State of U.S. Tariffs: February 21, 2026

Key Takeaways

-

The Budget Lab (TBL) estimates the effects of all US tariffs and foreign retaliation implemented through February 20, 2026, including the new 15% Section 122 tariffs and the elimination of IEEPA-based tariffs. Under our baseline case, the Section 122 tariffs expire after 150 days, but this report also presents estimates for a scenario where they are made permanent.

-

Current Tariff Rate: Before the IEEPA tariffs were struck down, consumers faced an overall average effective tariff rate of 16%, the highest since 1936. Immediately following the IEEPA ruling, the rate fell to 9.1%. After the Section 122 tariffs were imposed, the rate rose to its current level of 13.7%. If those tariffs expire in 150 days, the rate will fall again to 9.1%.

-

Overall Price Level & Distributional Effects: TBL assumes the Federal Reserve “looks through” the tariffs and allows prices to rise such that the tax burden is felt through prices rather than nominal incomes. If Section 122 tariffs expire as scheduled, the ultimate price level impact will be between 0.5% and 0.6%, representing a loss of between $600 and 800 for the average household. (If they are instead made permanent, the price impact would be between 0.8% and 1.0% and the household loss figure would be $1,000 and $1,300).

-

Commodity Prices: The current tariff regime falls most heavily on metal products and electrical equipment, and motor vehicles. (If Section 122 is extended, apparel and related goods would also rank near the top of affected commodities.)

-

Macro Effects: Tariffs increase the unemployment rate by 0.3 percentage points by the end of 2026. In the long run, the US economy is persistently 0.1% smaller, the equivalent of about $30 billion annually in 2025 dollars. (If Section 122 is extended, the long-run hit is about twice as large.)

-

Long-Run Sectoral GDP & Employment Effects: In the long run, tariffs present a trade-off. US manufacturing output expands by 2%, but these gains are more than crowded out by other sectors: construction output contracts by 2.4% and mining declines by 1.1%. (These effects are directionally similar and larger if Section 122 is extended.)

-

Fiscal Effects: Assuming Section 122 tariffs expire in 150 days, the administration’s tariffs will raise about $1.3 trillion over 2026-35, though slower economic growth reduces revenues and brings the net dynamic revenue to $1.1 trillion. (If they are instead made permanent, these figures would be $2.2 trillion and $1.9 trillion.)

Changes Since the Last Report

This report was updated on February 21st to reflect three changes: the incorporation of the full list of exemptions listed in Annex II, the President’s announced rate increase from 10% to 15%, and a correction to the pre-SCOTUS effective tariff rate, which we now estimate to be 16.0% instead of 16.9%.

Since our January update, there have been several major tariff policy changes.

- All IEEPA-based tariffs, including both the “reciprocal” and “fentanyl” tariff regimes, were struck down by the Supreme Court on February 20, 2026. IEEPA was the main authority under which tariffs had been enacted through early 2026, accounting for most of the new revenue raised. The Budget Lab separately analyzed the impact of this ruling in a standalone report. In this report, we assume that IEEPA duties will be refunded over the next year.

- After the Supreme Court ruling, the President signed a proclamation imposing a flat 10% tariff on all imports under Section 122 of the Trade Act of 1974, a time-limited authority allowing duties for up to 150 days. Shortly after, the President announced the rate would be raised to 15%. As under IEEPA, goods subject to Section 232 actions are excluded and USMCA-compliant goods from Canada and Mexico remain exempt. The proclamation also recreates product-specific exemptions from the old IEEPA base by excluding critical minerals, energy products, agricultural goods, pharmaceuticals, electronics, and more.

We analyze two scenarios for tariff policy: one where Section 122 expires at the end of 150 days as scheduled, and another where it is extended.

Results

Average effective tariff rate

The distinction between pre-substitution metrics (before consumers and businesses shift purchases in response to the tariffs) and post-substitution (after they shift) is a crucial one. One metric where the difference is meaningful is the average effective tariff rate.

