Beneficiaries of a Fully Refundable CTC Would Change from Year to Year

Key Takeaways

-

Because of its earnings requirements, the current Child Tax Credit (CTC) design means that some families receive a smaller credit if their income drops temporarily.

-

Among parents who don’t earn enough to qualify for the full CTC this year, two-thirds will earn enough next year. This suggests that many low-income parents are experiencing temporary, not permanent, economic hardship.

-

The fraction of parents who would benefit from full refundability in a given year is an estimated 19 percent. But across a two-year period, that figure rises to 32 percent.

(Note: the code used to produce the calculations in this report can be found here.)

The Child Tax Credit (CTC) is one of many income tax provisions scheduled to become less generous at the end of 2025, when key pieces of the Tax Cuts and Jobs Act (TCJA) expire. In this context, lawmakers and policy groups alike have offered CTC reform proposals for potential inclusion in a TCJA extension package.

One CTC design question that has received attention in recent years is the credit’s eligibility rules. Both the TCJA and pre-TCJA tax codes leave about one-quarter of families unable to receive the full credit due to restrictions based on earnings and tax liability. But in 2021, the American Rescue Plan Act (ARPA) made the credit fully available to parents with low incomes by removing these restrictions. This change, commonly referred to as “full refundability,” has been the subject of many analyses finding positive impacts for the finances and longer-term outcomes of low-income families.

This discussion, however, can sometimes paint a picture where income is a fixed attribute: a family is considered either low-income or not, and therefore either gains from full refundability or doesn't. But in reality, many filers who don't receive the full CTC are experiencing temporary, not chronic, income shortfalls.

For that reason, one overlooked benefit of full refundability is how it would strengthen the CTC’s role as social insurance—that is, public financial protection against the ups and downs of economic life. In this blog, we show that most parents who don't earn enough to qualify for the full CTC in one year do earn enough the following year. This means that full refundability would benefit a larger number of parents over time than what a one-year snapshot indicates.

The CTC Tries to Accomplish Several Goals at Once

To understand the debate around full refundability, it’s helpful to think through what goals the CTC might be trying to accomplish:

Horizontal equity. Horizontally equity is the idea that taxpayers with similar resources should pay similar amounts in tax. The CTC makes taxes fairer “horizontally” by adjusting tax burden for family size—for example, recognizing that a family of four earning $50,000 is worse off than a single worker making $50,000.

Vertical equity. In contrast, vertical equity is the principle that tax burdens should rise with ability to pay. The CTC promotes vertical equity by being generally progressive: a $2,000 credit is worth more to a family making $50,000 than to a family making $350,000. The credit also phases out at high incomes.1

Social insurance. Having children can disrupt parents’ participation in the labor market—especially for mothers, who face a “child penalty” on average. By increasing after-tax income for those who qualify, the CTC can act as insurance against the labor market downsides associated with raising children.

Work incentives. The CTC phases in with earnings. This feature reduces effective marginal tax rates for low-income workers and thus encourages certain parents to join and stay in the labor force rather than spend time at home with children, all else equal.

These goals are often in tension with one another. For example, the credit’s phase-in design increases labor force participation (greater work incentives) but at the cost of excluding low-income families (less vertical equity). Similarly, the credit’s phase-out design, where high-income households lose eligibility for the CTC, makes the tax code more progressive (greater vertical equity) but at the cost of losing a tax adjustment for family size at high incomes (less horizontal equity). The priority Congress has given to each of these goals has varied over time, resulting in a range of policy designs for the CTC.

The CTC's Phase-In Design Exacerbates Income Shocks

Another tradeoff between CTC goals is work incentives versus social insurance.

There are two ways fiscal programs can act as social insurance. The first is through a "fixed benefit" design that provides a stable floor of support regardless of income fluctuations (for example, Social Security benefits in old age). For parents whose earnings are always high enough to qualify for the full credit, the CTC provides this type of security.

The second mechanism is a "variable benefit" that increases when income falls (for example, unemployment benefits that kick in after job loss). Most parts of our progressive tax system work this way: if your earnings drop, you pay proportionally less in taxes, helping cushion financial blows.

