Tax Cuts and Jobs Act Expiration: Options for the Tax Code

Key Takeaways

-

The expiration of the Tax Cuts and Jobs Act (TCJA) offers an opportunity to discuss broad tax changes.

-

In the short run, extending the TCJA leads to higher real gross domestic product (GDP) levels, while a deficit-reducing tax plan that incentivizes investments leads to lower real GDP levels.

-

In the long run, the deficit-reducing plan leads to higher real GDP, while the TCJA extension leads to a slightly lower level of real GDP than we would have seen if the tax cuts had been allowed to expire.

-

An option that provides more tax breaks for children who were raised in the bottom income quintile would on average raise their wages as adults by nearly 1 percent annually.

-

On net, the extension options would decrease the burden of filing taxes by an estimated 1.3 hours on average relative to current law. Average burdens could be lessened even more by allowing the qualified business income (QBI) deduction to expire entirely.

-

Under each tax plan scenario, almost 40 percent of returns could plausibly be pre-populated by the IRS.

Summary

Most individual income tax provisions of the Tax Cuts and Jobs Act (TCJA) expire at the end of 2025. This report analyzes three options for tax reform surrounding expiration: a scenario in which all elements are extended (“Full Extension”), an option which preserves cuts for all but the highest-earning Americans (“Partial Extension”)1, and a tax plan that includes deficit reduction proposed by professors Kimberly Clausing and Natasha Sarin (“Clausing-Sarin”). These options highlight the tradeoffs that policymakers will face in 2025.

The report begins with conventional budgetary and distributional estimates from our microsimulation model.

