No Tax on Police Officers, Firefighters, Veterans, and Active Duty Military: Basic Background

Last week, former President Trump mentioned he was considering exempting police officers, firefighters, veterans, and active duty military (for the rest of this report: veterans and uniformed & protective services, or VUPS) from federal income taxation. This proposal is the latest in a series of narrowly-focused tax break ideas from former President Trump during the campaign, including exempting tipped income, exempting interest on auto loans, and exempting overtime income.1

This analysis gives an overview of the population that would be covered by this proposal and what the fiscal impact of a federal tax exemption might be. In summary:

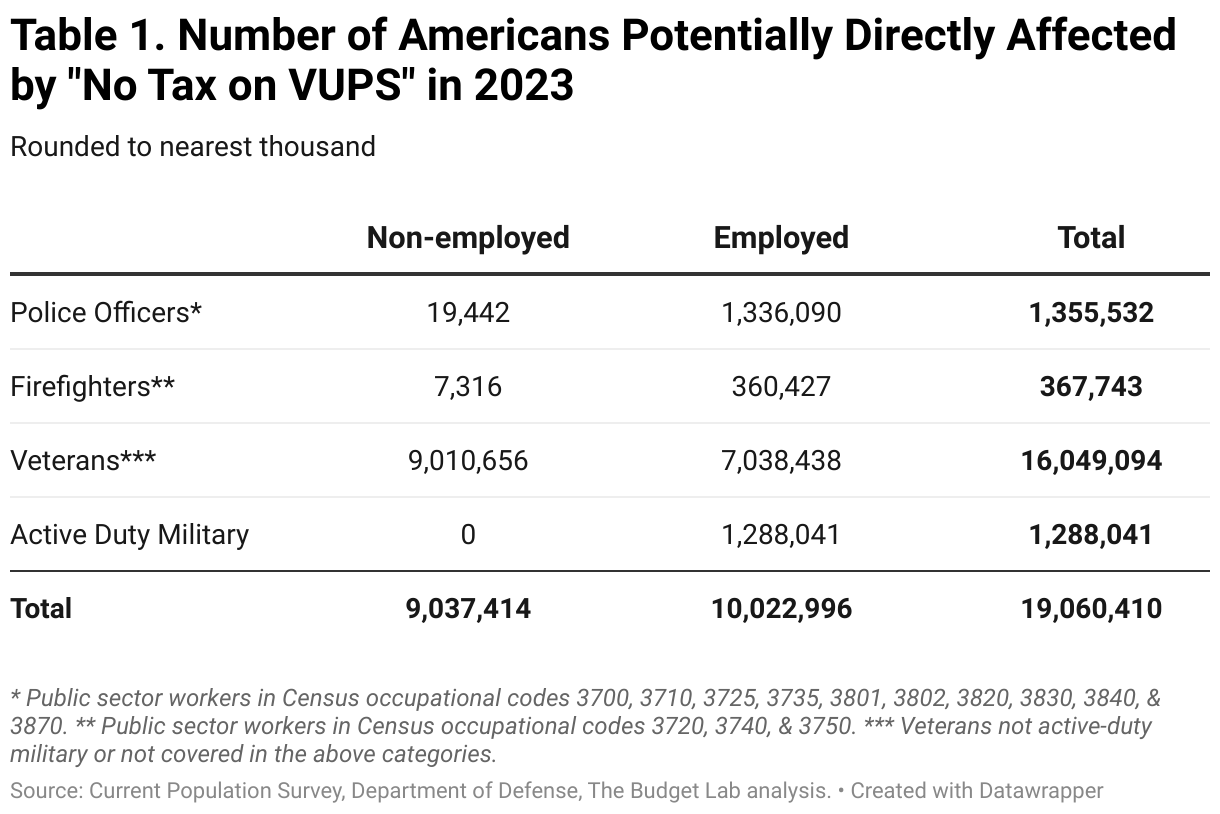

- In 2023, there were 19 million people who would be covered by this new federal income tax exemption; 16 million of these were veterans alone, another 1.4 million were police officers and 1.3 million were active duty military.

- A VUPS exemption would cost $2 trillion over the next 10 years against current policy if applied just to income taxes (0.6% of GDP), and $3.6 trillion if applied to both income and payroll taxes (1% of GDP).

