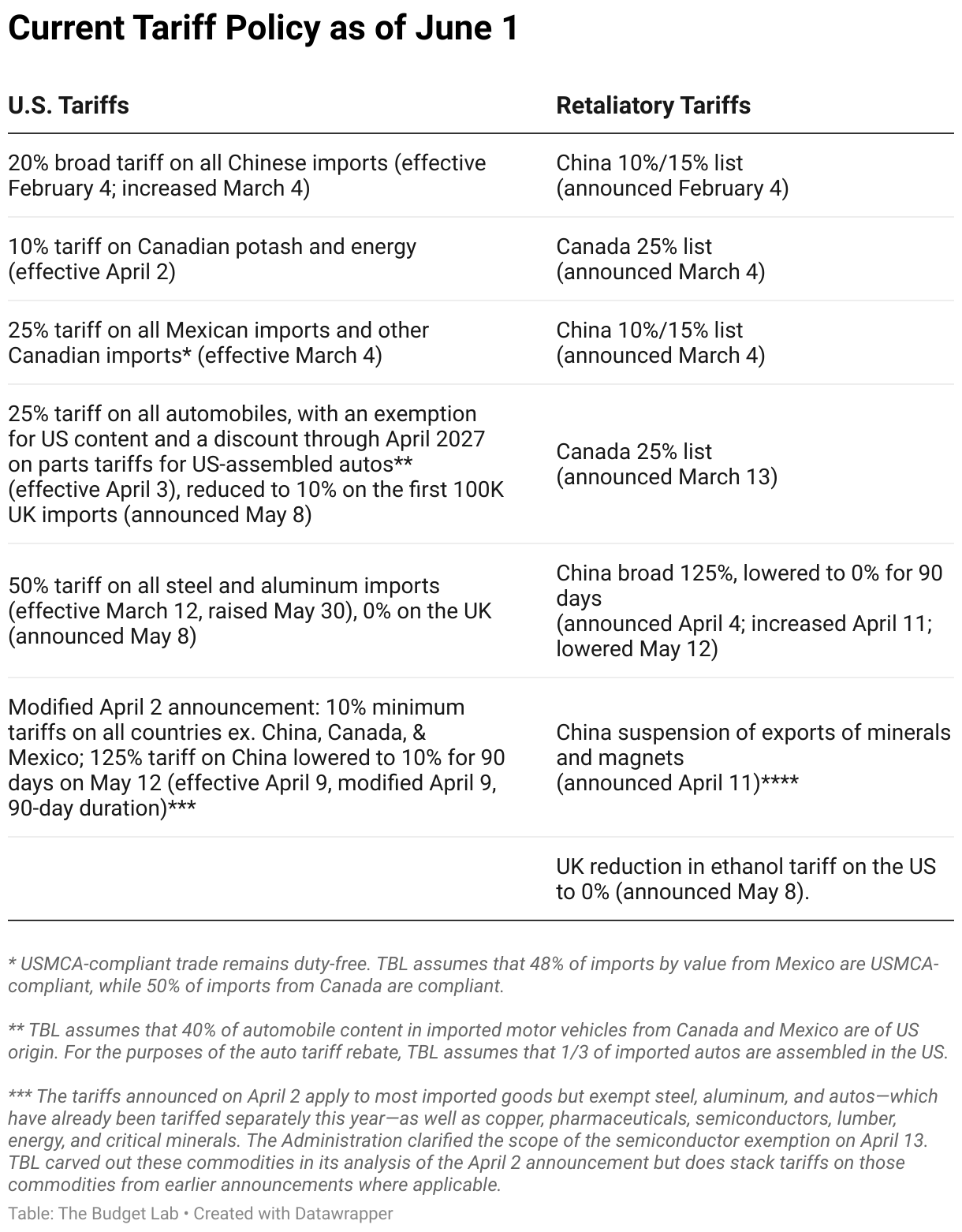

State of U.S. Tariffs: June 1, 2025

Key Takeaways

-

The Budget Lab (TBL) estimated the effects all US tariffs and foreign retaliation implemented in 2025 through June 1, including the effects of the higher 50% steel & aluminum tariffs announced May 30. TBL analyzed the June 1 tariff rates as if they stayed in effect in perpetuity.

-

Current Tariff Rate: Consumers face an overall average effective tariff rate of 15.6%, the highest since 1937. After consumption shifts, the average tariff rate will be 14.5%, also the highest since 1938.

