Deals, Wheels, and Deductions: The Fiscal Effects of a Car Loan Interest Tax Deduction

At a campaign event in Detroit on Thursday, former President Trump called for a new tax deduction for interest on car loans. This idea is the latest in Trump’s growing list of proposed tax breaks for specific forms of income or spending, including tax exemptions for tips, overtime pay, and Social Security benefits—policies which the Budget Lab has analyzed in a series of reports (I, II, III, IV).

Below, we estimate the first-order budgetary and distributional effects for a car loan interest deduction and describe how these effects might change when considering behavioral feedback. Depending on how the deduction is structured, it could have a budgetary cost of up to $173 billion over ten years. While more than one in four families in most income quartiles would benefit from the proposal, the tax break would be relatively small (less than $250 for most income groups) and increase after tax income of filers by less than 0.2% across all income groups.

How would a tax deduction for car loan interest work?

There are two types of income tax deductions: above-the-line deductions, which subtract from gross income, and itemized deductions, which subtract from taxable income for those with eligible expenses in excess of the standard deduction. Because only about one in ten families itemize their deductions, the tax benefit of itemized deductions skews towards higher-income taxpayers. That’s in contrast to above-the-line deductions, which produce tax savings for anyone with positive income.

Prior to 1987, most personal interest expenses, including interest on car loans, could be written off as an itemized deduction. Under current law, only mortgage interest and certain investment interest are available as itemized deductions. Student loan interest is available to some taxpayers as an above-the-line deduction. (Whether interest should be deductible at all is an interesting theoretical question.)

It is not clear which kind of deduction former President Trump has in mind for car loan interest. The basic tradeoff is this: an above-the-line deduction would benefit more taxpayers and have a more progressive distributional impact, but these benefits would come at a higher revenue cost to the government. We analyze both potential designs in our quantitative analysis below.

How much would this tax break cost—and who would benefit?

The budgetary and distributional impacts of a car loan interest deduction depend in part on who pays car loan interest and how much they pay. Because there is no such tax break under current law, the IRS microdata which underlies our tax model doesn’t include the information we need to evaluate these effects. That means we have to look at other data sources and incorporate that information into our model.

To do so, we use microdata from the 2022 Survey of Consumer Finances (SCF) to estimate the statistical relationship between income, demographic characteristics, and car loan interest. Then, we use those relationships to impute car loan interest for all records in our simulated population of tax filers. For more information on our procedures and assumptions, including links to the code used to produce the calculations, please see the Appendix below.

We estimate that, in 2022, about one third of tax units paid car loan interest for a total of $65 billion. But since that year, interest rates on car loans have doubled. As a result, we nowcast strong growth in total interest paid: our projection for 2024 is $85 billion, and our projection for 2026 is $93 billion, reflecting the roll off of lower-interest loans. In the latter half of the decade, we expect that growth will be slow due to moderating interest rates.

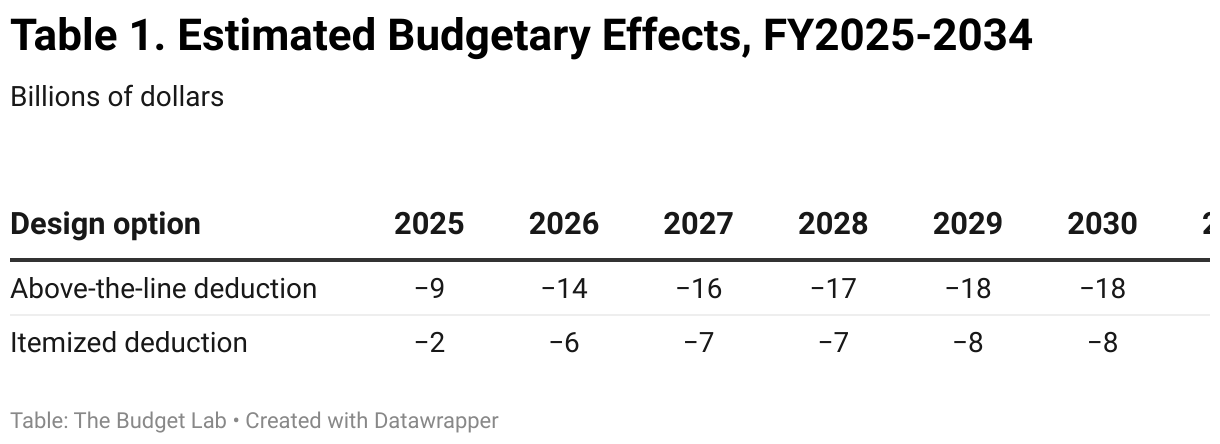

Table 1 presents estimated static ten-year budget costs for two versions of the policy: an above-the-line deduction ($173 billion over the window) and an itemized deduction ($71 billion). These numbers do not include the effects of behavioral feedback.

