State of U.S. Tariffs: SCOTUS Ruling Update

Key Takeaways

-

The Budget Lab (TBL) estimates the effects of all US tariffs and foreign retaliation implemented in 2025 after the decision by the Supreme Court of the United States (SCOTUS) that President Trump exceeded his authority to invoke the 1977 International Emergency Economic Powers Act (IEEPA) to impose reciprocal tariffs.

-

Current Tariff Rate: Without IEEPA tariffs, consumers will face an overall average effective tariff rate of 9.1%, which remains the highest since 1946 excluding 2025. (If IEEPA tariffs had been allowed to stay in effect, this figure would have been 16.9%.)

-

Overall Price Level & Distributional Effects: Under TBL’s assumptions about macroeconomic effects and Federal Reserve responses, the price level will rise by 0.6% in the short run, representing a loss of about $800 for the average household and $400 for households at the bottom of the income distribution. (With IEEPA, the price level impact would instead be 1.2%.)

-

Commodity Prices: After the SCOTUS case, the remaining set of tariff policies in effect at the start of February 2026 fall most heavily on metals, vehicles, and electronics. (If IEEPA tariffs had not been invalidated, the burden would have also fallen more heavily on apparel and food products.)

-

Real GDP Effects: TBL estimates that the temporary positive fiscal impulse from IEEPA refunds will approximately offset the negative growth impacts of the remaining tariffs for 2026. In the longer run, the US economy will be persistently 0.1% smaller, the equivalent of about $30 billion annually in 2025$. (If IEEPA tariffs had not been invalidated, the long-run hit to output would have been 0.3%)

-

Labor Market Effects: The unemployment rate is estimated to be about 0.3 percentage points higher by the end of 2026 due to remaining tariffs. (If IEEPA tariffs had not been invalidated, the 2026 hit to employment would be about twice as large.)

-

Long-Run Sectoral GDP & Employment Effects: In the long run, tariffs present a trade-off. US manufacturing output expands by 1.2% but these gains are more than crowded out by other sectors: construction output contracts by 2.4% and agriculture declines by more than 1%. (These relative patterns are similar with or without IEEPA tariffs.)

-

Fiscal Effects: All tariffs to date as of February 2026 are projected to raise about $1.2 trillion over 2026-35, though slower economic growth reduces revenues and brings the net dynamic revenue to $1 trillion. (With IEEPA, these figures would be more than twice as large.)

-

Discussion: The economic implications of the SCOTUS decision are complicated by two major factors. First, in the short-term, firms will be aggressively seeking refunds on tariffs paid in 2025, which has large revenue effects and uncertain distributional effects. Second, the current Administration has stated its intent to replace IEEPA tariffs with tariffs using other authorities, but there remain timing and other questions regarding these steps.

SCOTUS Decision

On February 20th, 2026, SCOTUS decided that the President’s use of IEEPA to impose reciprocal tariffs on other countries exceeded his authority under that law and held that the IEEPA tariffs must be vacated. These tariffs made up most of the tariff regime that has been put in place over the course of 2025. The most recent estimates from the U.S. Customs and Border Protection imply that $142 billion will have been collected from tariffs enacted under IEEPA authority over the course of 2025.1 SCOTUS did not rule out allowing importers to claim refunds on refunds on any IEEPA tariffs they may have paid. While there are a range of questions regarding the process firms will go through to obtain refunds, it is likely that a substantial portion of the revenue raised via IEEPA in 2025 will be returned to firms.

Changes Since the Last Report

TBL has not made any substantial changes to the model since our January 19th report.

Results

This report focuses on two scenarios for tariff policy:

Current Policy. In this scenario, we follow the SCOTUS decision and model the repeal of IEEPA tariffs and the refunding of IEEPA tariffs to imports. Tariffs under other legal authorities are unaffected. Importantly, we assume that the administration does not replace IEEPA tariffs with new tariffs under other authorities.

IEEPA Upheld. In this scenario, tariff policies as of February 20th remain in effect in perpetuity.

Table 1 presents the impacts of the set of Tariffs (those in place as of February 20th, 2026) with and without the IEEPA tariffs that SCOTUS ruled on today. It also reports a third column showing how the question of refunds affects our estimates.2 The results are presented as changes relative to a counter-factual where no tariffs were implemented after January of 2025.