-

Overall Price Level & Distributional Effects: The price level from all 2025 tariffs rises by 1.5% in the short-run, the equivalent of an average per household consumer loss of $2,500 in 2024$. Annual pre-substitution losses for households at the bottom of the income distribution are $1,100. The post-substitution price increase settles at 1.3%, a $2,100 loss per household.

-

Commodity Prices: The 2025 tariffs disproportionately affect clothing and textiles, with consumers facing 31% higher shoe prices and 28% higher apparel prices in the short-run. Shoes and apparel prices stay 17% and 15% higher in the long-run respectively.

-

Real GDP Effects: US real GDP growth is -0.5pp lower from all 2025 tariffs. In the long-run, the US economy is persistently -0.3% smaller respectively, the equivalent of $100 billion annually in 2024$.

-

Labor Market Effects: The unemployment rate rises 0.3 percentage point by the end of 2025, and payroll employment is 376,000 lower.

-

Long-Run Sectoral GDP & Employment Effects: In the long-run, tariffs present a trade-off. US manufacturing output expands by 1.3% but more than crowds out other sectors: construction output contracts by 2.0% and agriculture declines by 0.9%.

-

Fiscal Effects: All tariffs to date in 2025 raise $2.4 trillion over 2026-35, with $347 billion in negative dynamic revenue effects, bringing dynamic revenues to $2.0 trillion.

Changes since the Last Report

Since the May 29 report:

- On May 28, the U.S. Court of International Trade invalidated the Trump Administration’s tariffs imposed under authority from the International Emergency Economic Powers Act. That case is ongoing; however, on May 29, a federal appeals court temporarily agreed to preserve the IEEPA tariffs. That means that as of today, June 1, those tariffs remain in place, and they are reflected in our analysis.

- On May 30, the Trump Administration announced that the U.S. will double its current tariff rate on steel and aluminum impots from 25% to 50%.

- TBL incorporated updated data on USMCA-compliant trade shares with Canada. Whereas before, TBL assumed that 38% of trade with Canada was USMCA-compliant, March Census data showed that the share rose substantially to 50%.

TBL analyzes tariffs on a “real-time current policy” basis, where policy as it stands as of date certain is assumed to continue in perpetuity, even if framed as a temporary policy.

Results

The table below summarizes the effects of current tariffs in place as of June 1, assuming they stayed in force indefinitely.