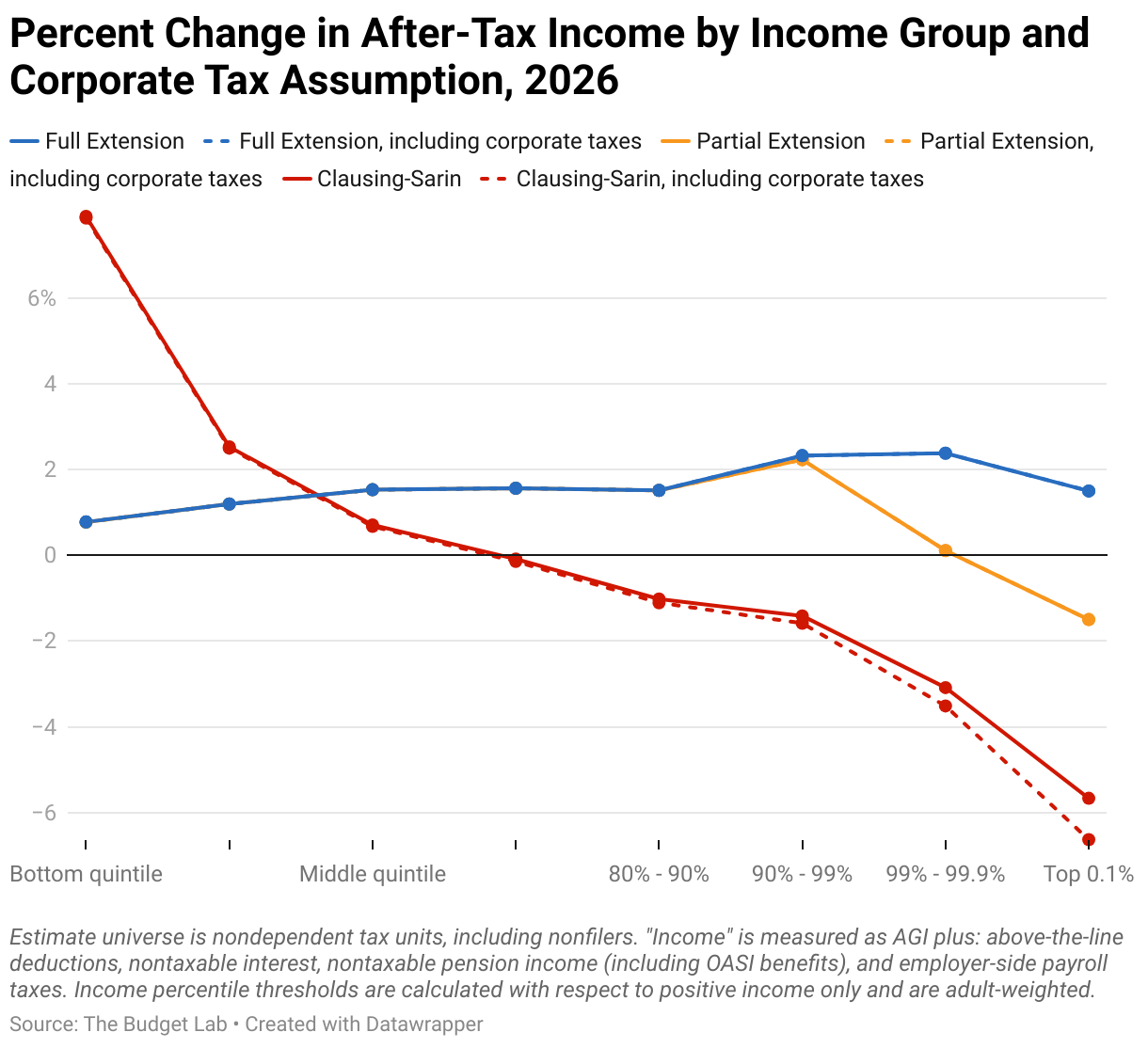

- Full TCJA Extension is estimated to cost nearly $3 trillion over the budget window relative to current law (which assumes full expiration). Benefits accrue to all income and age groups, with higher-income and older taxpayers benefiting somewhat more.

- Moving from Full to Partial Extension, which excludes the highest-earning Americans from tax cuts, would reduce costs from $3 trillion to $2 trillion.

- Finally, the Clausing-Sarin option would reduce deficits by more than $4 trillion in our accounting. Its revenue impacts grow as a share of GDP after the first decade. Lower-income and younger families would benefit on net at the expense of higher-income and older families.

- If policymakers removed rate cuts and the QBI deduction from Full Extension, they would raise revenue while cutting taxes (relative to current law) for the bottom half of the income distribution.

Next, we conduct a microeconomic analysis of each reform. The Full and Partial Extension scenarios are expected to slightly increase employment, while Clausing-Sarin would induce modest labor force exits, with the difference attributable to how each reform affects the returns to labor among lower-income parents.