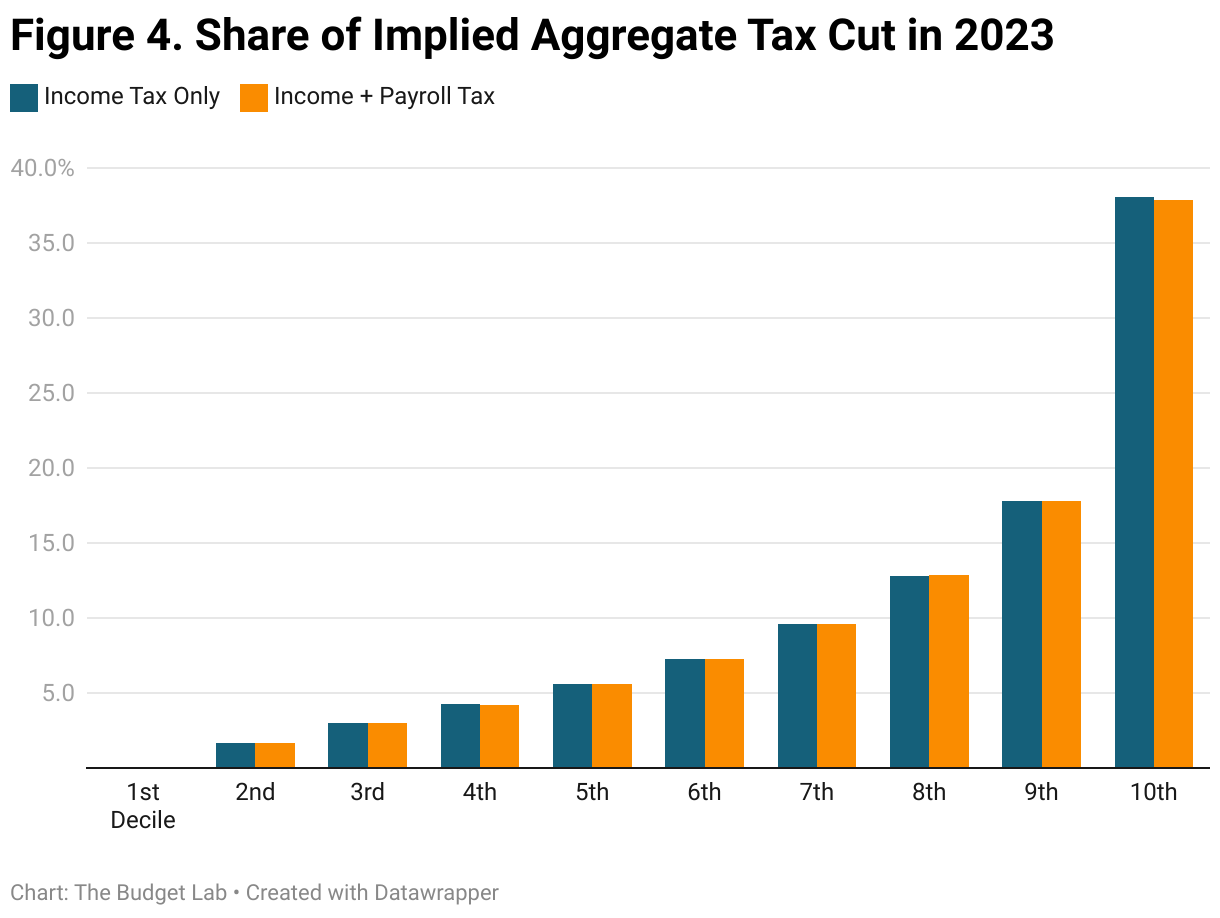

- In 2023, an income tax exemption for this population would have been regressive: more than half of the aggregate tax benefit would have fallen on the top two income deciles.

How many popele would be covered by this exemption?

In total, 19 million people fell into one of the covered VUPS categories in 2023, accounting for roughly 6% of the population (Table 1).2 Of these, just over half—ten million—were employed in 2023. The nine million not employed were overwhelmingly accounted for by veterans, most of whom were retired.

How much would a military, veteran, and first responder exemption have cost in 2023 and what would its distribution have been?

As a cautionary note up front, it is difficult and highly uncertain to reliably estimate the 10-year cost of the exemption former President Trump floated last week. Behavioral responses in particular are a first order consideration. For example, it would be reasonable to assume that in the face of an income exemption for these occupations, more Americans would seek out these jobs in order to avoid federal taxes. In addition, depending on how the exemption were structured — if one could exempt all of one’s income if one was in one of these occupations there would be an incentive to take a part-time job in one of these occupations to ensure that other income was not taxed. Without more details from the Trump campaign, it is difficult to be precise.