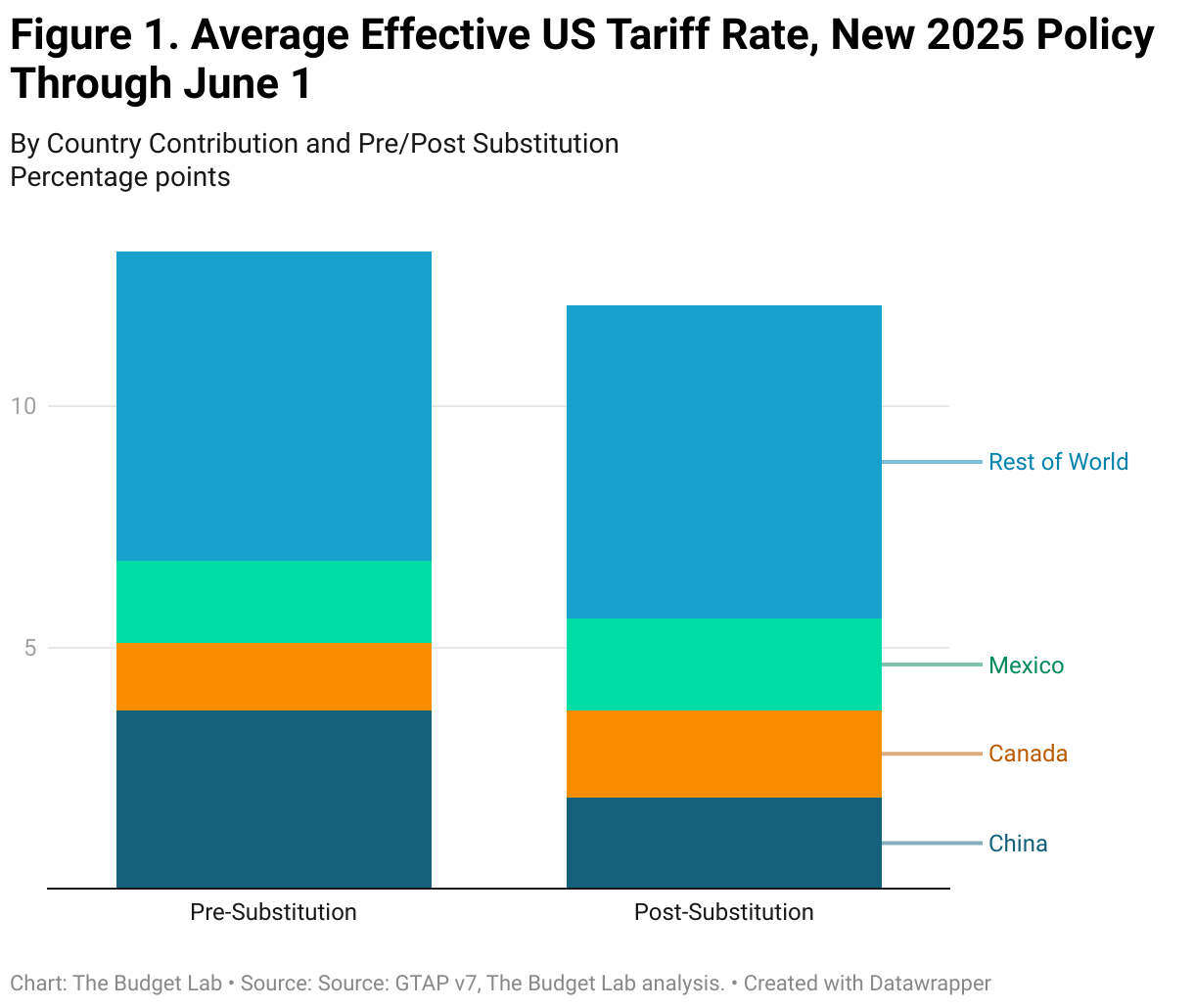

Average Effective Tariff Rate

The distinction between pre-substitution metrics (before consumers and businesses shift purchases in response to the tariffs) and post-substitution (after they shift) is a crucial one. One metric where the difference is meaningful is the average effective tariff rate.

Measured pre-substitution—assuming there are no shifts in the import shares of different countries—the 2025 tariffs to date are the equivalent of a 13.2 percentage point increase in the US average effective tariff rate. That calculation assumes that, for example, the share of imports from China remains at 14%, where it was in 2024. This is the right way to think about the tariffs from the perspective of consumer welfare, since it reflects the full cost faced by consumers before they start making difficult spending choices. This increase would bring the overall US average effective tariff rate to 15.6%, the highest since 1937.

Post-substitution—after imports shift in response to the tariffs—the 2025 tariffs are a 12.1 percentage point increase in the US average effective tariff rate, which brings the overall US effective tariff rate to 14.5%, the highest since 1938.

The timing of the transition from “pre” to “post” substitution is highly uncertain. Some shifts are likely to happen quickly—within days or weeks—while others may take longer.1

Average Aggregate Price Impact

The 2025 tariffs imply an increase in consumer prices of 1.5% in the short-run, assuming no policy reaction from the Federal Reserve. This is a pre-substitution number that captures consumer welfare effects. It is the equivalent of a loss of purchasing power of $2,500 per household on average in 2024 dollars. The post-substitution price increase settles at 1.3%, a $2,100 loss per household.

US Real GDP & Labor Market Effects

All 2025 US tariffs plus foreign retaliation lower real GDP growth by -0.5pp over calendar year 2025 (Q4-Q4). The unemployment rate ends 2025 0.3 percentage point higher, and payroll employment is 376,000 lower that same quarter. The level of real GDP remains persistently -0.32% smaller in the long run, the equivalent of $100 billion 2024$ annually, while exports are -14% lower.

Long-run US Sectoral Output & Employment Effects

Tariffs shrink the overall size of the US economy in the long-run by 0.3%, but beneath aggregate GDP they also drive reallocation across US sectors. Long-run output in the manufacturing sector expands by 1.3% under the tariffs, with nonadvanced durable manufacturing output 2.0% larger, nondurable manufacturing 1.1% larger. However, advanced manufacturing is down by 1.8%. Moreover, the expansion of the overall manufacturing sector more than crowds out the rest of the economy: construction contracts by 2.9%, agriculture by 0.9%, and mining & extraction by 0.7%.

Global Long-run Real GDP Effects

Canada has borne the brunt of the damage from US tariffs so far, with its long-run economy -1.9% smaller in real terms (reflecting both US tariffs and Canadian retaliation to date). China’s economy is -0.3% smaller, almost as large as the hit to the US. The EU economy is 0.1 percentage point larger in the long-run, while the UK’s is 0.2% bigger thanks in part to the benefits of US-UK trade deal.

