causal estimate across years as new birth cohorts age into the policy and enter the workforce. Third, the 20 percent assumed causal share is highly uncertain and implies a larger (29 percent) causal share of after-tax income, under the approximation that most U.S. households face an approximately 30% (i.e., 0.29 = 0.2 / (1 - 0.3)) all-in effective marginal income tax rate as suggested by Piketty, Saez, and Zucman (2016). We intend to revisit and refine our assumptions over time and emphasize that these estimates are a work in progress.

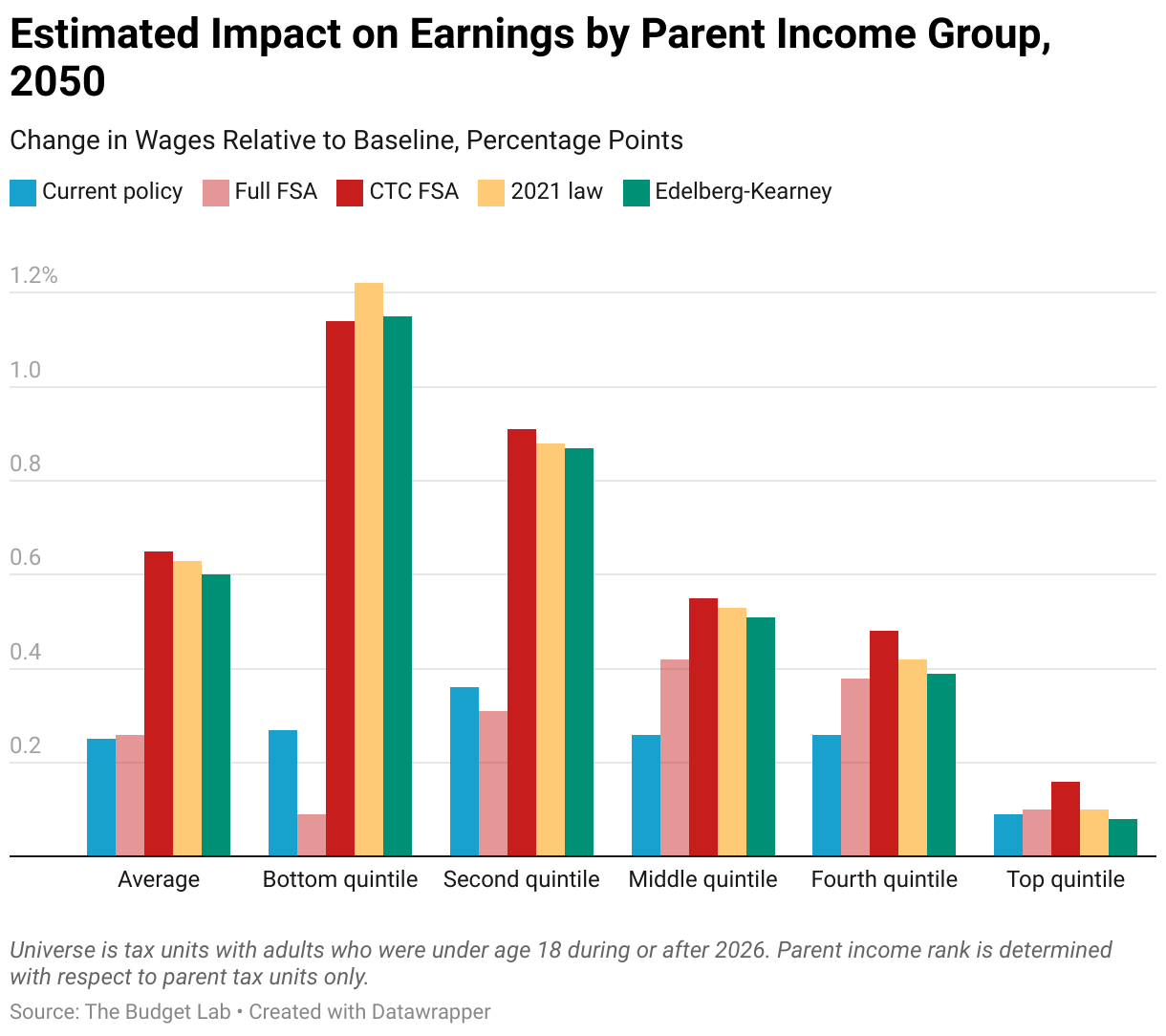

The following figure displays estimated changes in wages in 2050 among children exposed to a full 18 years of each reform. It breaks out effects by parent income rank.

- Considered alone, the FSA’s CTC provision would provide later-life benefits comparable to those of 2021 Law and Edelberg-Kearney. But the package as a whole, which offsets CTC expansion with other tax increases, especially for unmarried parents with multiple children, is expected to provide limited benefits, on average, for children who grow up in this group.5

- We project that kids who grow up in a bottom-quintile family would fare best under the 2021 Law and Edelberg-Kearney reform options, with wages for these children being one percent higher compared to current law (about $300 in additional earnings every year, adjusted to current price levels). Current Policy, which excludes low-income families from receiving full benefits, would generate much smaller effects for children in this group.

- Each CTC expansion would provide smaller benefits as a share of income to higher income families. Children whose parents rank in the top quintile are expected to see the smallest relative benefit in adulthood, fundamentally driven by the CTC representing a smaller share of income at higher income levels.

Footnotes

- The elasticity values we use generate a probability of employment with respect to taxes. What we model is the existence or non-existence of wages. Therefore, what we see is earnings on the extensive margin, which is functionally a participation decision. We have tried to be consistent in our use of “employment” or “participation” accordingly.

- Please see this CBO report for a discussion of the relevant evidence.

- A Center on Budget and Policy Priorities analysis finds that some low-income parents – namely, those with multiple children above age five – would be made worse off when accounting for the loss of EITC benefits.

- Our results for 2021 Law are not directly comparable to those of other researchers, who estimate employment changes against a different policy baseline.

- Note that parent income ranks are assigned to children based on the distribution of income among tax units with children only. This population universe contrasts with that of our standard income distribution metrics, in which all tax units, including those without children, are considered. For this reason, impact as measured by the latter definition does not necessarily map to impact by parent rank.