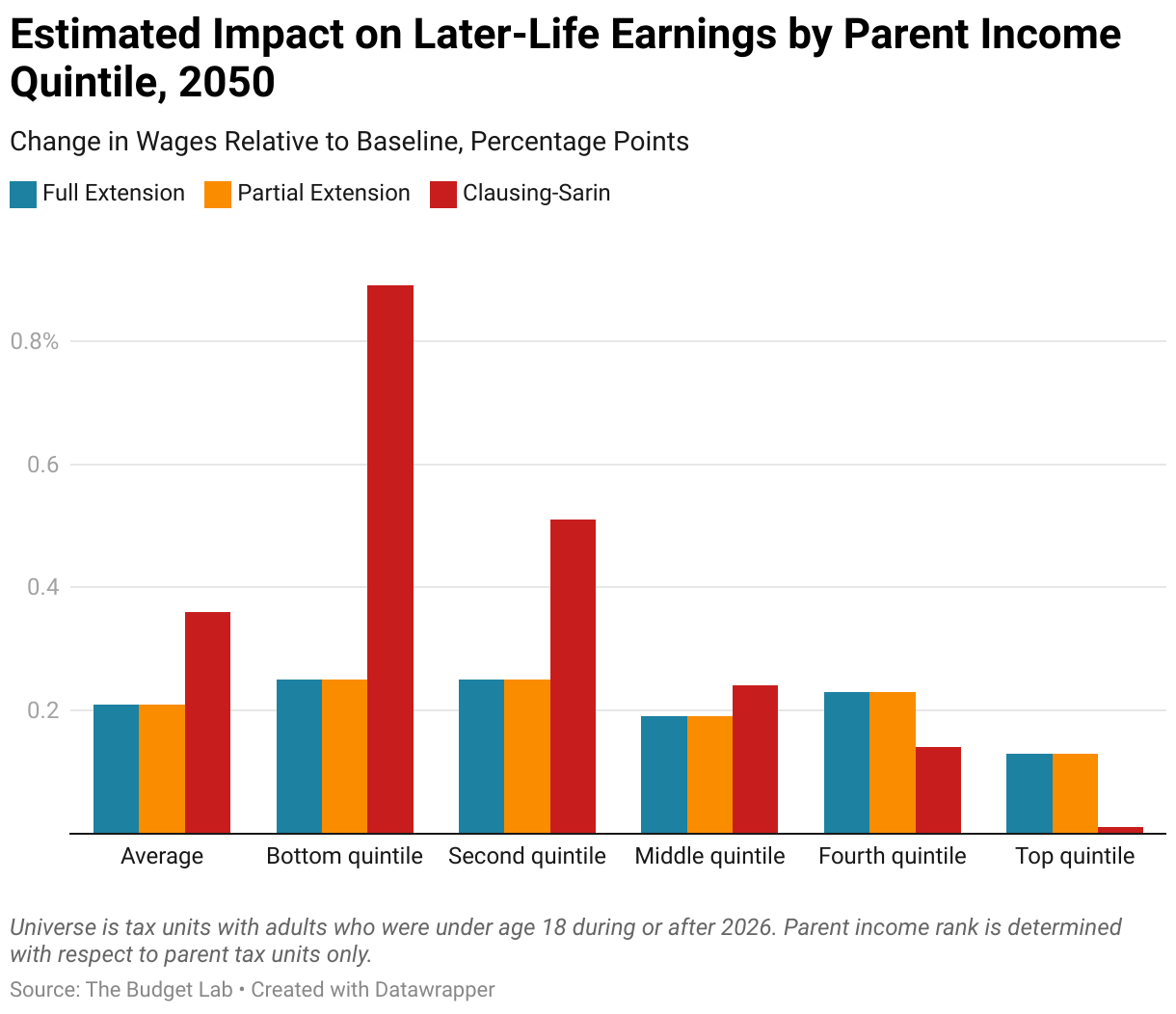

We also model the extent to which child-oriented provisions in each plan translate to improved labor market outcomes in adulthood. These estimates are constructed using a novel methodology exploiting descriptive evidence on intergenerational mobility. Clausing-Sarin, with its Child Tax Credit (CTC) provisions providing more generous benefits to lower-income families, is projected to increase average future wages of children who were raised in the bottom income quintile by nearly 1 percent annually. The Full and Partial Extension options would generate smaller improvements in later-life outcomes.

We then conduct a macroeconomic analysis of each reform using the Federal Reserve’s FRB/US model of the U.S. economy using a fiscal baseline aligned with Congressional Budget Office (CBO) projections. In the short run, we project that the Partial and Full Extension scenarios would temporarily boost real output growth by increasing deficits and thus aggregate demand. In contrast, the Clausing-Sarin scenario would reduce deficits and slow near-term real GDP growth. In the long run, the two Extension scenarios would leave the economy on a slightly slower growth path while Clausing-Sarin would leave it on a faster real growth path through increases in business investment. We expect the Federal Reserve would respond to first-order changes in price pressures by adjusting interest rates, which would be somewhat higher under both the Full and Partial Extension scenarios and lower under Clausing-Sarin.

The report concludes by estimating how each reform would affect tax compliance costs. Some elements of the TCJA (such as the QBI deduction) increased the time burden associated with filing taxes, whereas others (like the reduction in itemizing and alternative minimum tax filers) reduced it. On net, the Full and Partial Extension options would decrease the burden of filing taxes by an estimated 1.3 hours on average. The Clausing-Sarin scenario further lowers average burdens by allowing the QBI deduction to expire entirely. Finally, we estimate that the number of returns for which information could plausibly be pre-populated by the IRS would rise from roughly 36 percent to almost 39 percent under each scenario.

All macroeconomic forecasts and estimated effect sizes are subject to uncertainty, particularly in the long term and for future generations. Furthermore, since the magnitude of policy effects is in part conditional on macroeconomic conditions, the uncertainties around each effect interact with one another. Budget scoring requires educated assumptions and guesses. In addition, estimates involving future earnings outcomes rely on past research informed by models of the historical labor market. However, the labor market may look considerably different in the decades to come. We do not provide confidence intervals throughout this report, but we do attempt to communicate where we are more or less certain in our work.