Measured pre-substitution—assuming there are no shifts in the import shares of different countries and products—current tariff policy, while the Section 122 tariffs are in effect, represents the equivalent of a 11.3 percentage point increase in the US average effective tariff rate. That calculation assumes that, for example, the share of imports from China remains at recent historical levels. A pre-substitution approach is a good measure of welfare, since it reflects the full cost faced by consumers before they start making difficult spending choices. This increase would bring the overall US average effective tariff rate to 13.7%, the highest since 1941, excluding last year’s tariff rates.

Post-substitution—after imports shift in response to the tariffs—the current tariffs generate a 9.8 percentage point increase in the US average effective tariff rate, which brings the overall US effective tariff rate to 12.2%.

If the Section 122 tariffs expire in 150 days as scheduled, the effective tariff rate will then be 9.1%, the highest since 1947 (8.0% post-substitution). Figure 1 shows this scenario.

Average aggregate price impact

The current tariff regime implies an increase in consumer prices of 0.6% in the short run, assuming full passthrough of tariffs to consumers and assuming that the Section 122 tariffs expire. If these tariffs are instead extended, this figure is about 1.0%. These pre-substitution numbers capture consumer welfare effects and are the equivalent of a loss of income of about $800 (expiration) or $1,300 (extension) per household on average in 2025 dollars.

Under expiration of the Section 122 tariffs, the post-substitution price increase settles at 0.5%, a $600 loss per household. (If extended, these figures are roughly 0.8% and $1,000.)

