How Does OBBBA Affect the Time it Takes to File a Tax Return?

Key Takeaways

-

The TCJA extension piece of OBBBA means that taxpayers will continue to benefit from the time-savings in the TCJA, but the new ‘No Tax’ provisions increase the time it takes to file taxes.

-

Overall, due to the increased complexity from the new provisions, the average time burden does not substantially change under OBBBA despite the time savings from the TCJA extension.

-

For lower-income tax filers, time to file will actually increase under OBBBA.

-

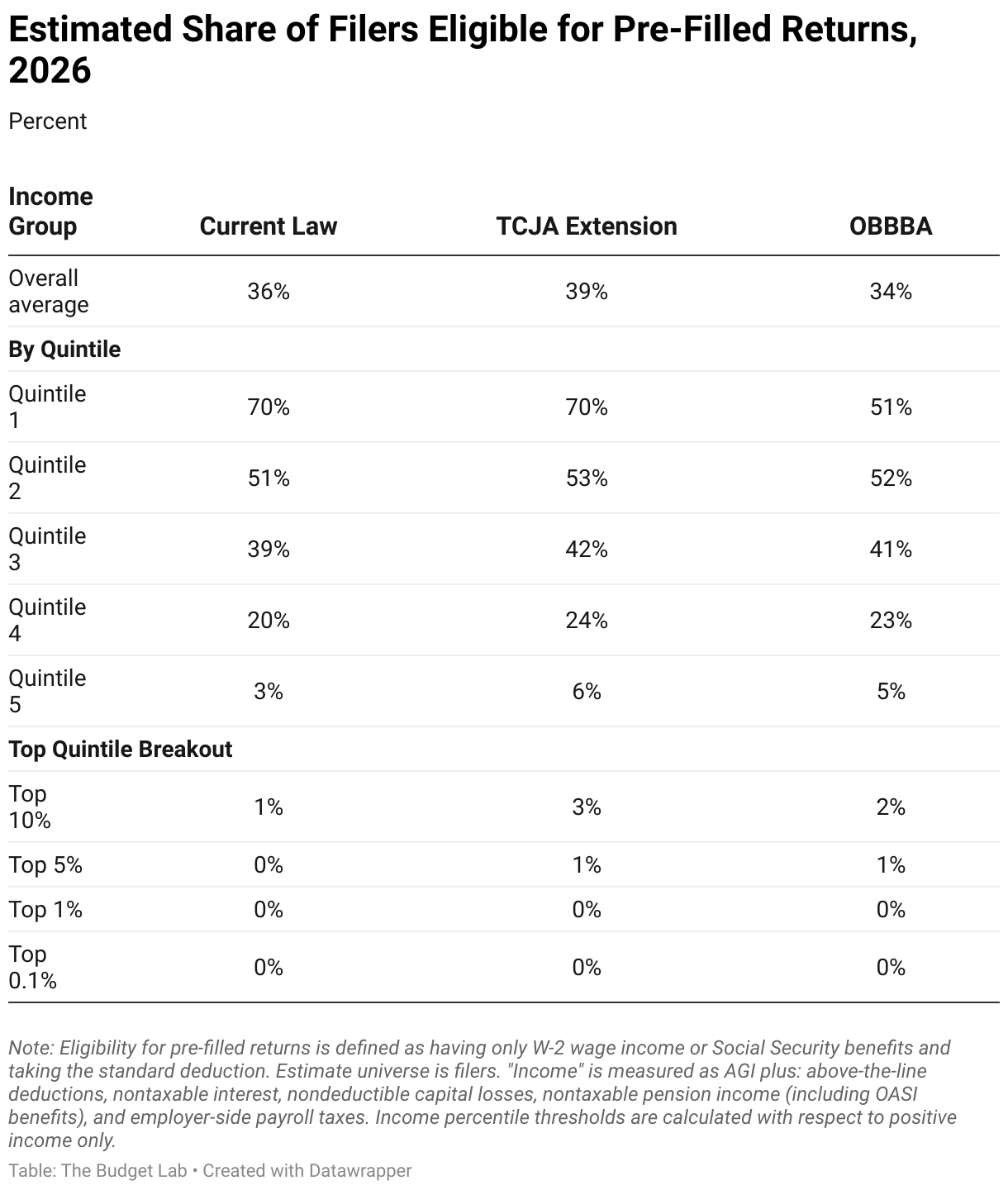

The increase in complexity in the tax code means that a smaller share of tax filers could have “pre-filled” returns under OBBBA than if TCJA had simply expired.