Exempting veterans’ income is especially significant given that it has the potential to grant a lifetime of tax-free income to an individual even after they leave military service. This would increase the cost above the TBL estimates here, likely to a significant degree.

That said, even ignoring behavioral effects, exempting 19 million Americans from federal taxation is a substantial proposal. A starting point for sizing the idea is to know how much such an exemption would have cost in the recent past. For this, TBL turned to the Current Population Survey Annual Social and Economic Supplement (ASEC) for 2024, which contains income and tax data for tax year 2023.

Using the CPS ASEC, TBL estimates that filers in covered occupations accounted for $145 billion in federal individual income tax revenue in 2023 and $120 billion of both employee- and employer-side payroll taxes.3 That’s roughly 7% of 2023 income and payroll tax revenues and, combined, 1% of GDP, which, incidentally, is almost exactly the amount the US spent on veterans programs and military retirement combined in 2023 ($242 billion).

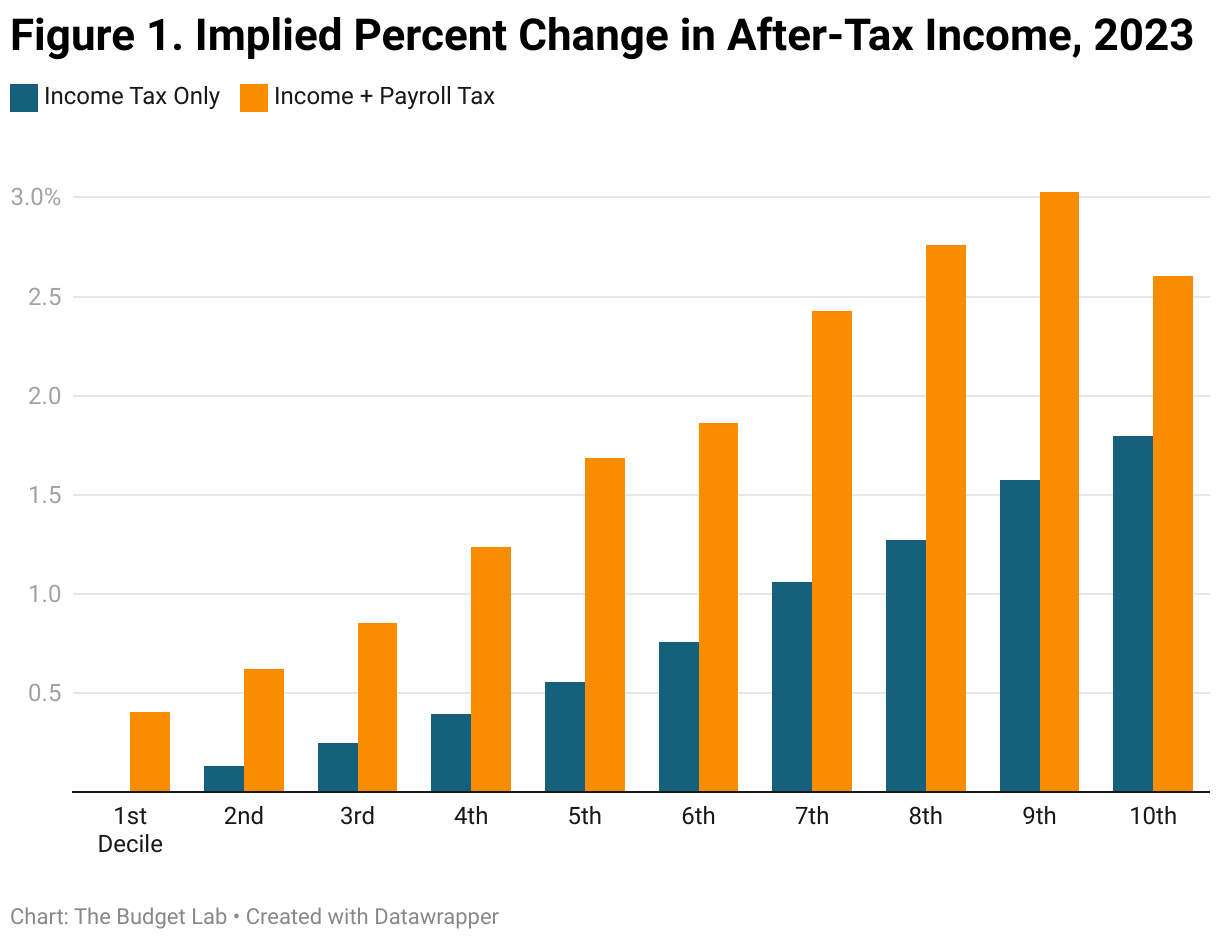

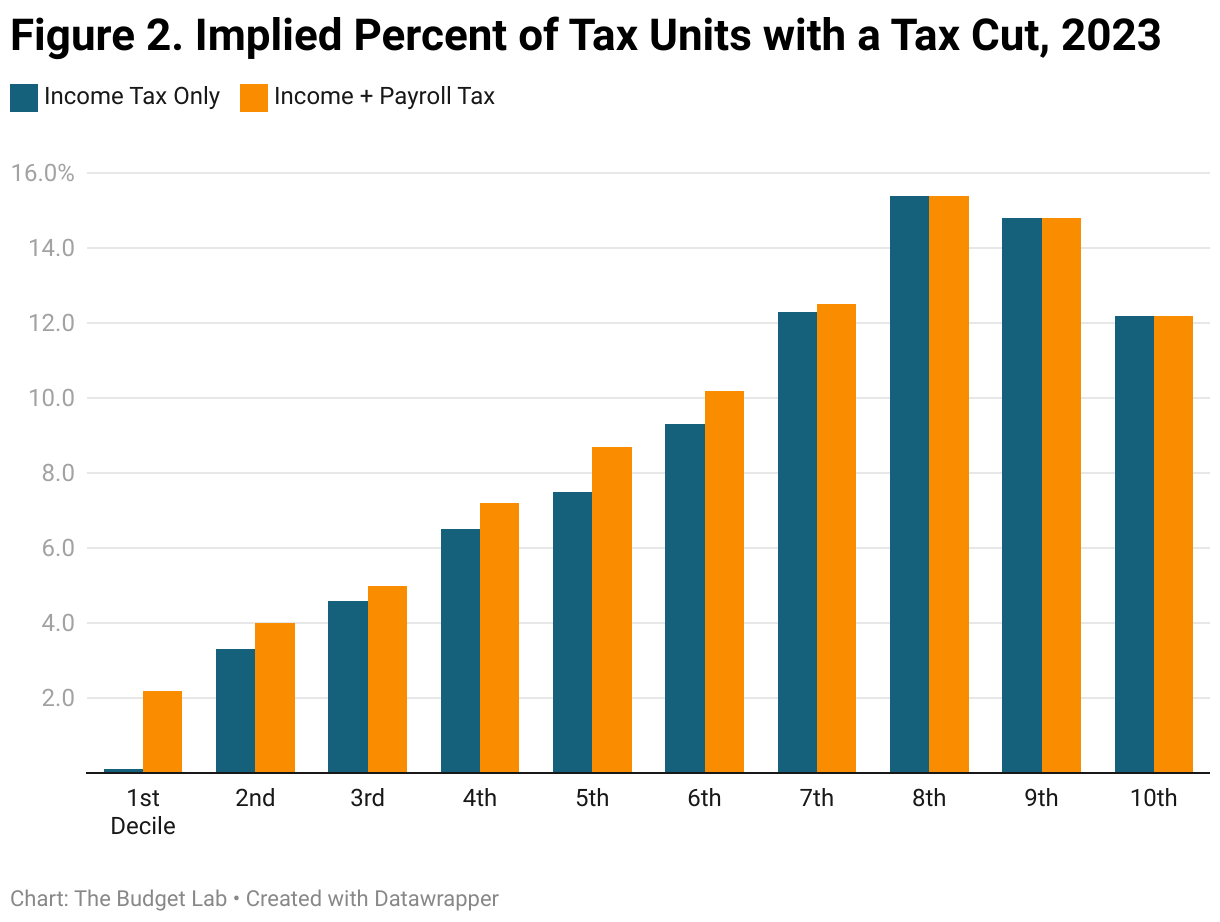

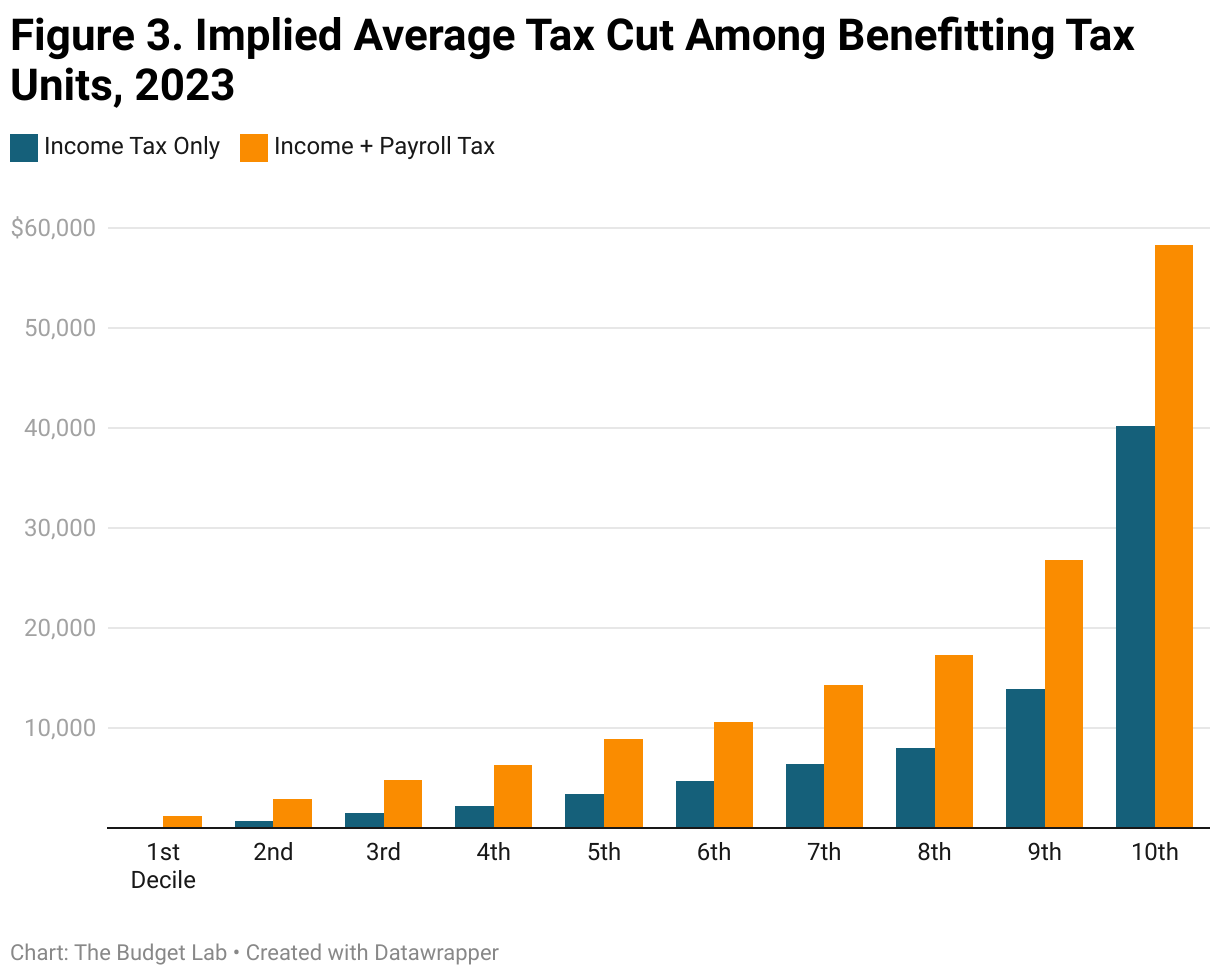

On average across all taxpayers, an income tax exemption would have raised after-tax income by 1.3%, while an income tax and payroll tax exemption would have raised it by 2.4%, but as Figures 1-4 show, the actual benefits would have varied significantly by income. Tax savings from this type of exemption would have been highest at the top decile in 2023 dollar terms, with an average benefit of $40,000 income tax exemption /$58,000 income + payroll tax exemption respectively for beneficiaries in the top decile. As a share of after-tax income, the strongest effect comes in the 9th decile for the combined exemption. More than half of the aggregate tax benefit would accrue to the top two deciles.

How much would the exemption cost over the next 10 years?