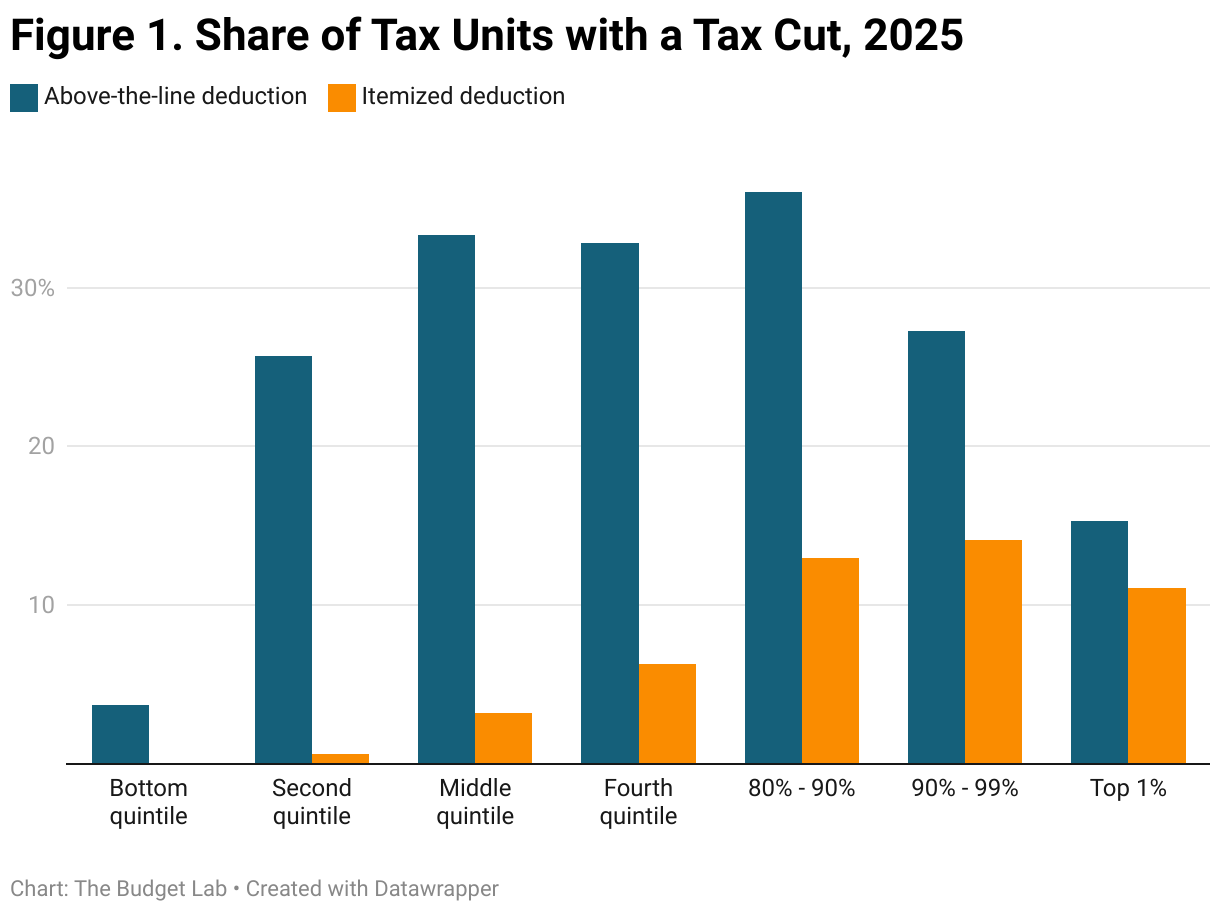

To assess the distributional impact of this idea, we ask three questions and calculate the answer by income group. First, what share of taxpayers would benefit from a car loan interest deduction? Second, among those who benefit, what would the average tax cut be? And finally, how large is the overall effect relative to after-tax income?