Introduction

Filing taxes is an annual burden for millions of individuals and businesses, encompassing both tangible costs and intangible stress factors that extend far beyond simply writing a check to the government. The complexity of the tax code, with deductions, credits, exemptions, and constantly evolving regulations, forces taxpayers to invest substantial time and energy into understanding their obligations or alternatively pay professionals to navigate the system for them. The average American spends 13 hours each year gathering documents, organizing receipts, learning about tax law changes, and either preparing their own returns or working with accountants and tax preparers.1 This time commitment represents an opportunity cost, as those hours could otherwise be spent on productive work, family time, or leisure activities.

The financial burden extends beyond the taxes owed to include preparation costs, whether through tax software, professional fees, or the hidden costs of record-keeping throughout the year. Small business owners face particularly acute challenges, often requiring sophisticated accounting systems and professional guidance to comply with employment taxes, quarterly payments, and complex business deduction rules. The system's complexity also creates inequities, as those with simpler financial situations may struggle with the same forms and requirements designed for complex business arrangements, while wealthy individuals and corporations can afford specialized advice to minimize their tax burdens legally. This administrative burden arguably represents a form of hidden tax itself, as the collective time and resources devoted to tax compliance could otherwise contribute to economic productivity and personal well-being.

As part of our analysis of the One Big Beautiful Bill Act (OBBBA), we considered how the tax changes affect the time burden of filing taxes. We explored how extending the Tax Cuts and Jobs Act (TCJA) expiring provisions in this piece. In this piece, we consider how the tax provisions enacted as part of the bill change the burden of filing taxes. The provisions that affect the filing burden are each of the “No Tax On” provisions as well as the change in the State and Local Tax (SALT) deduction.