Background

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, represented a significant overhaul of the federal income tax code. In addition to making permanent and fundamental corporate tax changes, the legislation cut taxes for most families through a series of temporary changes to the individual income tax code. These individual tax changes were written to sunset at the end of 2025, building an inflection point into the government’s budget baseline – a point at which, if no additional legislation is passed, taxes are scheduled to rise from current levels.

As 2026 approaches, policymakers face important questions about how to address the expiring changes. The current macroeconomic environment – one of low unemployment, inflationary pressures, and high interest rates – differs from that of 2017 when the TCJA was passed into law. Renewed interest in debt sustainability and debates over poverty and inequality will shape the contours of any extension legislation put forth. In this context, policymakers will be forced to trade off TCJA extensions that lower tax rates with other priorities, such as long-term deficit reduction, new spending initiatives, lower interest rates, and more.

This report informs the discussion about TCJA extension by exploring three illustrative reform options, designed to highlight certain tradeoffs policymakers will soon face:

- Full Extension is a straightforward extension of each major individual income tax provision otherwise set to expire.

- Partial Extension is an option under which only a subset of expiring provisions is extended, with the goal of targeting tax cuts to be consistent with President Biden’s past pledges.

- Clausing-Sarin, based on a collection of proposals put forth by Kimberly Clausing and Natasha Sarin in a Brookings white paper, uses the 2025 TCJA expiration as the jumping off point for a tax reform plan that aims to reduce the deficit, increase the progressivity of the tax code, limit existing avenues for tax avoidance, and address global issues like climate change.

This report proceeds by viewing each option through four analytical lenses.

- Budgetary: By how much would each reform affect the government’s fiscal picture over the next three decades?

- Distributional: How much do the benefits and costs of each reform vary with income and age?

- Economic: To what extent does each reform induce adults to enter or exit the workforce? Can we expect these reforms to affect future economic outcomes for today’s children? How do broader indicators like GDP, inflation, and interest rates change under each option, and to what extent do these outcomes depend on the Federal Reserve’s actions?

- Administrative burden: How much does each reform add to or subtract from the administrative burden associated with filing tax returns?

Reform options

In this section, we describe each reform option in detail. All reform options are assumed to go into effect beginning in tax year 2026.

The table below summarizes major provisions across each proposed reform.