Figure 1 shows the estimated fraction of tax units in each group that would see a tax cut in tax year 2025. As described above, a smaller fraction of taxpayers in each group would benefit from an itemized deduction design relative to an above-the-line deduction design. Though many bottom-quintile families pay car loan interest, most don’t have any taxable income to begin with, and so would not benefit—a recurring theme of Trump’s recent proposed tax breaks.

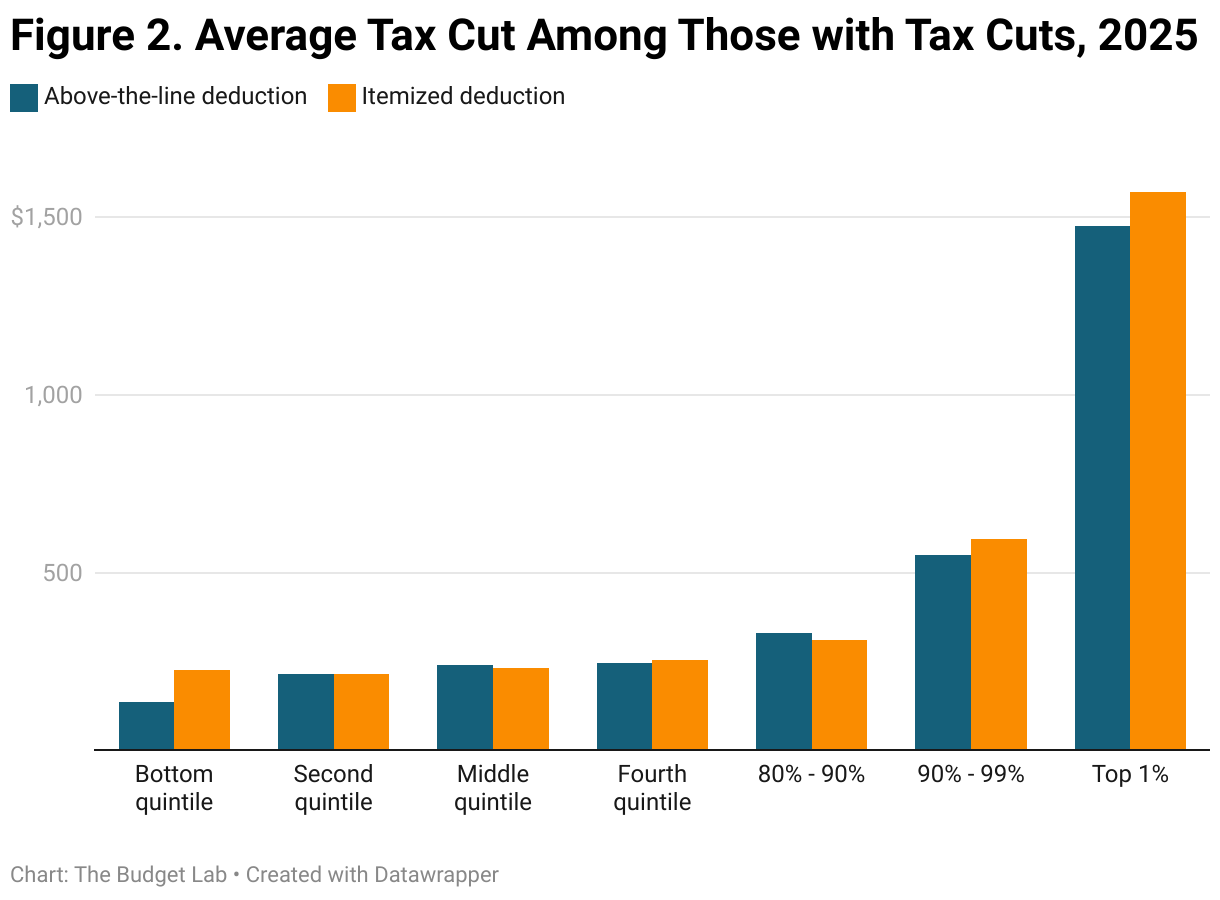

Next, Figure 2 shows the average tax cut among those who benefit from the new deduction. For those in the bottom 90% by income, average tax savings would generally be in the $200-$300 range. But the savings would be largest for those at the top, since deductions create larger savings for those with higher tax rates and the income tax is progressive. The average benefit for those in the top 1% would be closer to $1,500.