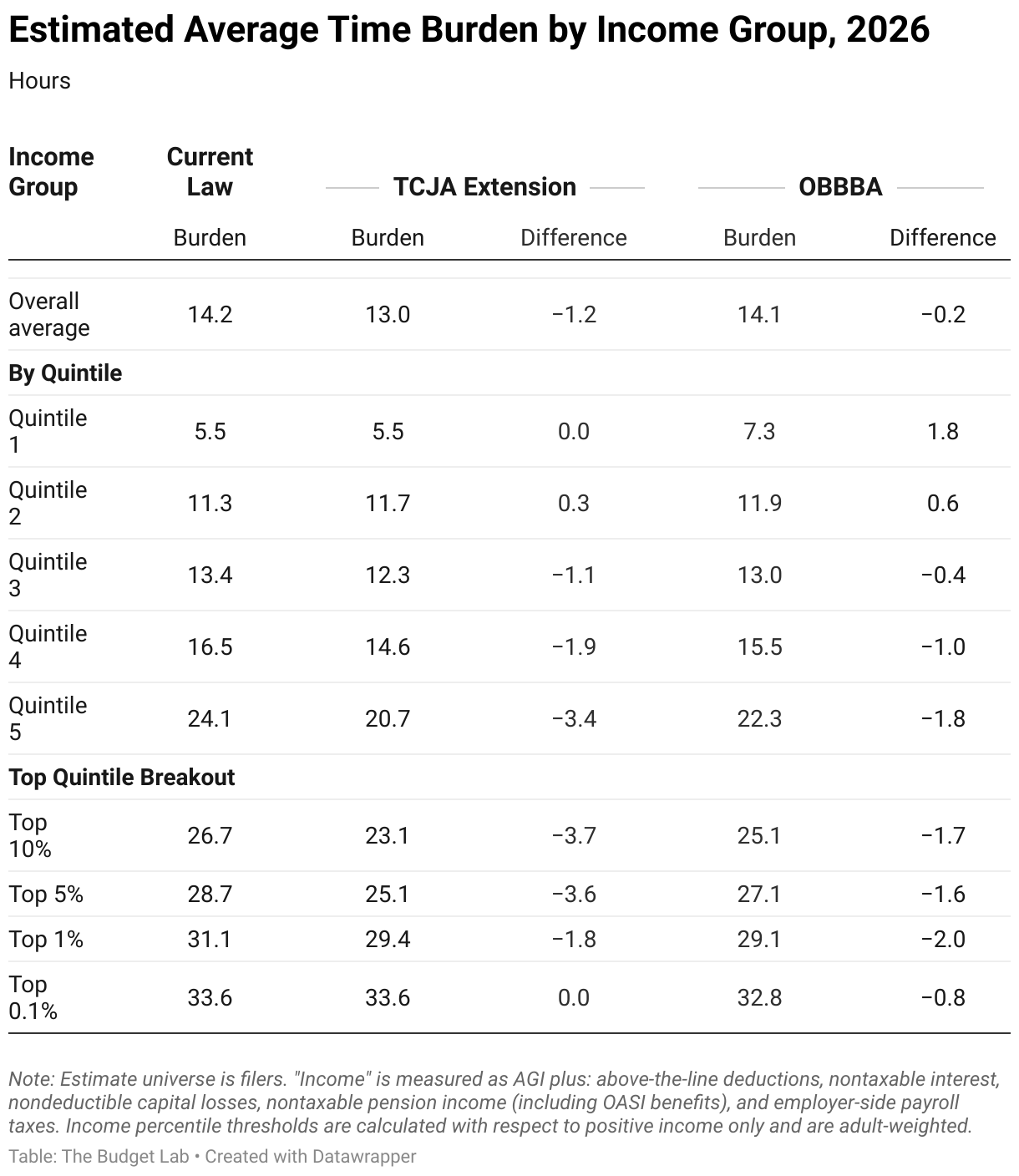

- Under the TCJA expiration scenario, the overall average time burden is 14.2 hours. Simple extension of TCJA decreases the average time burden by roughly 72 minutes.

- Only the second income quintile sees an increase in time burden under simple TCJA extension. It is due largely to the utilization of the Qualified Business Income deduction by this income group.

- The decrease in time burden in other income groups is largely due to the increase in the standard deduction which reduces the number of itemizers.

- With the passage of the OBBBA, we forecast the average time burden ticks down slightly relative to a current law scenario but is a substantial increase relative to simple TCJA extension.

- The “No Tax On” provisions add time burden. The lowest quintile sees an almost 2 hour increase in time burden while the second lowest quintile sees roughly a 36 minute increase. The estimates highlight the distribution of benefits from the “No Tax On” provisions. These provisions are aimed at lower income groups but there is cost to those benefits- additional time burden.

- The third through fifth income quintiles see a drop in time burden from the TCJA expiration scenario but see an increase in time burden as compared to the simple TCJA extension. This difference is due to the higher SALT cap. A higher SALT cap increases the number of itemizers and therefore, the time burden.

Number of Potential Pre-Filled Returns

For filers who only receive income subject information reporting, the government already has the information needed to fill out their tax returns. These are filers who do not file any extra schedules, do not need to comply with complicated rules, and are not required to engage in extensive recordkeeping – they receive only W-2 wages and/or Social Security earnings, both provided on information returns (W-2 and SSA-1099, respectively).This makes this set of tax filers ideal candidates for “pre-filled” returns, with minimal burden on the taxpayer. The IRS is currently piloting a program called Direct File that allows residents in 12 states with similarly relatively simple returns to file directly with the IRS and is a step towards pre-filled returns. However, there is a provision in the OBBBA to explore ending this program.

The table below shows the share of simple filers in each income group. These simple filers are largely unaffected by the policy changes in TCJA extension except for the change in the standard deduction and is clear in Table 2 with minimal change in percentage of simple filers. However, there are significant changes due to the “No Tax On” provisions in the OBBBA. In fact, a smaller share of filers could have “pre-filled returns” under OBBBA than under current law.

Appendix

No Tax Provisions

The "No Tax on" provisions, enacted as part of the One Big Beautiful Bill Act in July 2025, introduce a significant new layer of administrative complexity to tax filing. The three provisions “No Tax On Tips,” “No Tax on Overtime,” and “No Tax on Auto Loan Interest” each require extra filing that adds to the burden of filing taxes. Consider each in turn.