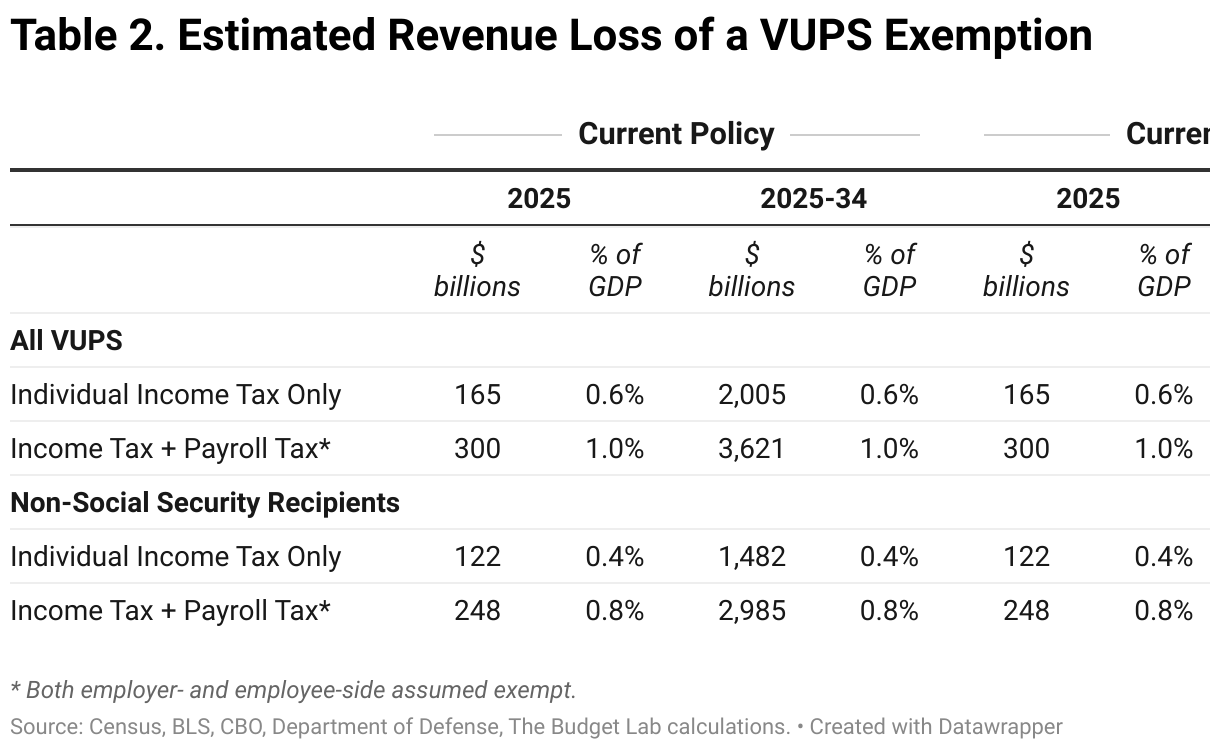

Looking forward, under conventional assumptions (e.g. no assumed employment shifts towards these occupations), TBL estimates that a military, veterans, and first responders exemption would cost roughly $2 trillion over the next decade (0.6% of GDP) if it just applied to individual income taxes, and $3.6 trillion (1% of GDP) if it exempted employee and employer payroll taxes as well (see Table 2). These estimates are against a current policy4 baseline wherein the expiring provisions of the Tax Cuts & Jobs Act of 2017 (TCJA) and all other tax provisions expiring under current law are fully extended.

Excluding Social Security recipients

President Trump has also proposed exempting taxes on Social Security, and a number of veterans receive Social Security payments, creating an overlap with the exemption considered in this analysis. To give a rough sense of how a military, veterans and first responders exemption might “stack” below a Social Security exemption, The Budget Lab analyzed the same two options discussed above but only among eligible Americans with no Social Security income. The incremental cost falls to $1.5 trillion over 10 years (0.4% of GDP) under an income tax-only option and $3.0 trillion (0.8% of GDP) under and income tax + payroll tax option. Bear in mind, these lower scores do not represent “savings,” but rather just smaller costs that can be attributed solely to the military, veterans and first responder exemption versus an already-assumed Social Security exemption.

Scoring against current law, the cost would be higher since post-2025 marginal rates go up under current law, making a tax exemption more expensive. The individual option rises to $2.2 trillion over 10 years while the combined income + payroll option becomes $3.8 trillion (Table 2).

What are the demographics of the affected VUPS groups?

