State of U.S. Tariffs: April 8, 2026

Key Takeaways

-

The Budget Lab (TBL) estimates the effects of all US tariffs and foreign retaliation implemented through April 8, 2026, including the newly announced pharmaceutical tariffs and changes to metal tariffs under Section 232. Under our baseline case, the Section 122 tariffs expire after 150 days, but this report also presents estimates for a scenario where they are made permanent.

-

Current Tariff Rate: Today, the pre-substitution average effective tariff rate stands at 11.8%, the highest since the early 1940s (excluding 2025). Later this year, after the Section 122 tariffs expire and the pharmaceutical tariffs go into effect, this rate will be 9.7%. (If the Section 122 tariffs are instead made permanent, the rate would be 12.2%.)

-

Overall Price Level & Distributional Effects: TBL assumes the Federal Reserve “looks through” the tariffs and allows prices to rise such that the tax burden is felt through higher prices for consumers rather than lower nominal incomes for workers and firms. If Section 122 tariffs expire as scheduled, the ultimate price level impact will be between 0.5% and 0.7%, representing a loss of between about $760 and $940 for the average household. (If they are instead made permanent, the price impact would be between 0.9% and 1.1% and the household loss figures would be between $1,200 and $1,500.)

-

Macro Effects: On a year-over-year basis, the 2026 economy benefits from lower tariff rates this year compared to last year. In the long run, the US economy is persistently 0.1% smaller, the equivalent of about $30 billion annually in 2025 dollars. (If Section 122 is extended, the long-run reduction in output grows by about two-thirds.)

-

Long-Run Sectoral GDP & Employment Effects: In the long run, tariffs present a trade-off. US manufacturing output expands by 1.1%, but these gains are more than crowded out by other sectors: construction output contracts by 2.5% and mining declines by 1.0%. (These effects are directionally similar and larger if Section 122 is extended.)

-

Fiscal Effects: Assuming Section 122 tariffs expire in 150 days, the administration’s tariffs will raise about $1.3 trillion over 2026–35, though slower economic growth reduces revenues and brings the net dynamic revenue to $1.2 trillion. (If they are instead made permanent, these figures would be $1.9 trillion and $1.7 trillion.)

Changes Since the Last Report

This report reflects several changes, the code behind which is available to view in our public GitHub repository, since our update published the morning of April 2. The first two are policy changes announced later on April 2:

- Changes to metal tariffs. Prior to this announcement, Section 232 tariffs on metals were structured as a single-rate system where imports were subject to a 50% tariff on the respective metal content of steel, aluminum, and copper products. The new policy creates a multi-rate system based on metal content (where certain country-specific rates apply), effective April 6, 2026:

- High-metal content products face a 50% rate.

- Most derivative products face a 25% rate (on the full import value, not just the metal content value).

- Other derivative products face a minimum 15% overall tariff rate.

- Products with less than 15% metal content by weight are exempt (though may be subject to other tariffs).

- New pharmaceutical tariffs. This announcement introduces a new 100% Section 232 tariff on most patented pharmaceuticals and related products. Generic drugs and “orphan” drugs are exempt, and certain countries face lower rates based on trade deals. Products from companies who make certain onshoring agreements with the administration are eligible for a lower rate; if those companies also enter pricing agreements, their products are exempt entirely. Seventeen drug manufacturers are named explicitly in the announcement as having pre-existing onshoring agreements. This regime goes into effect on September 29, 2026.

Both regimes include scheduled future changes that we do not model. (The metal tariff’s 15% floor is temporary, expiring December 31, 2027; elements of the company-specific preferential treatment framework for the pharmaceutical tariffs expire in 2029 and 2030.) Because we use a “current policy” modeling framework, where we evaluate the effects of policy as enacted through a near-term horizon, these longer-term scheduled changes are not reflected in our estimates.

Since the last report, we also made several minor changes to our effective tariff rate model which affected the estimated overall average effective tariff rate by less than 0.1 percentage point.

Results

Average effective tariff rate

The distinction between pre-substitution metrics (before consumers and businesses shift purchases in response to the tariffs) and post-substitution (after they shift) is a crucial one. One metric where the difference is meaningful is the average effective tariff rate.