But for lower-income parents, the CTC's phase-in design actually works in reverse. When their income falls, their CTC amount falls too, amplifying rather than softening the financial shock. This is the necessary flip side of rewarding higher earnings with a larger credit, which means that the work incentive goal and the social insurance goal of the CTC are inherently opposed.2

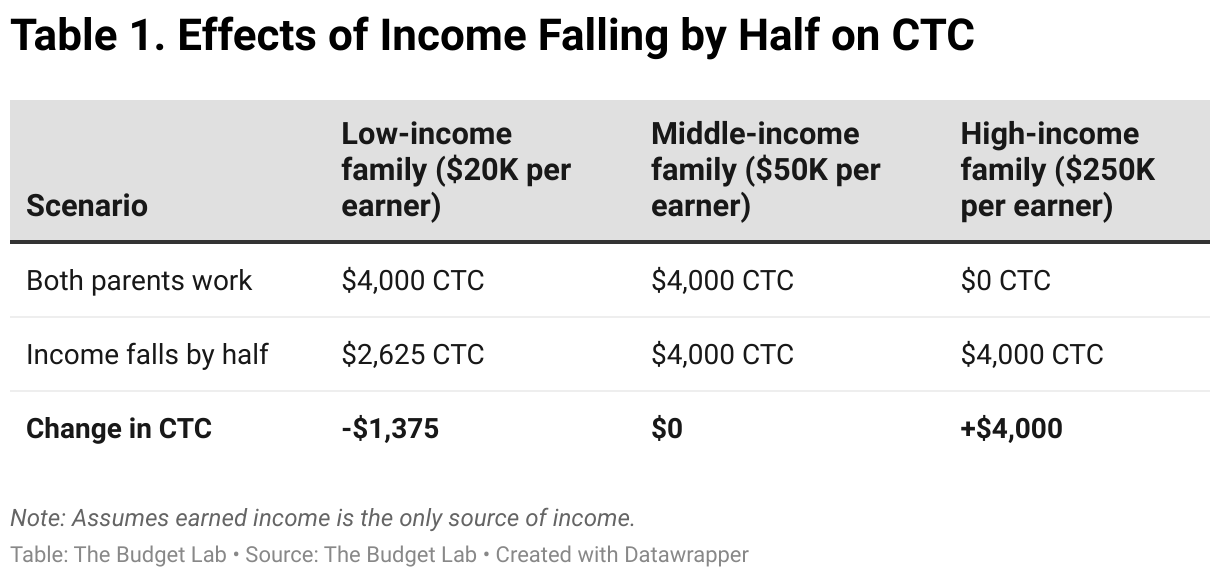

Table 1 illustrates this dynamic with examples. When a low-income family's earnings fall by half, they lose much of their CTC, making their financial situation even worse. Meanwhile, middle-income families keep their full credit when income drops, and high-income families can actually gain CTC benefits when their income falls (due to the phase-out).

Many Parents Are Only "Low-Income" Temporarily

How much does this dynamic—the CTC’s tendency to exacerbate negative income shocks for certain parents—matter in practice? The answer, in part, depends on how much income volatility we see in the real world. If it's common for parents to move in and out of the phase-in range, then policymakers may wish to focus their attention on the social insurance objectives of the CTC.

We can measure parents’ income volatility using Census survey data, which tracks the earnings of families across consecutive years. In each year, we determine whether parents had enough earnings to qualify for the full CTC or whether they were only eligible for a partial (or no) credit.3 Then, we calculate the fraction of parents moving in and out of these situations across years.

