Distributional Effects of Selected Provisions of the House Reconciliation Bill (Preliminary)

Key Takeaways

-

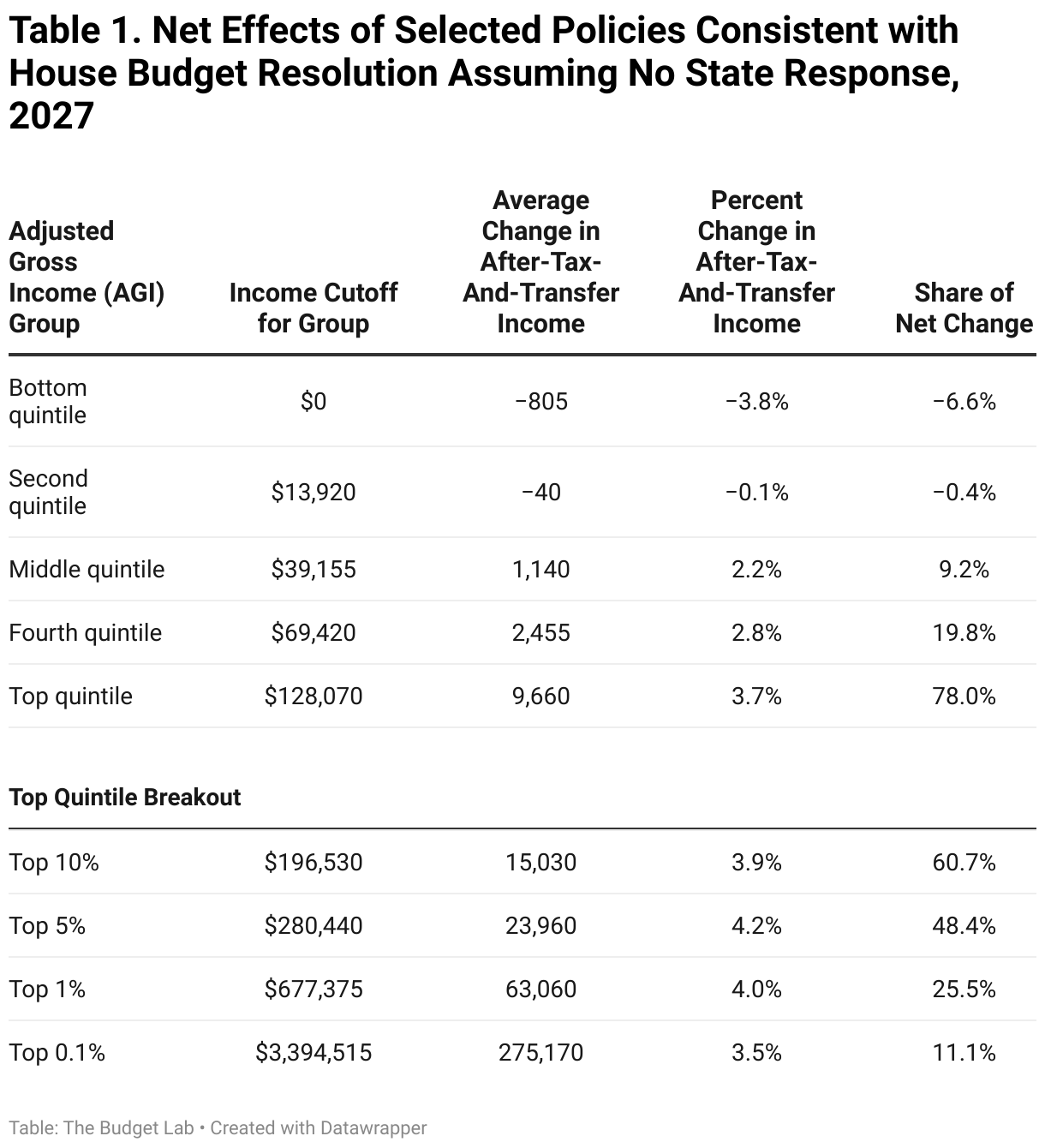

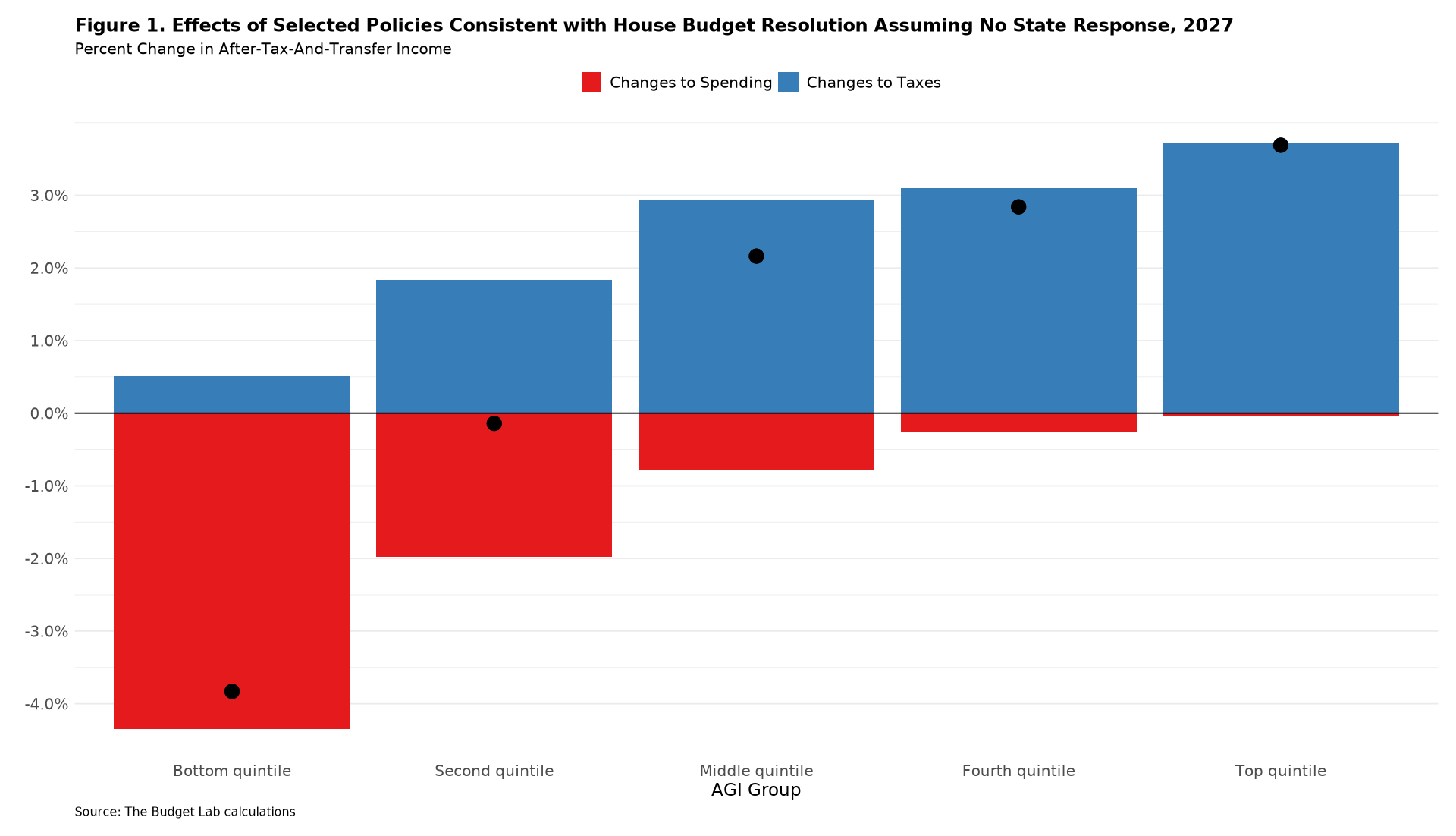

Changes proposed by the House budget resolution would result in a decline of almost 4 percent (over $800) to income for the bottom quintile, but an increase of over 4 percent (nearly $70,000) for the top 1 percent. These estimates assume that states do not offset cuts to social safety net programs included in the resolution.