By age

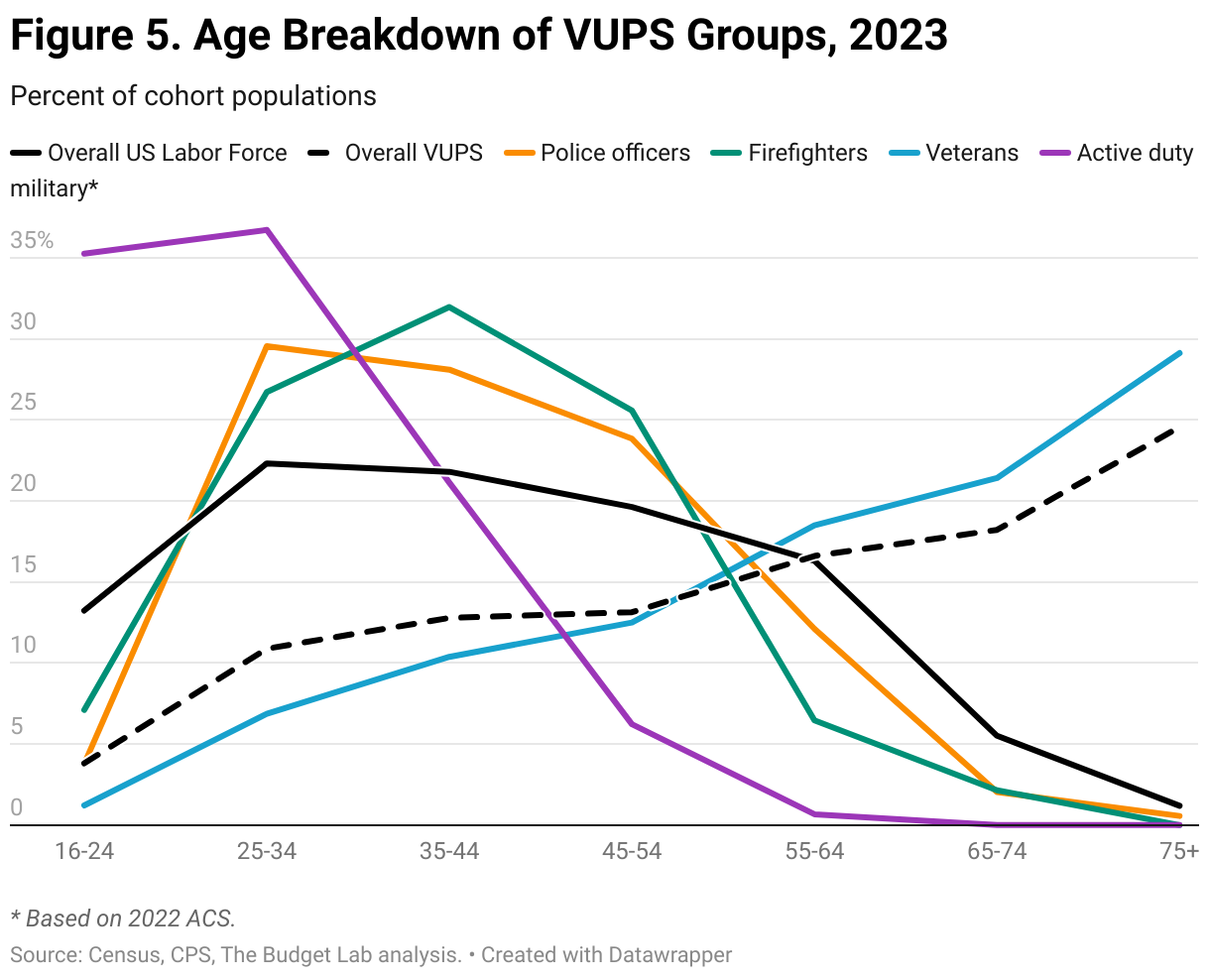

Overall, the population categories covered by Trump’s proposal are older than the overall US labor force. But the categories themselves have very different age profiles. Figure 5 shows the age shares of police officers, firefighters, veterans, and active duty military, as well as for the overall US labor force. Police officers, whose median age was 40 in 2023, and firefighters, 39, skew only slightly younger than the overall US labor force, with a median age of 41. On the other hand, the median age of an activity duty servicemember was 28 in 2022, while the median veteran’s age was 65 in 2023. Since veterans make up more than 80% of the VUPS population, their age profile dominates the overall average.

