July Jobs Day Preview: Approaching the Long-Term

Expectations for the U.S. employment report on Friday are for growth of 177,000 payroll jobs in July, which would raise the three-month moving average to 200,000 per month, and the unemployment rate staying at 4.1%.

As we wrote in our June Jobs Day preview, the best way to reconcile 1) cooling momentum in measures like hires, vacancies, and quits with 2) enduringly high employment levels, especially the prime-age (25 to 54) employment-to-population ratio and 3) low unemployment claims and layoffs is through the lens of a full employment labor market at trend, where falling momentum represents a ceiling with diminishing returns, rather than a recessionary one, where falling momentum represents deteriorating conditions.

Since then, throughout July weekly unemployment insurance claims—one of the best early warning recession indicators we have—have continued to come in at subdued levels. If July job growth comes in fast enough to at least keep up with population growth—110,000 or more—and if prime-age employment in July’s jobs report remains robust, then it is likely that the labor market remained at or near full employment in July.

Being clear on the full employment / recession distinction is not Pollyannaish or triumphalist. It is hard-headed. A full employment labor market is a deeply uncertain one, and without the tailwinds of cyclical momentum that normally help drive growth when, say, the US is bouncing back from the depths of a recession, it is one vulnerable to risks.

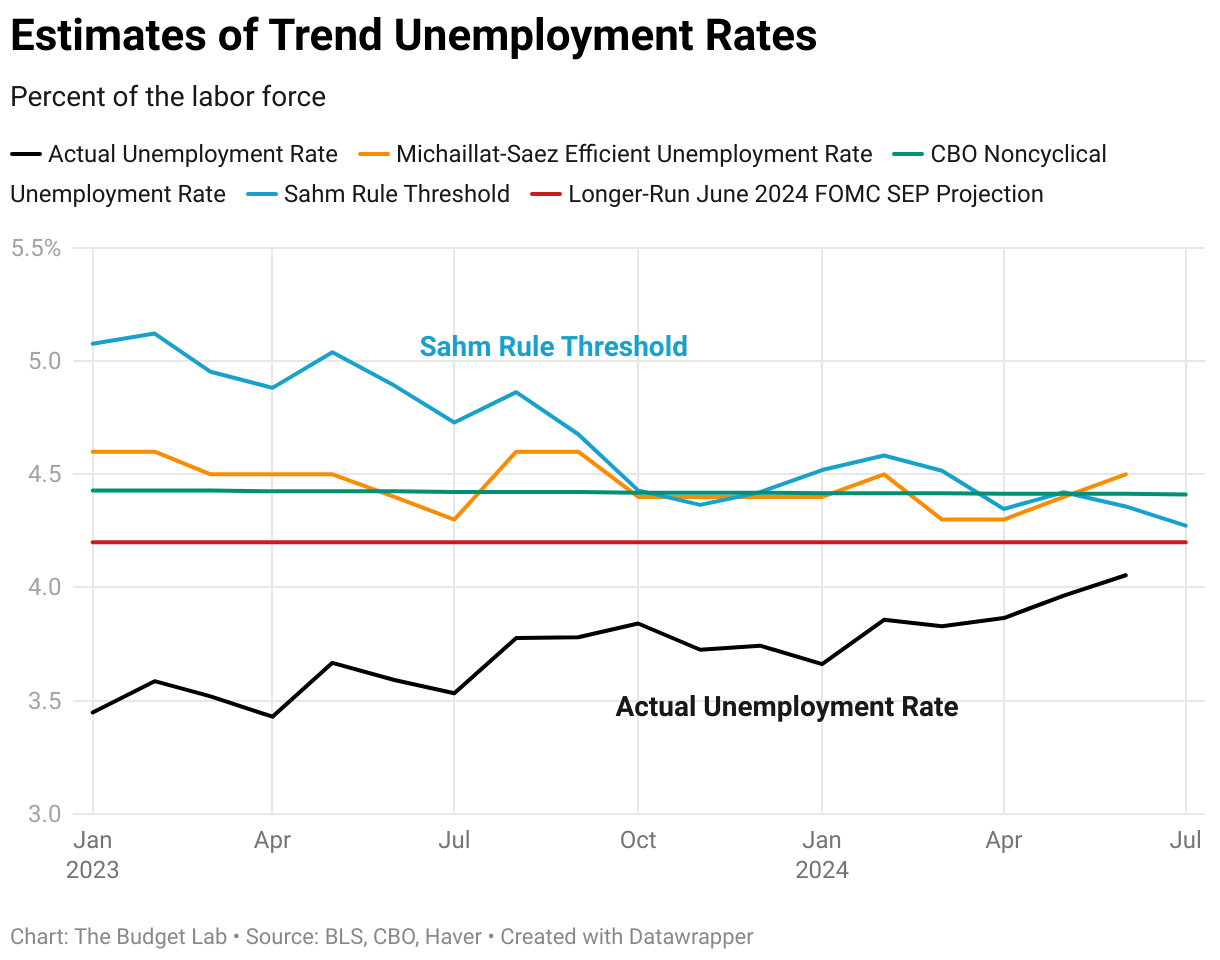

One such risk is that the unemployment rate rises further even absent a recession as the labor market continues to transition into a medium-to-long-run equilibrium. Few economists thought the 3.4% unemployment rate achieved in April 2023 was sustainable for an extended period of time. Even before the pandemic, prominent estimates of the longer-run “natural” rate of unemployment rate tended to cluster between 4 ¼ - 4 ½ %, with others outside that range. Many recent estimates of short- and longer-run “trend” unemployment rates are likewise higher than the June level of 4.1%, suggesting unemployment could have further to go before it settles. The median Federal Open Market Committee (FOMC) participant at the Federal Reserve forecast an unemployment rate of 4.2% over the long run back in June. The Congressional Budget Office (CBO) estimates that the noncyclical rate of unemployment (previously called the non-accelerating