-

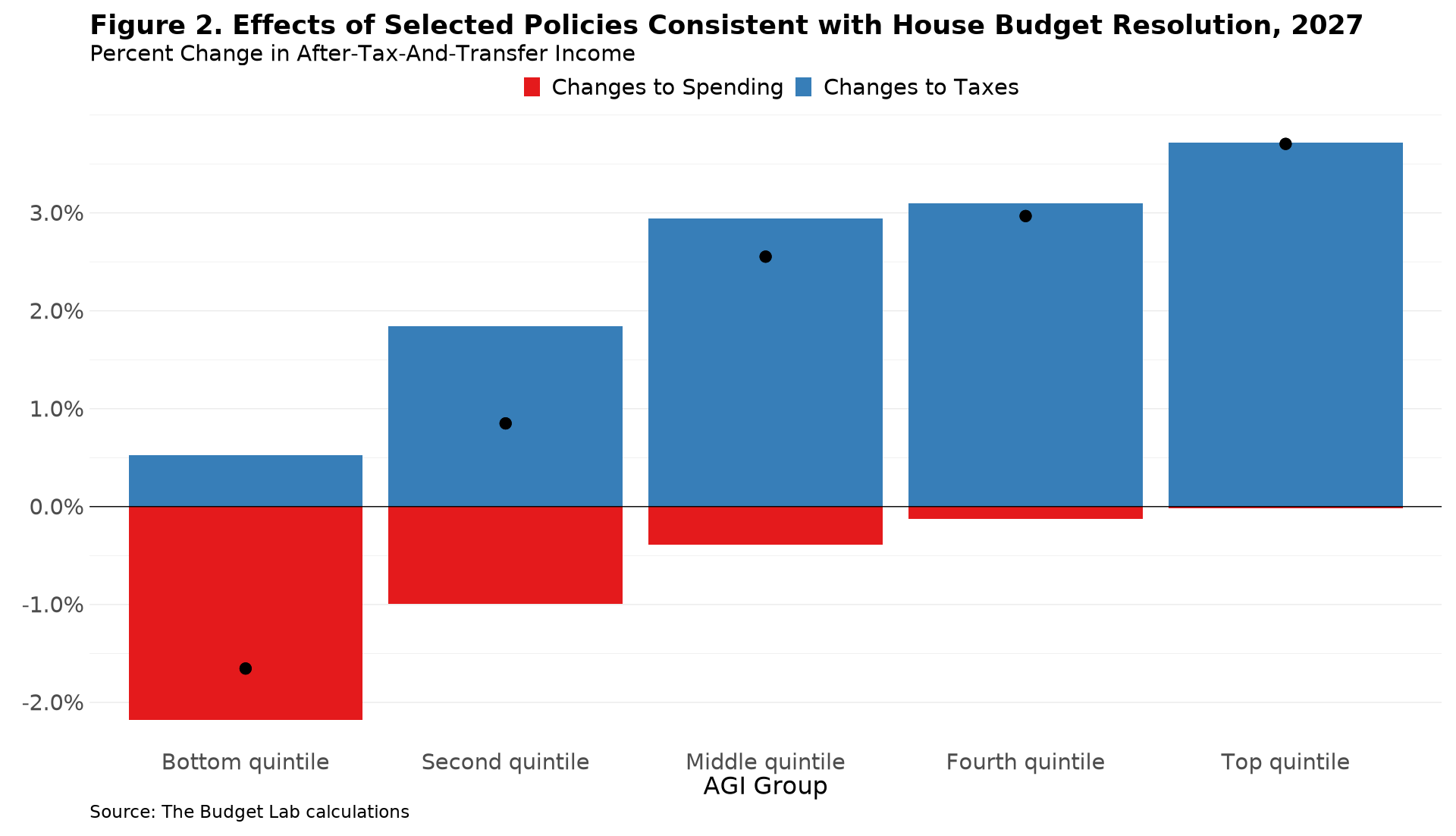

Even assuming that states make up some of the cuts, the bottom quintile would see an income loss of about 2 percent ($345). Note that this does not account for how states may finance these expenditures – if states do so through tax increases or through cuts to other spending, the overall distributional effect may be different.

-

Policymakers have said that they will partly pay for the spending in this legislative package through tariffs. As previous Budget Lab analysis has shown, assuming that tariffs remain in place, the overall impact on families would be even more regressive.

Note: The original version of this analysis mistakenly excluded the phaseout of the SALT deduction maximum in the Ways and Means Committee bill. This error has been corrected.

This report analyzes the distributional effects of selected provisions of the reconciliation bill currently under consideration by the House of Representatives, updating previous analysis from The Budget Lab to account for the full set of tax provisions included in our preliminary score of the Ways and Means Committee’s bill. (That analysis found that those changes would add $3.4 trillion to the debt over the 2025-2034 window and $15.3 trillion from 2025-2055.) We plan to update this analysis further with additional detail on provisions included in the broader House budget bill. (We also do not include the distributional effects of tariffs in this analysis, though we plan to do so in forthcoming work.)

Our analysis accounts for the following tax provisions included in the Ways and Means Committee’s reconciliation instructions: TCJA extension, SALT reform, standard deduction reform and temporary expansion, temporary exceptions for certain forms of income and expenses (tips, overtime, auto loan interest), Child Tax Credit reform, and qualified business income deductions. Further, we also model changes to the estate tax and to business expensing. On the spending side, we include changes to Medicaid spending consistent with the Energy and Commerce Committee’s reconciliation instructions, and changes to the Supplemental Nutrition Assistance Program (SNAP) consistent with the Agriculture Committee’s instructions.

