The Financial Cost of the Senate Budget Bill’s Tax Provisions

Key Takeaways

-

The tax provisions in the budget bill introduced by the Senate Finance Committee on June 16 would add $4.1 trillion to the debt over the 2025-2034 window (1.15% of GDP over this time period) and $19.4 trillion from 2025-2055 (1.14% of GDP over this time period).

-

If the temporary tax provisions became permanent, the cost over the 2025-2034 window is $4.5 trillion (1.26% of GDP over the time period) and over the 2025-2055 window is $21.0 trillion (1.23% of GDP over the time period).

-

During the 2045-2055 window, the cost in additional interest (even assuming no increase in interest rates due to this bill) is over 87 percent of the direct cost of the bill as written, rising to around 90 percent if the temporary tax provisions became permanent.

-

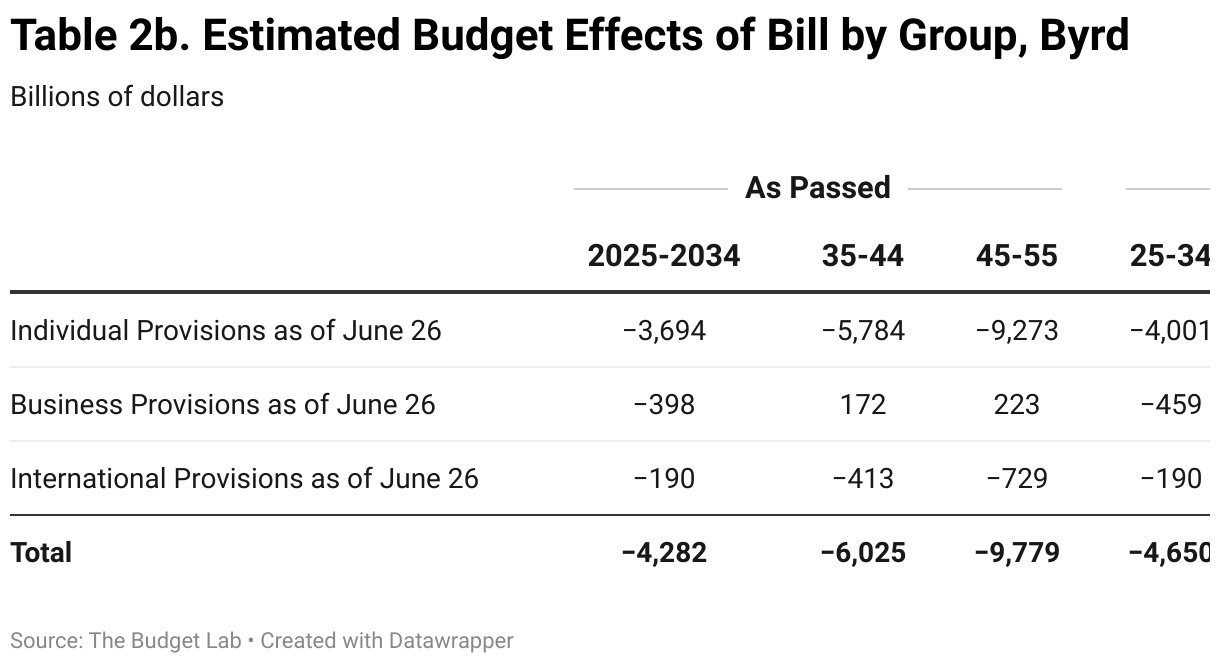

If the provisions judged to violate the Byrd Rule are removed, the cost over the 2025-2034 window increases to $4.3 trillion (1.19% of GDP over the time period) and $4.6 trillion (1.29% of GDP over the time period) if the temporary provisions are made permanent. The cost over the 2025-2055 window would increase to $20.1 trillion (1.18% of GDP) and $21.7 trillion (1.27% of GDP), respectively.