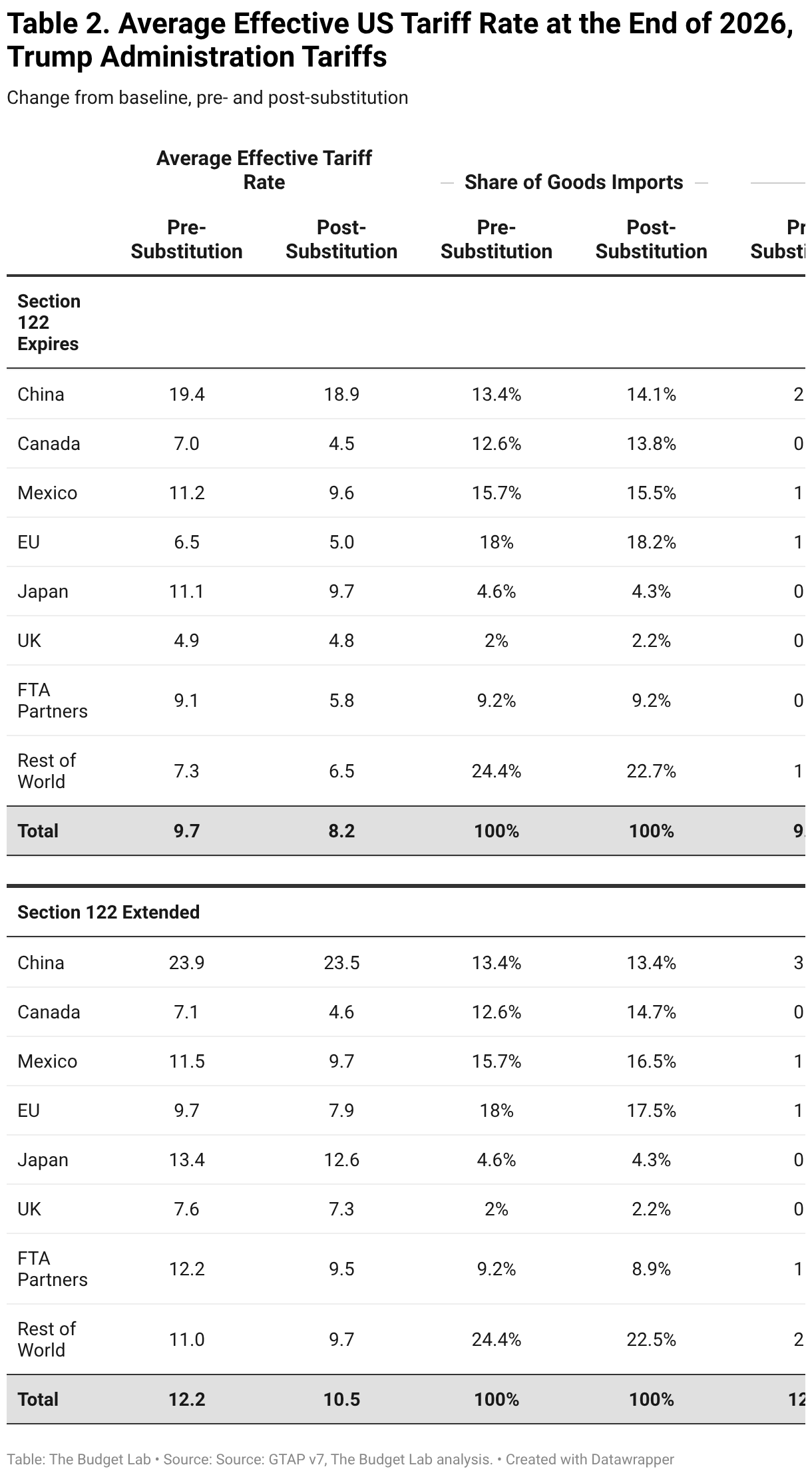

Measured pre-substitution—assuming there are no shifts in the import shares of different countries and products—the tariff policy in effect as of April 6 brings the US average effective tariff rate to approximately 11.8%, the highest since the early 1940s (excluding last year's tariff rates). A pre-substitution approach is a good measure of welfare, since it reflects the full cost faced by consumers and firms before they start making difficult spending choices. After the Section 122 tariffs expire in July and the Section 232 pharmaceutical tariffs take effect in September, the rate will settle at 9.7%. If the Section 122 tariffs are instead made permanent, the end-of-2026 rate would be 12.2%.

Post-substitution—after imports shift in response to the tariffs—the end-of-2026 effective tariff rate will be 8.2% assuming Section 122 expires, or 10.5% if extended.

Figure 1 shows the Trump administration’s tariffs in the long-run historical context, and Figure 2 plots the daily pre-substitution ETR throughout 2025 and 2026. Table 2 shows a country-level breakdown for pre- and post-substitution rates for the end of 2026.