The results of this exercise are shown in the tables and figures below, which display changes to after-tax-and-transfer income in calendar year 2027. Reporting suggests that the precise start year of changes to Medicaid and SNAP are a live topic of discussion among members of the House Republic conference. For illustrative purposes, we assume for the purposes of our analysis that these changes are spread evenly over the nine remaining years of the budget window and show results for 2027.

We present two sets of results: one set that assumes that states do not offset Federal cuts to Medicaid and SNAP spending with increases in state funding for those programs, and one set that assumes that they offset half of those cuts on average, consistent with the Congressional Budget Office’s (CBO’s) practice.

The overall effect of these policy changes would be regressive, shifting after-tax-and-transfer resources away from tax units (members of a household filing a tax return together) at the bottom of the distribution towards those at the top. Tax units at the bottom of the income distribution would see a reduction in after-tax-and-transfer income of 4% ($800), those in the middle of the distribution would see an increase of 2% ($1,140), and those in the top five percent of tax units would see an increase of more than 4% ($24,000). Nearly four-fifths of the net fiscal benefit would accrue to the top quintile. Even if states were to partially offset cuts to SNAP and Medicaid, the bottom quintile would see a reduction in after-tax-and-transfer income of 1.7% ($345).

For Medicaid and SNAP, we assume that total cuts to Federal spending on the programs are equal to the amounts specified by their respective committees. We assume that cuts are spread equally across the remaining years of the budget window, and that spending on each subcomponent of the programs—in particular, benefits for recipients—is reduced proportional to its share of program spending in the most recent baseline projections from CBO. The Budget Lab will update these assumptions as more details on these provisions emerge.