Average effective tariff rate

Table 1 presents two different measures of the effective tariff rate: pre-substitution (before consumers and businesses shift purchases in response to the tariffs) and post-substitution (after they shift).

Measured pre-substitution—assuming there are no shifts in the import shares of different countries and products—post-SCOTUS tariff policy represents the equivalent of a 6.7 percentage point increase in the US average effective tariff rate. That calculation assumes that, for example, the share of imports from China remains at 13%, where it was in 2024. A pre-substitution approach is a good measure of welfare, since it reflects the full cost faced by consumers before they start making difficult spending choices. This increase would bring the overall US average effective tariff rate to 9.1 percent, which is about one third of the peak rate experienced in 2025.

Post-substitution—after imports shift in response to the tariffs—the current suite of tariffs generates a 5.6 percentage point increase in the US average effective tariff rate, which brings the overall US effective tariff rate to about 8.0%. The timing of the transition from “pre” to “post” substitution is highly uncertain. Some shifts are likely to happen quickly—within days or weeks—while others may take longer.3

Had the President’s authority to enact tariffs via IEEPA been upheld, the pre-substitution effective tax rate would have been 16.9%, and the post-substitution rate would have been 14.3 percent.

Table 2 breaks down the changes in effective tariff rates through February 2026 by country and region. Panel A shows the changes without IEEPA, and Panel B shows the changes had SCOTUS held that IEEPA authorized the current set of tariff policies. IEEPA invalidation cut the effective rate on Chinese imports by almost two thirds while reducing the rate for Canada and Mexico by much less.

Average aggregate price impact

The tariffs through 2026 imply an increase in consumer prices of 0.6% in the short run, assuming full passthrough of tariffs to consumers. (For the purpose of this calculation, TBL assumes the real income adjustment imposed by tariffs comes through prices rather than nominal incomes.) This is a pre-substitution number that captures consumer welfare effects. It is the equivalent of a short-run income loss4 of about $800 per household on average in 2025 dollars. The post-substitution price increase settles at 0.5%, a $600 loss per household.

Had SCOTUS held that IEEPA tariffs could remain in effect, these price impacts would have been about twice as large.