By race/ethnicity

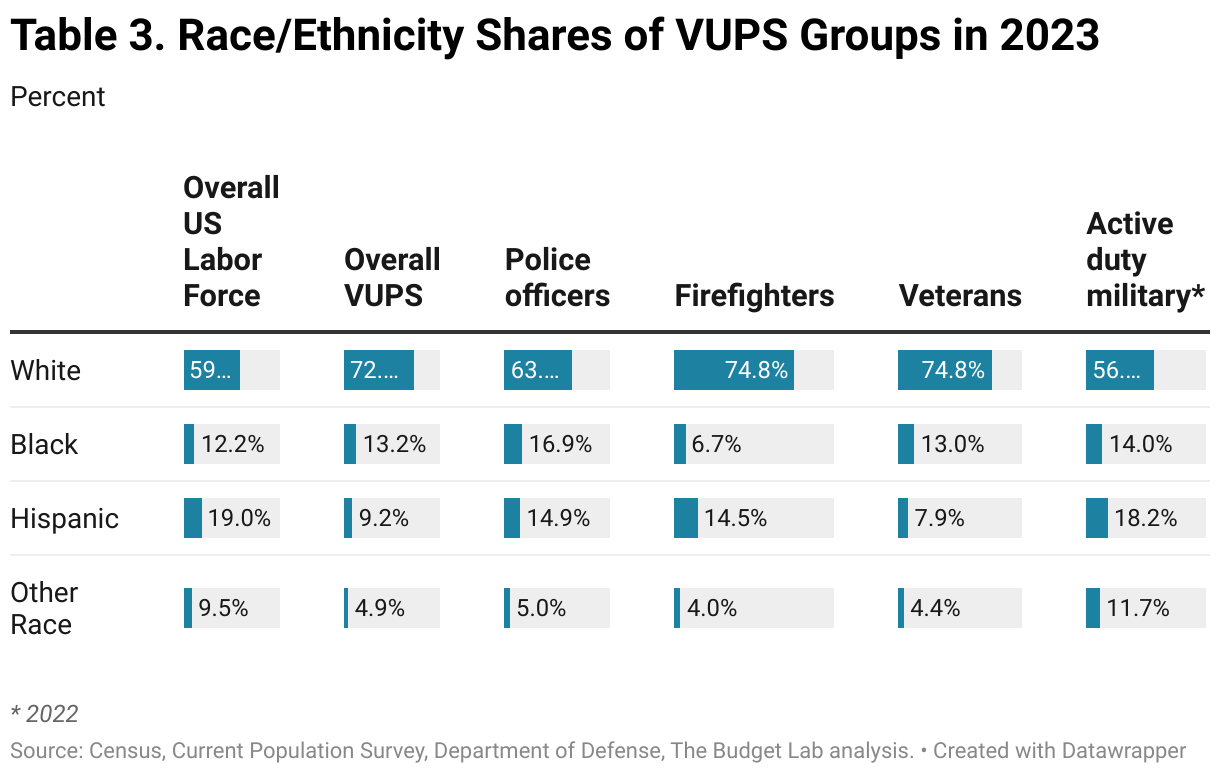

Table 3 below breaks down the VUPS populations by race/ethnicity. As with age, the veterans profile dominates the overall average. As is well-known, the armed forces are more racially diverse than the overall US labor force. Other VUPS groups have higher white shares than the US labor force, while police and veterans have higher Black shares as well. All groups have lower Hispanic shares than the US labor force.

Conclusion

A VUPS exemption would carve at least 19 million people out of the federal tax code. In reality, this number would likely grow as more Americans sought out occupations that promised tax-free income. Putting these considerations aside, TBL estimates such an exemption would cost $2-3.6 trillion over the next decade (0.6-1% of GDP). The proposal would be regressive, with generally higher benefits at higher incomes.

Footnotes

- He has also proposed exempting income from social security, a proposal Budget Lab has not yet scored.

- A basic starting question is how many people fall into the four categories former President Trump mentioned. The Budget Lab (TBL) looked at data from the Current Population Survey (CPS) to get a sense of the non-military population. Some judgement was required in defining “police officer” and “firefighter”. Budget Lab ultimately decided on a definition that included any public sector worker in one of 13 occupations. The Budget Lab defined a “veteran” as anyone in the CPS who ever served in the armed forces and was not currently a police officer, firefighter, or active duty military. Since the CPS only tracks the civilian non-institutional population, data on active duty military counts for 2023 come from the Department of Defense.

- For dual-income filers, TBL allocated individual income taxes before credits to VUPS proportionally based on total individual income. For active duty military, TBL raked the in-sample CPS ASEC active duty military sample to match the age, marriage-parenthood, and income bracket profile of all activity duty military in the 2022 ACS, and then realigned the headcount so that the CPS ASEC active duty military headcount matched the 1.29 million number from the Department of Defense for 2023.

- While Budget Lab generally scores against a current law baseline which better reflects the costs of new decisions Congress would have to make and does not require policy assumptions, we score against current policy here assuming that if former President Trump would be reelected he would extend the expiring tax cuts in the TCJA, and thus a new proposal from him should be “stacked” on top of that existing policy decision.