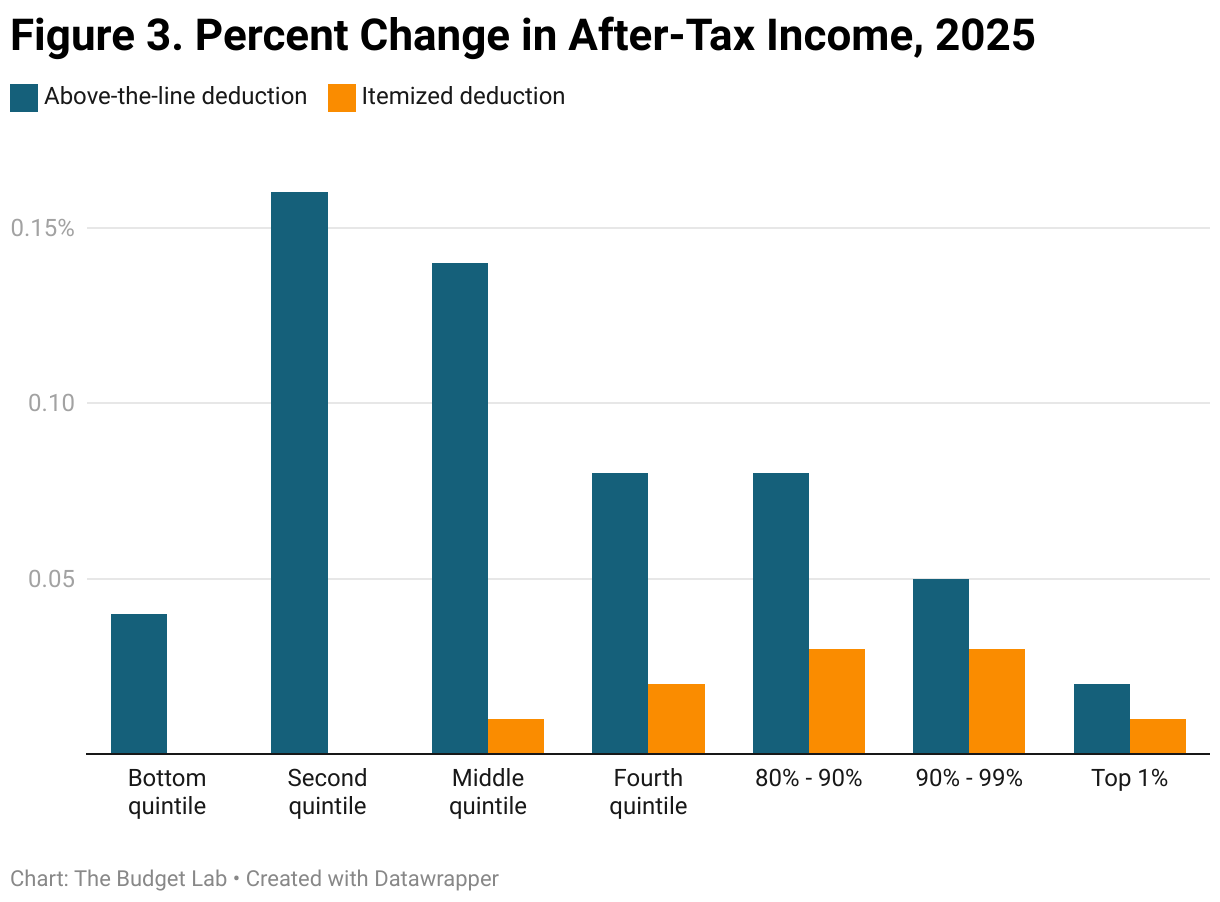

Finally, Figure 3 shows the overall impact in relative terms. These tax breaks would represent a small (less than 0.2% of income) increase in after-tax income for all groups. Excluding the bottom quintile, that small change would be distributed progressively because car loan interest is a larger share of income for lower-income groups than higher-income groups—enough to offset the fact that deductions generate larger tax savings for higher-income taxpayers.

It’s worth noting that these estimated distributional impacts would change somewhat in 2026 if the Tax Cuts and Jobs Act’s (TCJA) individual tax provisions expire as scheduled under current law. Because the standard deduction would fall and several restrictions on itemizing would be lifted, a greater fraction of taxpayers would itemize and thus benefit from an itemized deduction for car loan interest. Tax rates would also be slightly higher, which leads to larger tax savings per dollar deducted.

How might taxpayers respond?