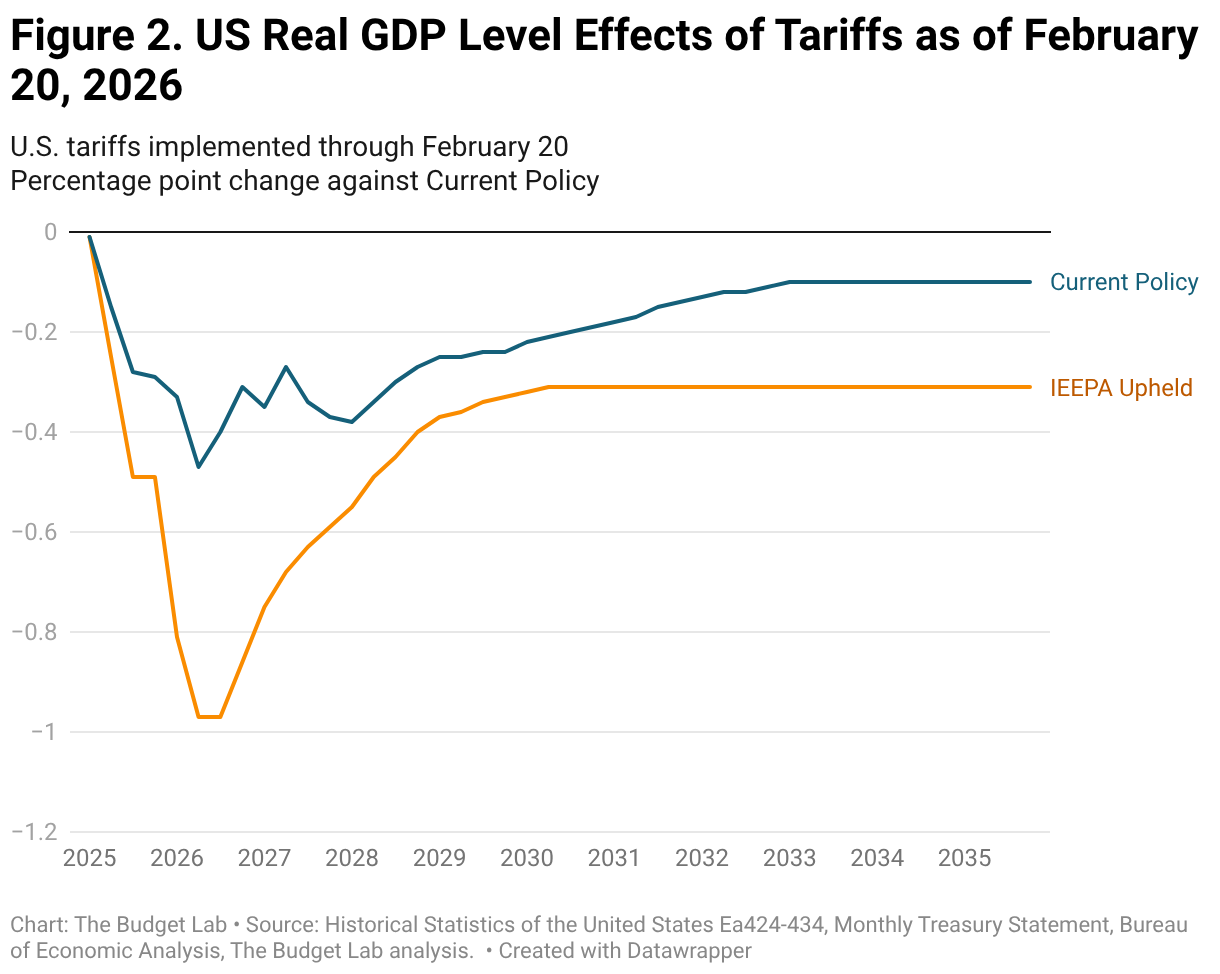

US real GDP & labor market effects

TBL projects that, all else equal, the remaining tariffs will increase the unemployment rate by 0.3 percentage points and reduce payroll employment by 550,000, by the end of 2026. We estimate that the temporary positive fiscal impulse from IEEPA refunds will approximately offset the negative growth impacts of the remaining tariffs for 2026, though there is substantial uncertainty over how and when refunds will be administered and thus the short-term effects of these refunds is uncertain. The level of real GDP remains persistently 0.1 percent smaller in the long run (the equivalent of about $30 billion in 2025$ annually). With IEEPA tariffs, these economic costs would have been somewhat larger.

Long-run US sectoral output & employment effects

Without IEEPA tariffs, the existing set of trade policies are set to shrink the overall size of the US economy in the long run, but beneath aggregate GDP they also drive reallocation across US sectors. Long-run output in the manufacturing sector expands slightly due to the remaining tariffs. But this expansion of the overall manufacturing sector more than crowds out the rest of the economy: agriculture, construction, and mining sectors all see reductions in output. These relative patterns would have been similar (though larger in magnitude) had the President’s use of IEEPA power been upheld.