-

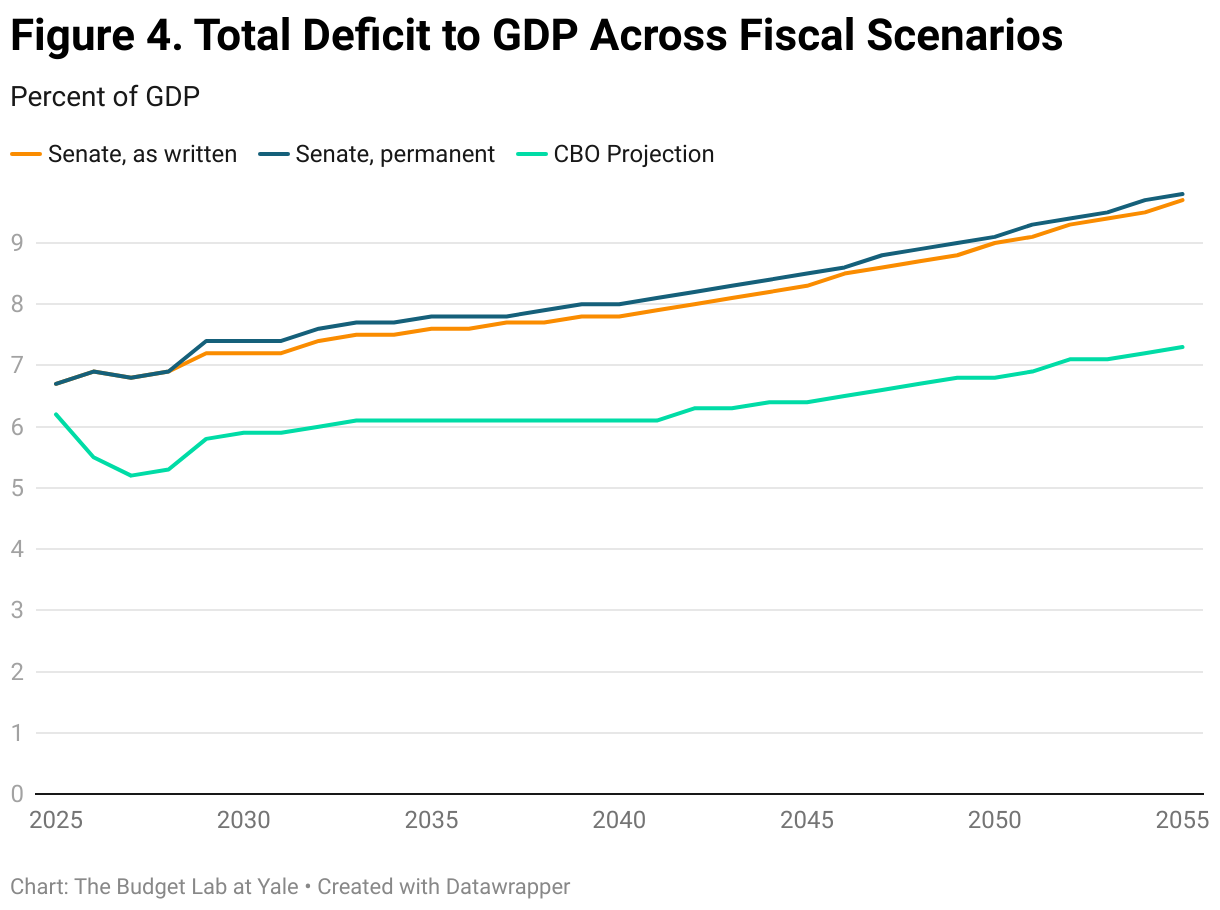

Under each scenario for the bill (Permanent and Temporary), the deficit level increases over the 2025-2055 window.

-

Our projection of the deficit depends on our forecast of future interest rates. All else being equal, higher debt and deficit levels will raise interest rates. This analysis does not include any increase in interest rates due to higher debt levels.

Note: this score has been updated to reflect information about stricken provisions of the bill as of June 27, 2025.

Summary

This report provides an analysis of the budget bill introduced in the Senate. The tax provisions of the bill primarily extend and enhance the tax provisions in the 2017 Tax Cuts and Jobs Acts (TCJA) that are set to expire at the end of 2025. As in the House version, the bill also includes versions of several policies put forth by the President during the presidential campaign.