inflation rate of unemployment or NAIRU) at the moment is 4.4%. The Michaillat-Saez Efficient unemployment rate, which minimizes the nonproductive use of labor, is currently 4.5%. These metrics measure different concepts at different horizons, but they all suggest that even without a recession, the unemployment rate may land at a somewhat higher level than it currently is now.

The U.S. has not achieved full employment often in its economic history, and it has even less experience being at trend long enough to see these short-to-long run transitions up close in real time. Such transitions could easily be misinterpreted as more common recessionary signals. For example, if the unemployment rate rose further consistent with the aforementioned medium-to-long-run trend estimates, doing so could mechanically trigger the Sahm Rule, an empirical framework for dating US recessions. The Sahm Rule finds that, historically, official US recessions have started when the three-month average of the unemployment rate has risen 0.5 percentage points from its low over the prior year.

An unemployment rate of 4.28% for July will trigger the Sahm Rule, unlikely but far from impossible. But even if July’s unemployment rate comes in lower, the risk remains that future reports in the months ahead could still do so (although the unemployment rate needed to trigger the Sahm Rule will also itself be rising further as last year’s low unemployment rates start falling out of the 12-month window).

Of course, rises in the unemployment rate often do signal a deterioration in labor market conditions; indeed, this is why the Sahm Rule has worked so well in the past at predicting recessions. At the moment however, recent rises in the unemployment rate are coming against the backdrop of a +200K/month pace of job growth, a high level of prime-age employment, and a low level of jobless claims. So as with everything in this full employment economy, observers should be cautious and keep their priors loose. On the one hand, the labor market can deteriorate fast, and there is evidence that even +200K jobs a month (which may be revised down in future benchmark revisions) is not enough to keep pace with the labor supply surge being driven in part by immigration (another source of risk and uncertainty). On the other hand, what we may be witnessing up close with the rise in the unemployment rate is simply something rare and mostly theoretical: a handoff of the labor market from the well-tread short-term to the fabled long-term.