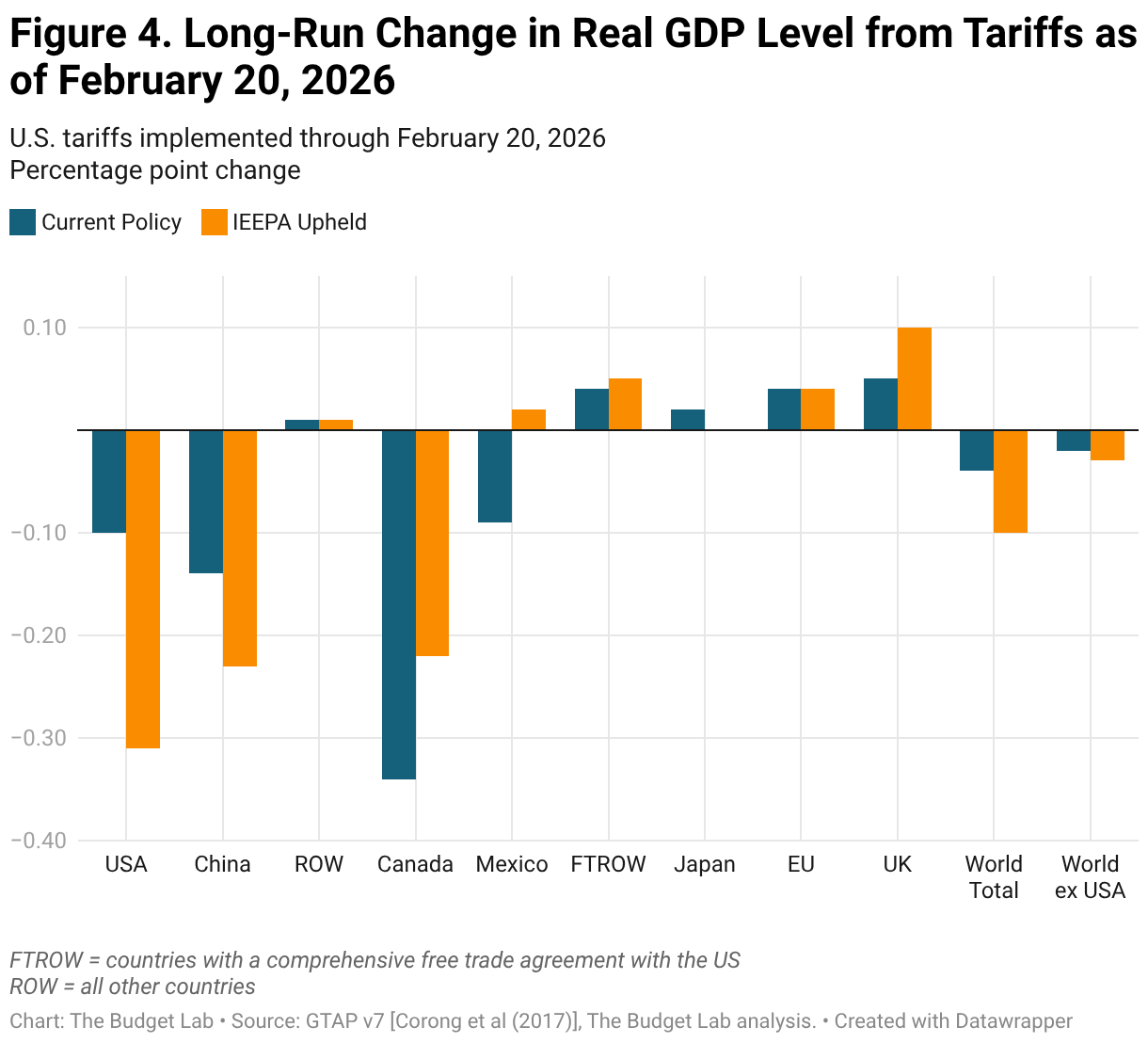

Global long-run real GDP effects

Long-run global GDP is slightly lower due to the tariff policy after the decision regarding IEEPA, but this aggregate figure masks heterogeneity across countries. China’s and Mexico’s economies are each somewhat smaller due to the remaining tariffs, whereas the UK, EU, and Japan all see small gains in the long run. Canada sees the largest decline without IEEPA. With IEEPA, these relative effects would have been somewhat different: Canada would have seen a smaller hit to output, and Mexico’s economy would have been slightly larger, not smaller.

Fiscal impact

The tariffs as of February 20th, 2026, following the SCOTUS decision, would raise more than $1.2 trillion over ten years, conventionally scored.5 Given the negative output effects of the tariffs, these new revenues will be partially offset by reductions in tax revenue because of lower growth. Based on Congressional Budget Office rules-of-thumb, TBL estimates that these effects would total almost $200 billion over the decade. This is about half of what would have been raised if IEEPA tariffs were upheld by court.

Distributional impact

One way to measure the distributional burden of tariffs is to look at the relationship between consumption, which gets more expensive under tariffs, and income for a given year. Under this view, tariffs are a regressive tax because lower-income households spend a larger fraction of their income than higher-income households do on average.

TBL finds that the burden, expressed as a share of post-tax-and-transfer income, after the removal of IEEPA tariffs would be about 3 times larger on the first decile than the top (1.1% versus 0.4%). The average annual costs to households in the first and top decile are about $400 and $1,800 respectively in 2025$. With IEEPA tariffs, these burden numbers would have been about twice as large.