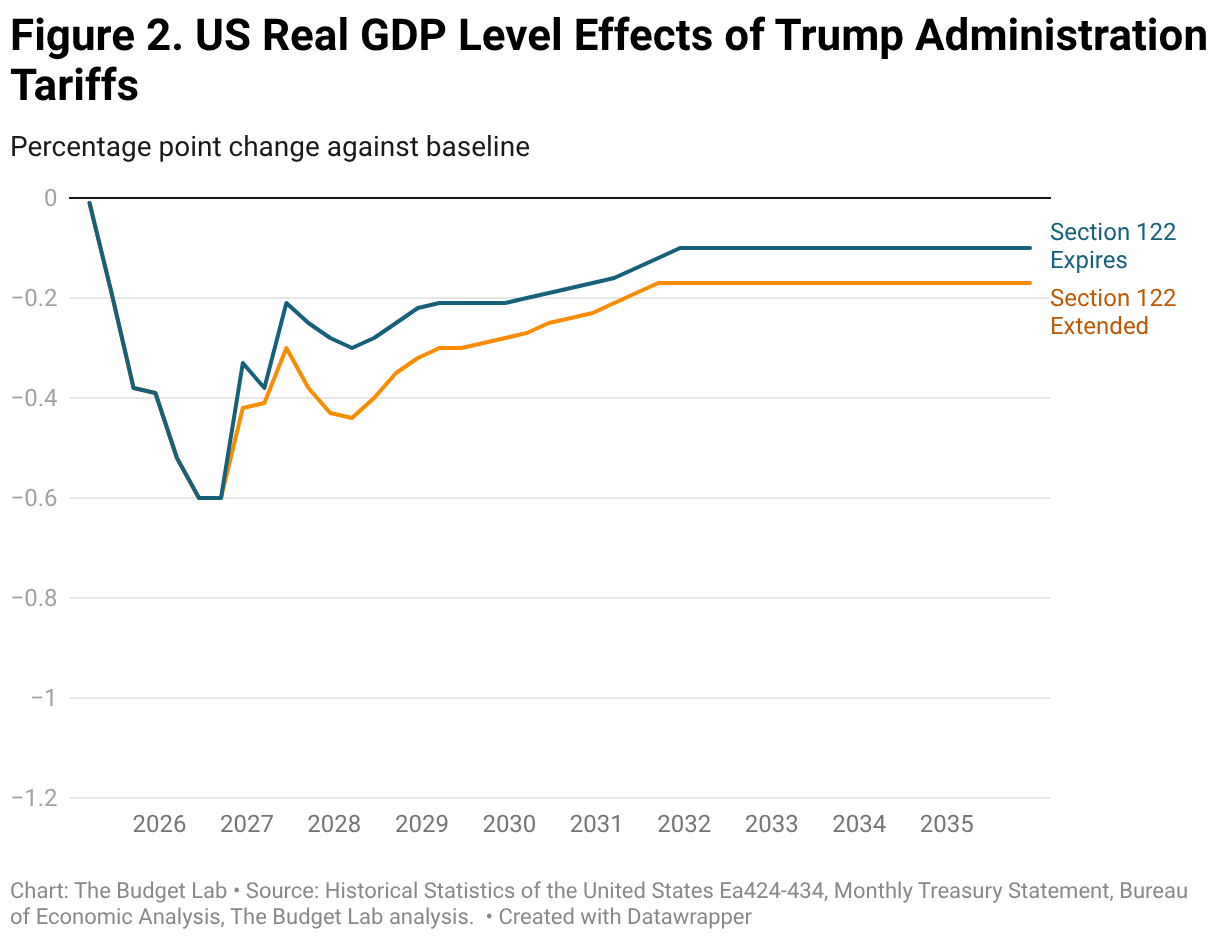

US real GDP & labor market effects

TBL projects that, all else equal, the current tariff regime will increase the unemployment rate by 0.3 percentage points by the end of 2026—if Section 122 tariffs expire (the negative hit to employment would be slightly higher if extended). We estimate that the temporary positive fiscal impulse from IEEPA refunds will approximately offset the negative growth impacts of the remaining tariffs for 2026, though there is substantial uncertainty over how and when refunds will be administered and thus the short-term effects of these refunds is uncertain. The level of real GDP remains persistently 0.1% to 0.2% smaller in the long run, depending on the duration of Section 122 tariffs.

Long-run US sectoral output & employment effects

Tariffs shrink the overall size of the US economy in the long run, but beneath aggregate GDP, they also drive reallocation across US sectors. Long-run output in the manufacturing sector expands slightly, with durable manufacturing seeing the largest gains within the manufacturing category. But this expansion in manufacturing more than crowds out the rest of the economy: construction, mining & extraction, and agriculture contract slightly. These patterns are similar regardless of whether Section 122 tariffs expire or are extended.

Global long-run real GDP effects

Long-run global GDP is slightly lower due to tariff policy. Canada, China and Mexico see the largest negative hits to output, while European and other free trade agreement partners see slight boosts to output. These directional effects are similar regardless of whether Section 122 tariffs expire or are extended in July.

Fiscal impact

The current tariff regime, assuming that Section 122 tariffs expire, would raise about $1.3 trillion over ten years, conventionally scored. The 150 days of Section 122 tariffs contribute about $30 billion to this sum. Given the negative output effects of the tariffs, these new revenues will be partially offset by reductions in tax revenue as a result of lower growth. TBL estimates that these effects would total about $180 billion over the decade, bringing net dynamic revenue to about $1.1 trillion.

If instead the Section 122 tariffs are extended, revenue would be meaningfully higher: conventional revenue would be nearly $2.2 trillion over the decade and the dynamic score would be roughly $1.9 trillion.

Distributional impact

One way to measure the distributional burden of tariffs is to look at the relationship between consumption, which gets more expensive under tariffs, and income for a given year. Under this view, tariffs are a regressive tax because lower-income households spend a larger fraction of their income than higher-income households do on average.

TBL finds that the burden, expressed as a share of post-tax-and-transfer income, on the first decile is about three times that of the top decile (1.1% versus 0.4% if Section 122 tariffs expire, and 1.9% versus 0.6% if extended). The average annual cost to households in the bottom and top deciles are about $400 and $1,800 respectively in 2025 dollars—figures that assume Section 122 tariffs expire and are thus not reflected in these numbers. If instead Section 122 is made permanent, these annual household burdens would be $700 and $3,000.

Commodity price effects

The charts below show how the overall price level increase from current tariffs would look across individual commodities, both in the short run and the in the long run after consumers shift purchasing patterns and firms reconfigure production decisions. Commodities hit hardest by the tariff regime include metals, electrical equipment, vehicles, and computers.

Apparel, leather products, and textiles would be largely unaffected by tariffs if the Section 122 tariffs expire, since the Section 232 tariff regime does not apply to them. But if extended, those products would see relatively large price increases.