Tips

The no tax on tips provision allows eligible workers to deduct up to $25,000 in reported tips from their federal taxable income for tax years 2025-2028. The deduction phases out for workers earning over $150,000 annually ($300,000 for joint filers). Employees can only deduct tips that are properly reported to employers and reflected on Form W-2 statements. Workers must implement record-keeping to track their tips so they can fully account for their income when filing their taxes. The deduction applies only to "qualified tips" that are voluntary and customer-determined, meaning workers must distinguish between legitimate tips and mandatory service charges (like a certain percentage tip for parties over 5). Additionally, workers still must report all tips to their employers if they total $20 or more in a single month and those earnings remain subject to Social Security and Medicare payroll taxes. In our model, filing for this deduction adds 34 minutes to filing burden.

Overtime

The "No Tax on Overtime" provision allows employees to exclude qualified overtime compensation from gross income for federal income tax purposes through an above-the-line deduction, capped at $12,500 for single filers and $25,000 for joint filers, with the same phase-out thresholds as the tips provision. The filing burden begins with the definition of qualifying overtime compensation. Qualified overtime compensation is defined by the Fair Labor Standards Act (FLSA), meaning employers and employees must understand both federal labor laws and federal tax laws to determine what constitutes eligible overtime. This creates immediate complications because many categories of employees are exempt from overtime under federal laws, including executive, administrative, professional, and certain sales and computer-related occupations. This adds complexity to what appears to a simple tax benefit.

For workers, the filing burden involves documenting and claiming the overtime deduction while navigating the same income limitations as the tips provision. The deduction phases out by $100 for each $1,000 by which the taxpayer's modified adjusted gross income exceeds $150,000 ($300,000 for joint returns), requiring careful income calculations to determine benefit amounts. Workers must also ensure their overtime compensation is properly reported on Form W-2 to claim the deduction, making them dependent on employer compliance with new reporting requirements. In our model, filing for this deduction also adds 34 minutes to the filing burden.

While not in our model, the filing burden extends beyond individual tax returns to broader payroll administration challenges for both the tips and overtime provision. Employers must absorb additional work distinguishing between regular wages, tips, overtime, and bonuses for tax reporting purposes. Currently, overtime pay is not identified separately from regular wages on the Form W-2, so employers will be required to report overtime wages separately on Form W-2. Payroll systems likely already track overtime wages for non-tax purposes, but new software mapping is required to capture overtime wages for tax reporting requirements. This suggests that many employers may face significant costs and operational disruptions to comply with the new reporting requirements, particularly smaller businesses that lack sophisticated payroll infrastructure. The tax treatment creates additional filing complexity because, like tips, overtime wages remain subject to multiple forms of taxation despite the income tax deduction. Overtime wages and tips are still subject to Social Security and Medicare taxes, and employers must continue withholding federal income tax, state and local taxes where applicable. This dual treatment means payroll systems must accommodate income that is simultaneously taxable for some purposes and deductible for others, requiring sophisticated accounting capabilities.

The regulatory uncertainty surrounding implementation adds another layer of complexity. For both the tips and overtime provisions, employers can "approximate" amounts using "reasonable methods" to be specified by the Treasury Secretary for 2025, but these methods remain undefined. For the tips provisions, The Treasury Department and IRS must still write regulations defining which specific jobs qualify for the deduction, creating ongoing uncertainty for both workers and employers about eligibility. There is also a transition rule for 2025 under which information reported may approximate a separate accounting of qualified overtime amounts by any reasonable method creating temporary flexibility that may lead to inconsistent treatment across employers and potential compliance issues. The retroactive effective date to January 1, 2025, compounds this challenge by creating transition period administrative complexities without adequate preparation time.

Auto Interest

The "No Tax on Auto Loan Interest" provision allows taxpayers to deduct up to $10,000 annually in auto loan interest, effective for vehicle purchases from 2025 through 2028. However, it introduces multiple verification requirements and documentation burdens. The car's vehicle identification number (VIN) must be reported on tax returns in order to qualify for the deduction to link loan payments to specific vehicles. The vehicle qualification requirements create ongoing documentation challenges throughout the loan term since the deduction only applies to new vehicles for personal use, and the vehicle must have had its "final assembly" occur in the United States. While the bill does not provide an exhaustive definition of what "final assembly" means, consumers can likely verify their vehicle's eligibility through dealer-provided documentation or certifications, as dealers are likely to advertise qualifying vehicles.