Commodity price effects

The charts below show how the 0.6% price level increase from the tariffs as of February 20th, 2026 would look across individual commodities in the short-run (pre-substitution) and the long-run (post-substitution). We find that metal products, electronics, and vehicles rank among the products with the largest price increases in both the short and long run. If the Court had ruled differently, this picture would have looked somewhat different: price increases for apparel and food products (burdened more heavily by IEEPA tariffs) would have also ranked near the top.

Discussion

Refunds

Since the oral arguments for this case back in September, firms have increasingly positioned themselves to be able to receive a refund for any tariff paid under IEEPA authority. The exact mechanism for repayment is uncertain, but there are substantial economic consequences of that effort. The first of these is straightforward; any refund process would reduce the total amount of revenue raised by the new system of tariffs. The size and timing of that reduction will be partially a function of the complexity and ease of the refund process. The wider economic impact of the refund process depends in part on the behavior of firms, and mirrors in many ways the conversation regarding the pass-through of tariffs to consumers via higher prices. Firms that receive refunds could choose to pass along those savings to consumers by lowering prices, or they could instead either re-invest those funds or transfer them to owners via dividends or stock buybacks. Net economic and distributional consequences of refunds depend in large part on these responses. Consider the case where firms passed 75 percent of the new tariffs along to consumers, but firms do not adjust prices in response to refunds. This would represent a transfer from consumers to firm owners. The net economic impact of this would then depend on how those additional resources were spent.

Replacing IEEPA tariffs using other Tariff Authority

One of the major sources of uncertainty regarding the future economic impacts of tariffs is the degree to which the current Presidential administration will respond to this decision by raising tariff rates via other tariff authorities. As has been discussed in both the press and by economists, the president has other sources of legal authority to enact tariffs without further congressional action. These authorities generally fall into two groups: those that require investigations by federal agencies but have few if any restrictions on the eventual tariffs imposed (Sections 201, 232, and 301) and Section 122, which provides a temporary authority to impose tariffs without an investigation, but is limited to a 15 percent rate for only 150 days. There is another authority, under Section 338 of the Tariff Act of 1930 (otherwise known as Smoot-Hawley) that would allow the President to impose a 50 percent tariff with no investigation or time limitations, but no President has used this authority before, raising again concerns about future legal challenges.

Scholars have shown that it is likely that a tariff regime as large as that created in part with IEEPA authority could be constructed via some combination of these laws. First, in the short run, many of the IEEPA tariffs could be replaced by a 15 percent rate under Section 122. While the exact way this authority would interact with other tariffs is unclear, if the President were to employ this authority to fully replace IEEPA tariffs without any product- or country-specific exemptions and set the rate to its maximum level of 15 percent, we estimate the pre-substitution effective tariff rate would rise to 24.1 percent, higher than TBL’s estimate of 16.9 percent with IEEPA intact. If instead Section 122 were applied at a rate of 15 percent but the current product- and country-specific exemptions under IEEPA were maintained, the effective rate would instead be 20 percent. Over the medium term, other scholars have highlighted that the growth of Section 232 and Section 301 investigations could be built upon to implement a tariff regime approximately as large as that SCOTUS has just dismantled.

Footnotes

- At the time of this writing, IEEPA collections data is available through mid-December of 2025; $142 billion is an extrapolated estimate for all of 2025.

- We assume that refunds would be issued within the next year, meaning that their impacts are limited to revenue estimates and short-run macroeconomic variables like annual GDP growth and unemployment. Other variables of interest in this report, like the average household burden and price level impact, represent impacts over the medium- and long-run horizons such that the question of refunds has no bearing on them. For further discussion on this topic, see the Refunds section below.

- TBL assumes throughout its tariff analysis that the transition to longer-run GTAP equilibria occurs after three years.

- TBL defines “income” as CBO-concept post-tax-and-transfer income. “Short-run” refers to the effect over the next couple of years; TBL proxies for this definition by using CBO projections of the distribution of income in 2027, expressed in 2025 dollars.

- TBL employs a “relaxed conventional” assumption for the retaliation scenario, whereby foreign income is permitted to fall but US income remains fixed.