Average Aggregate Price Impact

The current tariff regime implies an increase in consumer prices of 1.1% in the short run, assuming full passthrough of tariffs to consumers and assuming that the Section 122 tariffs are extended. If these tariffs expire as scheduled, this figure is about 0.7%. These pre-substitution numbers capture consumer welfare effects and are the equivalent of a loss of income of about $1,500 (extension) or $940 (expiration) per household on average in 2025 dollars.

Under expiration of the Section 122 tariffs, the post-substitution price increase settles at 0.5%, a $760 loss per household. (If extended, these figures are roughly 0.9% and $1,200.)

US Macroeconomic Effects

TBL estimates that, all else equal, the current tariff regime has reduced GDP and increased unemployment slightly. While the level of output in 2026 is lower than it would have otherwise been if the pre-2025 tariff regime had been maintained, tariffs are increasing the growth rate of output in 2026 as the economy recovers somewhat from the large shock in 2025. The level of real GDP remains persistently 0.11% to 0.18% smaller in the long run, depending on the duration of Section 122 tariffs. Our modeling suggests any economic boost associated with refunds of IEEPA tariffs to businesses will be small.

Long-Run US Sectoral Output & Employment Effects

Tariffs shrink the overall size of the US economy in the long run, but beneath aggregate GDP, they also drive reallocation across US sectors. Long-run output in the manufacturing sector expands slightly, with durable manufacturing seeing the largest gains within the manufacturing category. But this expansion in manufacturing more than crowds out the rest of the economy: construction, mining & extraction, and agriculture contract slightly. These patterns are similar regardless of whether Section 122 tariffs expire or are extended.

Global Long-Run Real GDP Effects

Long-run global GDP is slightly lower due to tariff policy. Canada, China and Mexico see the largest negative hits to output, while European and other free trade agreement partners see slight boosts to output. These directional effects are similar regardless of whether Section 122 tariffs expire or are extended in July.

Fiscal Impact

The current tariff regime, assuming that Section 122 tariffs expire, would raise about $1.3 trillion over ten years, conventionally scored. Given the negative output effects of the tariffs, these new revenues will be partially offset by reductions in tax revenue as a result of lower growth. TBL estimates that these effects would total about $10 billion over the decade, bringing net dynamic revenue to about $1.2 trillion.

If instead the Section 122 tariffs are extended, revenue would be meaningfully higher: conventional revenue would be $1.8 trillion over the decade and the dynamic score would be roughly $1.7 trillion.

Distributional Impact

One way to measure the distributional burden of tariffs is to look at the relationship between consumption, which gets more expensive under tariffs, and income for a given year. Under this view, tariffs are a regressive tax because lower-income households spend a larger fraction of their income than higher-income households do on average.

TBL finds that the burden, expressed as a share of post-tax-and-transfer income, on the first decile is about three times that of the top decile (1.1% versus 0.4% if Section 122 tariffs expire, and 1.9% versus 0.6% if extended). The average annual costs to households in the bottom and top deciles are about $517 and $2,175 respectively in 2025 dollars—figures that assume Section 122 tariffs expire. If instead Section 122 is made permanent, these annual household burdens would be about $813 and $3,424.

Consumer Prices by Spending Category

Tariffs affect different goods and services differently. Figure 7 shows the estimated price impact by spending category. Assuming Section 122 tariffs expire as scheduled, the categories most affected are goods products like motor vehicles, clothing, and furnishings. Services, which account for the majority of consumer spending, face only indirect price pressures through tariffs and thus see much smaller price effects. If Section 122 tariffs are extended, the price effects are directionally similar but larger, and clothing would rank above motor vehicles as the hardest-hit category.

Appendix

The new pharmaceutical tariffs, which include carve-outs for specific companies and product types for which government data is unavailable, necessitate additional modeling assumptions beyond what is normally required for our analysis. We begin by calculating the 100% total duty floor on patented pharmaceuticals using the product list in the proclamation and modeling each of the country-specific trade-deal rates. We then reduce the effective rate by two country-level adjustment factors. First, a generic share captures the fraction of covered imports that are generic rather than patented and thus exempt: we assume 20% for most countries, and 95% for China and India where generic manufacturing dominates. These numbers generate an overall trade-weighted average generic share of about 23%. Second, an exempt company share captures the fraction of patented imports from the 17 named manufacturers with onshoring agreements, whose products we assume are fully exempt: we assume 40% globally, 75% for the EU, UK, and Japan, and 95% for Ireland, Switzerland, and Belguim. Both adjustment factors are judgmental assumptions based not on hard data but instead on our qualitative reading about trade patterns and company activities.