The income-based phase-out system adds complexity to the filing process. The deduction is reduced by $200 for every $1,000 that modified adjusted gross income (MAGI) exceeds $100,000 for single filers or $200,000 for married couples filing jointly. Taxpayers cannot deduct any loan interest at all if their modified adjusted gross income exceeds $149,000 for single filers or $249,000 for joint filers. This requires taxpayers to calculate their MAGI and apply the phase-out formulas to determine their eligible deduction amount.

The loan tracking requirements also creates a substantial record-keeping burden for taxpayers. Only first lien loans qualify, meaning leases do not qualify for the deduction. Taxpayers must maintain detailed loan documentation showing interest payments separately from principal payments throughout the loan term. Interest payments on loans are front-loaded, while principal payments grow on the back end, meaning the deduction will decline after the initial year, requiring taxpayers to track changing benefit amounts. Car buyers will be able to itemize their auto loan interest even if they take the standard deduction, which differs from the mortgage interest deduction (MID) that is only available to taxpayers who itemize. However, this benefit requires taxpayers to understand the interaction between this "above-the-line" deduction and their other tax planning strategies. In our model, this provision adds 86 minutes to the total time of filing taxes.

Like the other “no tax” provisions, the regulatory implementation adds uncertainty to the filing burden. The IRS is expected to create a resource listing qualifying vehicles and models, similar to existing resources for electric vehicle tax credits, to clarify which vehicles meet the final assembly requirement. Until these resources are available, taxpayers must rely on potentially incomplete information to determine eligibility, creating risk of incorrect claims and potential audit exposure.

The administrative burden extends to lenders and dealers who must provide appropriate documentation to support taxpayer claims. Lenders must now file paperwork for loans with at least $600 in interest, adding administrative requirements. However, this requirement may not provide all the documentation taxpayers need to substantiate their claims, potentially requiring additional record-gathering efforts.

As with the other “no tax” provisions, the temporary nature of the provision creates long-term filing complexity. The deduction will expire in 2028. This requires taxpayers to understand the sunset provisions and plan their vehicle purchases and loan structures accordingly, while maintaining records that support claims during the limited eligibility period. The practical impact on most taxpayers is more limited than the maximum benefit suggests. The average new car buyer would not be able to deduct the full $10,000. In order to receive the full benefit, taxpayers would need a loan of approximately $112,000 at a rate of about 7%. The filing burden is further complicated by limitations that may exclude eligible taxpayers from receiving meaningful benefits. Lower-income filers who might not have enough income tax liability may not benefit from the deduction. This means taxpayers must evaluate whether their tax liability is sufficient to make the administrative burden worthwhile, adding another layer of complexity to filing taxes.

Senior

The additional standard deduction for seniors also creates a new administrative layer in tax filing that introduces several compliance complexities and verification requirements for taxpayers age 65 and older. This temporary provision allows eligible seniors to claim an additional $6,000 deduction ($12,000 for married couples where both spouses qualify), but requires age verification, income calculations, and phase-out determinations. To qualify for the additional deduction, a taxpayer must attain age 65 on or before the last day of the taxable year. For married couples filing jointly, each spouse's age must be verified separately to determine whether they qualify for $6,000 or $12,000 in total deductions, requiring coordinated record-keeping between spouses. The deduction phases out at a rate of 6% of the amount of the household's Modified Adjusted Gross Income (MAGI) over $75,000 for single filers or $150,000 for joint filers. Households with over $175,000 for single filers or $250,000 for joint filers will be fully phased out of the additional senior deduction. This requires taxpayers to accurately calculate their MAGI, apply the phase-out formula, and determine their eligible deduction amount. The MAGI calculation requires seniors to identify and add back specific income items that were previously excluded, requiring detailed knowledge of tax rules or professional assistance to ensure accurate calculations. In our model, this provision adds 19 minutes to the overall time burden.

State and Local Tax Deduction

One provision in the TCJA that reduced the time burden from many filers is the State and Local Tax (SALT) Deduction cap of $10,000. The cap reduced the number of itemizers and therefore, the overall burden of filing taxes. In the OBBBA, the SALT cap was increased to $40,000 with the cap phasing down to $10,000 at $500,000 of income. This increase in the cap increases the number of itemizers and therefore, the time burden.