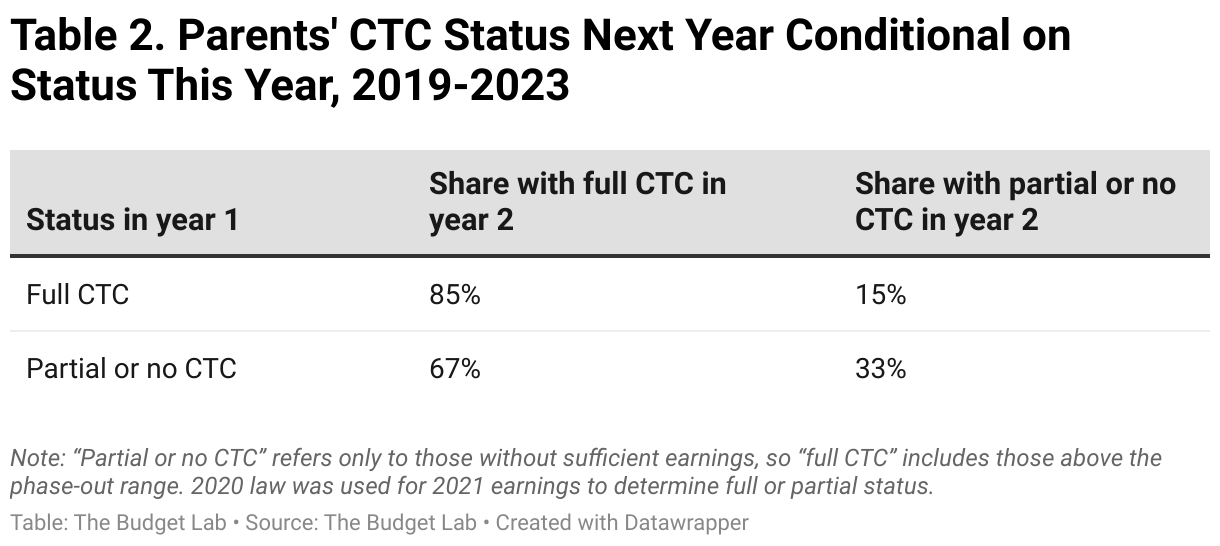

Table 2 shows the results. We estimate that two-thirds of parents who don't earn enough to qualify for the full CTC in one year do earn enough the next year. In other words, many parents are shuffling in and out of the CTC’s phase-in range rather than being stuck there permanently.

These numbers imply a high degree of year-to-year income fluctuations for parents towards the bottom of the U.S. income distribution, a finding backed up by the academic literature on mobility. Research using administrative data has repeatedly shown that family income exhibits substantial volatility due to factors like changes in labor force participation, marriage or divorce, and career switches. For example:

Larrimore, Mortenson, and Splinter (2015) find that more than one-third of bottom-quintile tax units experience income gains of at least 50% over a two-year timeframe. In a separate paper from 2022, the same authors show that 40 percent of those in poverty in 2007 were out of poverty the following year.

The Congressional Budget Office (2008) finds that 40 percent of workers aged 25 to 55 experience a one-year change in wages of at least 25 percent.

Splinter, Diamond, and Bryant (2009) show that over a three-year period, half of bottom-quintile households experience a 30 percent or greater increase in wages, and one quarter of middle-quintile households see a decline in wages of at least 10 percent.

The Congressional Research Service reports that one-third of Earned Income Tax Credit claimants did not claim the credit the prior year, most likely because their earnings were too high.

Point-in-Time Estimates Understate the Reach of Full Refundability

Finally, an important implication of our analysis is that full refundability would benefit a wider segment of the population than is suggested by point-in-time distribution tables. If limiting our view to a single year, the fraction of parents who would benefit from full refundability is about 19 percent. But across a two-year period, that figure rises to 32 percent.

This is a specific case of a more general issue with cross-sectional distribution analysis, which tends to understate the reach of safety net programs. Policies are often sometimes described as helping groups like “parents”, “the bottom quintile”, or “senior citizens” based on point-in-time numbers. But it’s important to remember that these groups are not fixed over time, which means that more people benefit from social insurance programs when you look at a wider timeframe.

Conclusion

Our calculations paint a different picture than what is often assumed about the would-be beneficiaries of a fully refundable CTC. Rather than being in a class of permanent nonworkers, most of the parents who don’t earn enough for the full CTC in one year go on to earn enough in the next. Low incomes are often a temporary experience. It is important for policymakers to consider their overall goals for the CTC and also the full range of who benefits over multiple years when deciding policy.

Footnotes

- We say “generally” progressive become the CTC’s phase-in, described below, reverses this trend at the bottom of the income distribution.

- Other researchers have noted this effect empirically; see Bitler, Hoynes, and Kuka (2017) and Larrimore, Mortenson, and Splinter (2015).

- We use the results of the Census’s tax model for imputing tax units and dependents within survey households. This survey-based approach may overstate the volatility of CTC eligibility across years, since evidence suggests some parents are able to strategically reallocate dependents between tax units within the same household over time (Splinter, Larrimore, and Mortenson, 2017).