Full Extension

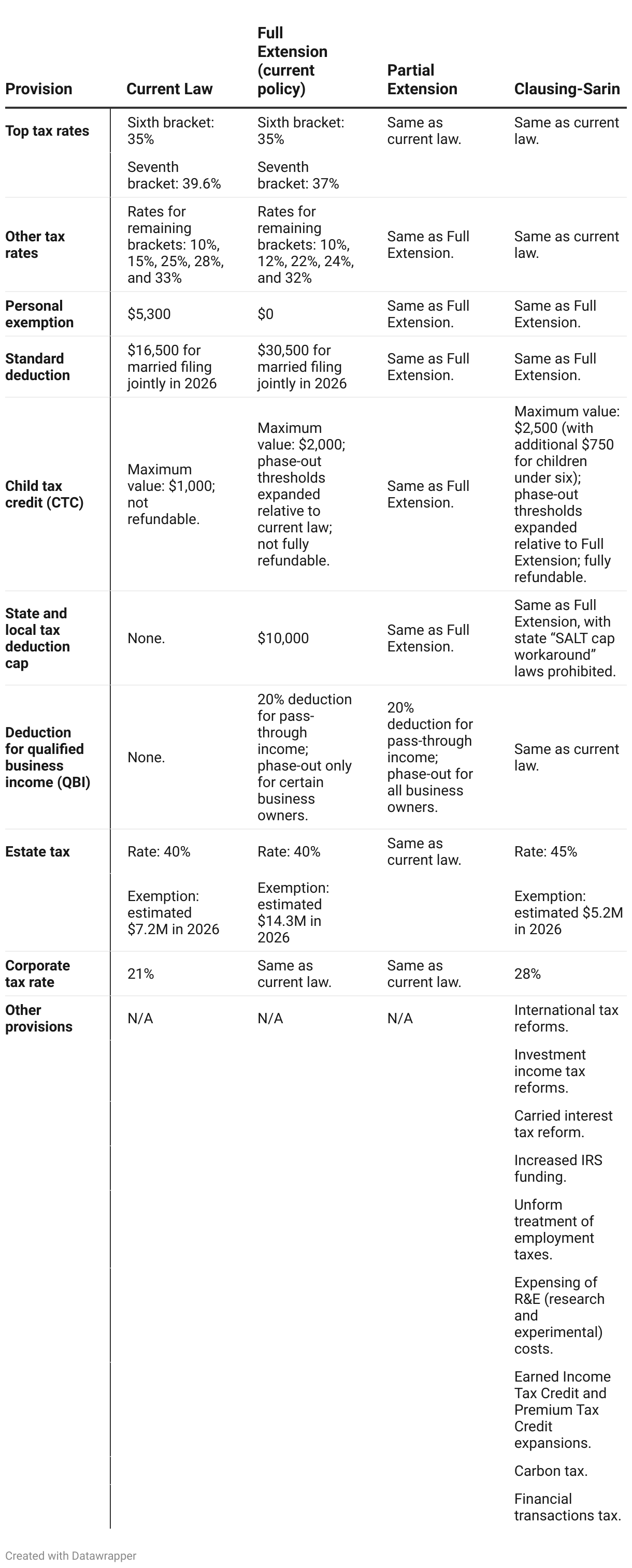

The first reform option is Full Extension, the goal of which is to prevent any significant change in tax law from 2025 to 2026. Specifically, the following TCJA provisions would be made permanent:2

- Reduced tax rates. The TCJA reduced tax rates on ordinary income and re-arranged certain bracket thresholds. The proposal would extend the current system of lower rates rather than allow rates to rise, as is scheduled under current law.

- Expanded Child Tax Credit (CTC). The TCJA increased the maximum value of the CTC from $1,000 to $2,000, expanded eligibility by raising the phaseout thresholds, modified refundability rules, and added a $500 nonrefundable credit for older and non-qualifying dependents. This more generous version of the CTC would be extended under the proposal.

- Expanded Alternative Minimum Tax (AMT) exemption. The TCJA curtailed the number of taxpayers who face the AMT, a parallel tax system that limits the value of tax preferences, by increasing the AMT exemption and raising the income threshold above which the exemption phases out. The proposal would extend these changes.

- Increased standard deduction. The TCJA roughly doubled the standard deduction, reducing effective tax rates and limiting the number of filers who elect to itemize their deductions. This scenario keeps the standard deduction value at its current-policy level, projected to be $30,500 after inflation adjustments for married filers in 2026, rather than allow the scheduled decline (with a projected value of $16,500 for married filers in 2026).

- Limitations on itemized deductions. Under the TCJA, the deduction for state and local taxes (“SALT”) is capped at $10,000, the mortgage interest deduction is limited to smaller amounts of debt, tighter charitable contributions restrictions apply, and several other, smaller deductions where eliminated. It also removed the so-called “Pease” limitation, a high-income surtax related to itemized deductions. The Full Extension option would extend these changes rather than removing them, as is scheduled in 2026.

- Elimination of personal exemptions. The TCJA eliminated personal and dependent exemptions, providing a per-person deduction of $5,300 after inflation adjustments in 2026. Under the reform it would remain at $0.

- Deduction for qualified business income (QBI). The TCJA introduced a new 20 percent deduction for pass-through income. For those whose business consists of service industry activities or does not meet certain criteria related to wage- and capital-intensity, the deduction phases out above a taxable income threshold. This provision, which expires entirely in 2026 under current law, would be extended permanently.

- Limitation on deduction for pass-through losses. The TCJA limited the current-year deduction for pass-through business losses to $500,000, adjusted for inflation. This limitation no longer applies starting in 2029, not 2026, as per more recent legislative changes. Under Full Extension, it would be extended permanently.

- Higher estate tax exemption. The TCJA doubled the estate tax exemption. It is set to return to its pre-TCJA value, adjusted for inflation, beginning in 2026. The higher exemption value would be made permanent under Full Extension.