Note: this analysis provides a conventional score for these proposals. In this analysis, we do not look at the macroeconomic implications of this proposal. For distributional analysis, please see this analysis. We thus do not account for any additional growth (or slowing of growth) that may emerge in the short or long run from passing this bill, nor do we analyze the impact of the increased debt burden on interest rates.

The provisions presented here are designed to fit within the $4.5 trillion allowance set by the 2025 budget resolution. As such, some are temporary to lower the cost of the bill such as the ‘no tax on’ provisions, the extra standard deduction for seniors, and special depreciation for qualified production property. The Joint Committee on Taxation (JCT) presented revenue effects of the bill here. However, these estimates are presented relative to a current policy baseline which assumes a costless extension of the TCJA. We present revenue effects relative to a current law baseline that reflects the true cost of the bill.

- We estimate that the cost of the bill’s tax provisions, relative to a current law baseline, over the 2025-2034 window is $4.1 trillion and over the 2025-2055 window is $19.4 trillion (1.14% of GDP).

- If the Byrd violations hold, the cost over the 2025-2034 window is $4.3 trillion and over the 2025-2055 window is $20.1 trillion (1.18% of GDP).

- Using conventional scoring methods, the JCT estimates this section of the bill will cost $4.2 trillion.1

- If we assume that the temporary provisions become permanent (in other words, if we assume that lawmakers keep extending these provisions), the cost of the bill presented by the Senate Finance Committee over the 2025-2034 window is $4.5 trillion (1.26% of GDP over the time period) and over the 2025-2055 window is $21.0 trillion (1.18% of GDP).

- If the temporary provisions are made permanent and the Byrd violations hold, the cost over the 2025-2034 window is $4.6 trillion (1.29% of GDP over the time period) and over the 2025-2055 window is $21.7 trillion (1.27% of GDP).

Note that the bill as written adds to the deficit in the years outside of the ten-year budget window. This is not consistent with reconciliation rules unless the Senate either rewrites the bill or changes how bills are evaluated as being consistent with reconciliation rules. Furthermore, the parliamentarian has stricken portions of the bill forcing 60 votes rather than the simple majority allowed under reconciliation.

Analysis

The bill extends the tax provisions established in the TCJA. These provisions include lower individual rates, increased standard deduction, a larger Child Tax Credit (CTC), and a deduction for qualified business income (QBI). The bill also includes a number of new tax-related provisions first included in the House version such as “Trump accounts,” which would allow parents to give more money to their children tax-free; the removal of the excise tax on firearms. It also includes several of the President’s campaign promises such as “no tax on tips,” “no tax on overtime,” and a larger standard deduction for older Americans (presumably to act as a version of “no tax on Social Security”). Unlike the House bill, this proposal would not increase the cap on state and local tax deductions from its current-policy level of $10,000 (though reporting indicates this provision is likely to change in negotiations).

The bill also makes changes to the international tax system by harmonizing effective rates on Foreign-Derived Intangible Income (FDII), Global Intangible Low-taxed Income (GILTI), and the Base Erosion and Anti-Abuse Tax (BEAT) at 14%. It also permanently extends the Controlled Foreign Corporation look-through rule [954 (c)(6)] and imposes a retaliatory tax on foreign corporations if their home jurisdiction has adopted taxes deemed to be harmful similar to the House bill.

The bill also includes offsets by repealing or phasing out Inflation Reduction Act energy credits and restricting ACA subsidies though slightly less aggressively than the House version. These ACA subsidies were stricken by the Senate Parliamentarian. The unscored Medicaid provisions may also serve as an offset.

Conclusion

As this version of the reconciliation bill moves forward, it is important to note that while the deficit and the debt are not the only factors to consider in evaluating the bill, the effect on the fiscal picture of the nation would be substantial.

Appendix

Note: The graphs below present the effects of the bill as written and only the provisions in Senate Finance. They include provisions challenged under the Byrd rule.

Footnotes

- The JCT did not provide estimates for the Medicaid and Medicare provisions. In the interest of comparable numbers, we do not provide those estimates either. Budget Lab is planning to provide updated numbers that include the impacts on the spending side. That update will also include tariffs.