The numbers in the previous section are static estimates—that is, they do not account for additional revenue loss generated by behavioral feedback. But there are several margins through which taxpayers and other actors in the market for vehicles might respond to a new tax break for car loan interest, all of which could increase the budget cost:

- Increased demand for cars. A tax break for car loan interest makes buying a car on credit cheaper, all else equal. As a result, consumer demand for cars would increase, which might manifest at the extensive margin (more cars purchased, perhaps coming from would-be lessees) or the intensive margin (a shift towards nicer or larger cars). To what extent this increase in demand gets capitalized into car prices depends on supply and demand factors, but evidence from similar policies indicates that higher prices are a possibility.

- Increased demand for financing car purchases. Right now, the fraction of car purchases that are financed is 80% for new vehicles and about a third for used vehicles. These numbers might increase if a tax subsidy is made available, as might the share of the purchase price that is financed.

- Bundled services in purchase price. Car manufacturers and dealers would have an incentive to bundle more services into the purchase price of a car if those services are made cheaper by a tax subsidy. The extent to which this would be possible would depend on legislative and regulatory language.

Conclusion

A deduction for car loan interest is the latest example of former President Trump’s proposed tax breaks for specific forms of income or spending. Like the other proposals, this one would worsen horizontal inequities within the existing code by creating a wider range of tax rates within income groups. Its budgetary and distributional effects would depend on exact policy design: an itemized deduction would reach a smaller, more affluent subset of families, while an above-the-line deduction would deliver tax cuts to a broader swath of the population at a higher budget cost.

Appendix

To construct microdata on car loan interest, we use data on automobile loan balances and loan interest rates from the Federal Reserve Board’s 2022 Survey of Consumer Finances (SCF). The SCF is a triannual survey of 4,600 households that asks detailed questions of income and wealth, including car loan balances and each loan’s interest rate. WE estimate annual car loan interest as the interest rate on each respondent's car loan times their reported outstanding balance. We only include interest on vehicle loan balances that applied to automobiles specifically; we exclude interest on loans for non-auto vehicles loans such as those for RVs, mobile homes, boats, and aircraft. The code for these procedures can be found here.

This procedure yields an SCF estimate of $46.8 billion in aggregate auto interest payments in 2022. For comparison, aggregate “vehicle finance charges” in the Bureau of Labor Statistic’s Consumer Expenditure Survey (CEX) — another small survey of households with a sample size of about 7,000— totaled $39.6 billion in 2022 and $48.6 billion in 2023. This is broadly consistent with our SCF calculation.

One caveat about the SCF data is that it appears to underestimate the size of the aggregate vehicle loan balances. Federal Reserve G.19 data show a total of $1.5 trillion in outstanding vehicle loan balances as of 2022, while the FRBNY Consumer Credit Panel shows an aggregate of $1.55 trillion. The SCF meanwhile suggests vehicle installment loan balances totaled $967 billion in 2022, more than 1/3 less. The driver of this discrepancy is unclear. One possibility is that it may be related to well-known issues that plague the SCF when measuring student debt, which is that definition of the primary economic unit in the SCF will miss adult children living with parents and therefore those children’s student debt, leading to an underestimate in the survey. Young adults under 35 do indeed account for less of a share of vehicle loan balances in the SCF than older cohorts. But, unlike with student loans, this result is not necessarily surprising. Moreover, if the totality of the discrepancy with the G.19 data were accounted for by young adults, it would imply that young adults have substantially more vehicle debt than older cohorts, which contradicts data from the Consumer Financial Protection Bureau (CFPB) showing that new car loan originations for the 30-44 cohort are consistently more than double the value of those for the <30 cohort, and that originations for the 45-64 cohort are even larger still.

Next, our methodology requires converting from the SCF primary economic units to the tax units of our microsimulation model. To do so, we estimate the conditional distribution of car loan interest as a function of wage percentile, marital status, parent status, and age using quantile regression forests. We then assign values to the tax data by randomly sampling from these distributions and project values into the future by assuming that interest expense growth with the Congressional Budget Office’s (CBO) economic projections of interest income. (The code for this imputation can be found here; the version of Tax-Simulator used to run the scenarios in this report can be found here.)

In the resulting imputed tax unit-level data, our estimate of aggregate car loan interest in 2022 rise to $65 billion, or 38% larger than the raw SCF estimate. This closes virtually the entire 41% gap between the SCF and the G.19 vehicle loan balances in 2022.