- Other provisions. The TCJA made several other individual income tax changes with smaller budgetary impacts than those of provisions listed above. These include the introduction of a capital gains tax preference called Opportunity Zones, the elimination of tax preferences for moving expenses, and changes to tax-preferred accounts for those with disabilities. Each provision is scheduled to expire in 2026 under current law and would instead be made permanent under Full Extension.

While the TCJA also made several temporary changes to corporate taxes, this report focuses on expiring individual income tax and estate tax changes only.

Partial Extension

The Partial Extension scenario is designed to extend the TCJA’s individual tax cuts for most taxpayers while allowing expiration of key provisions for richer families, in keeping with President Biden’s tax pledge. To that end, three changes are made to the Full Extension scenario:

- Expiration of changes to the top two rates/brackets. Under Partial Extension, the TCJA’s lower tax rates are extended for the first five brackets. The sixth bracket taxes income at 35 percent under both current law and the TCJA, though the bracket amount is set to rise in 2026 under current law. The seventh and final bracket taxes income at 37 percent under the TCJA but 39.6 percent under current law. The Partial Extension scenario uses current law parameters for these two brackets.

- Full disallowance of the QBI deduction above threshold. The QBI deduction is designed to phase out above a taxable income threshold only if the income is derived from a service-industry business or the wage and capital structure of the business fails to meet certain tests. Under Partial Extension, the QBI deduction is extended but would phase out for all taxpayers, regardless of industry or other business characteristics.

- Expiration of estate tax changes. Unlike Full Extension, which makes permanent the higher estate tax exemption under the TCJA, Partial Extension allows this change to expire.

The Biden administration has communicated a preference to limit any tax increases to the top 1-2 percent of families in terms of income. This option provides our interpretation of what that could look like.

To be clear: against a current law baseline, which is the official baseline used by government scorekeepers and reflects what is written in law, TCJA expiration does not increase taxes, since the tax system’s reversion to pre-TCJA rules is included in the baseline.

It is also difficult to design a package which cleanly extends tax cuts for those below an income threshold while allowing expiration for those above it without straying too far from the original design of the TCJA. Nonetheless, like all policy debates, discussions surrounding the 2025 TCJA expiration will involve questions about tax policy’s role in shaping the distribution of income.

Clausing-Sarin

In their paper titled The coming fiscal cliff: A blueprint for tax reform in 2025, authors Kimberly Clausing (Eric M. Zolt Chair in Tax Law and Policy at the UCLA School of Law) and Natasha Sarin (Professor of Law at Yale Law School) propose a series of tax reforms that include but are not limited to extending certain TCJA provisions. The paper’s thesis is that TCJA expiration in 2025 provides an opportunity for policymakers to think more fundamentally about reforming taxes, arguing that policymakers should proceed with several specific goals in mind: deficit reduction, progressivity, efficiency, and cooperation on global collective action problems like climate change and corporate taxation. The authors stress that their list of proposed changes is a starting point on which specific reforms consistent with their guiding principles can be designed. In this report, we model one such interpretation of their paper.

The first component of the Clausing-Sarin reform option is a partial extension of the TCJA’s expiring individual income tax cuts. As in Full Extension, the proposal would extend the AMT cuts, the larger standard deduction, the elimination of personal exemptions, the limitation on pass-through loss deductions, and the restrictions on itemized deductions. However, it would make the following modifications:

- Rate cut expiration. The Clausing-Sarin reform would allow rate cuts to expire.

- Expanded Child Tax Credit (CTC). The proposal includes a CTC expansion beyond that of the TCJA design. It would increase the maximum credit value to $2,500 and add an additional $750 for children under age six. It would expand credit eligibility across the income distribution, both to higher-income families (by extending the higher TCJA phase-out thresholds) and to lower-income families (by making the credit fully refundable and removing the earnings phase-in). The proposal would not extend the expiring requirement that qualifying children have Social Security Numbers.

- Deduction for qualified business income (QBI). The reform would allow this provision to expire as scheduled under current law.

- Elimination of state and local tax (SALT) cap workarounds. In the wake of the TCJA’s limitation on the deductibility of state and local taxes on individual tax returns, most states with an income tax have enacted new taxes which allow pass-through businesses to pay tax at the entity level rather than the individual level. Because business state and local taxes are generally deductible in determining net income includable in adjusted gross income (AGI), these laws encourage creative accounting to avoid the additional tax imposed by the SALT deduction limitation. Under the proposal, these so-called “SALT cap workarounds” would be prohibited.

- Estate tax exemption. The TCJA doubled the estate tax exemption to $11.2M in 2018, which we project would be $14.3M in 2026 under full extension. Under current law, it is scheduled fall to a projected $7.2M in 2026. The Sarin-Clausing proposal would lower the exemption even further to its inflation-indexed 2009 level of $5.2M. It would also increase the top estate tax rate from 40 to 45 percent.

In addition to extending and modifying certain expiring components of the TCJA, the Clausing-Sarin proposal also includes a set of more comprehensive reforms:

- Corporate tax rate increase. The proposal would raise the corporate tax rate from 21 percent to 28 percent.

- International tax reforms. The proposal would raise the global intangible low-taxed income (GILTI) effective rate from roughly 13 percent to 21 percent and determine liability on a per-country basis while also ending the exemption on the first 10 percent of tangible assets. It would also repeal the deduction for foreign derived intangible income (FDII).

- Investment income tax reforms. Under current law, when the owner of an appreciated asset dies and transfers ownership to an heir, cost basis for tax purposes is “stepped up” from its purchase price to market value. This tax treatment erases accumulated taxable gains. The Clausing-Sarin reform would change this treatment to “carryover” basis, wherein heirs retain the tax basis of the decedent. In addition, the reform would increase all tax rates on long-term capital gains and qualified dividend rates by 5 percentage points, setting rates at 5 percent, 20 percent, and 25 percent.

- Carried interest tax reform. Current law allows a portion of compensation earned by investment managers, known as “carried interest,” to be characterized as investment income rather than labor income. The proposal would tax this income at ordinary rates.

- Internal Revenue Service (IRS) funding. The Inflation Reduction Act (IRA) allocated nearly $80 billion in mandatory funding to the IRS through 2031, some of which has been cut in subsequent legislation. The proposal would re-establish funding at IRA levels on a permanent basis.

- Uniform treatment of employment taxes. Current law assesses a 3.8 percent tax rate on all income above $250,000 either through employment taxes or the net investment income tax (NIIT). Some owners of pass-through businesses, however, can avoid both taxes by characterizing income as profits rather than wages. The Clausing-Sarin reform option would eliminate this preferential treatment.

- Expensing of research and experimentation (R&E) costs. Current law requires firms to amortize certain R&E expenses over time rather than immediately deduct them, a change implemented in the TCJA. This proposal would return to the pre-TCJA regime of expensing these costs.3

- Premium Tax Credit (PTC) expansion. The American Rescue Plan Act (ARPA) and the IRA expanded the PTC, a subsidy for families to buy health insurance, by covering a greater share of costs and allowing those above an income threshold to qualify. These changes, which are scheduled to expire at the end of 2025, would be extended under this option.

- Earned Income Tax Credit (EITC) expansion. The ARPA temporarily expanded the EITC by roughly tripling the maximum benefit for childless workers, lowering the minimum age from 25 to 19, and eliminating the maximum age cap of 64. The Clausing-Sarin proposes a reinstatement of these EITC parameters.

- Carbon tax. The Clausing-Sarin reform would assess a new tax on carbon emissions, starting at $15 per metric ton and phasing in to an inflation-adjusted value of $65 over time. By exempting exports and taxing imports, the tax would apply only to domestic consumption. Refineries producing home heating oil and retail gasoline would be exempt from the tax.

- Financial transactions tax (FTT). The proposal establishes a three basis point tax on the gross value of most securities transactions.

Footnotes

- This version is designed to align with campaign promises President Biden has made to not raise taxes on those who are not among the highest-earning Americans. It is our interpretation of what that would involve.

- We are not looking at versions of extension that simply once again extend the provisions for 10 years, which is a likely scenario under reconciliation. We feel that it is important to look at the long-run impacts on the budget, economy, and taxpayers under these scenarios and to acknowledge that a 10-year extension sets up likely subsequent 10-year extensions.

- The proposal also makes the credit refundable over four years to be consistent with Pillar 2 international reforms.