Fiscal Impact & Historical Context

The 2025 tariffs to date, were they to remain in place (and not expire after 90 days), would raise $2.4 trillion over 2026-35 conventionally-scored.2 Given the negative output effects of the tariffs, there would be additional dynamic reductions in tax revenue as a result. Based on Congressional Budget Office rules-of-thumb, TBL estimates that these effects would total -$347 billion over the decade, bringing total dynamic revenue to $2.0 trillion over 2026-35.

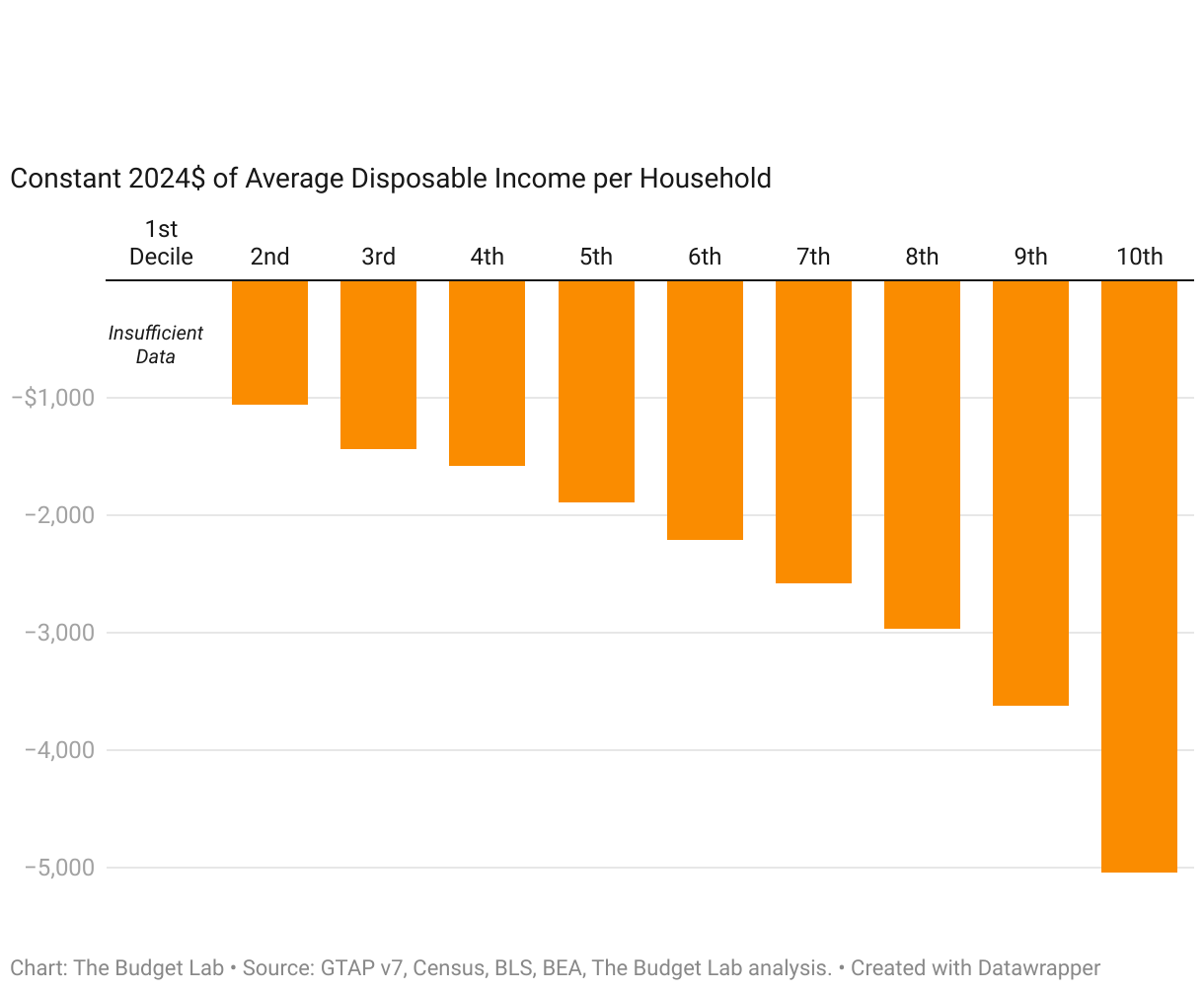

Short-run Distributional Impact

Tariffs are a regressive tax, especially in the short-run. This means that tariffs burden households at the bottom of the income ladder more than those at the top as a share of income. The regressivity is about the same when looking at all 2025 tariffs: the burden on the 2nd decile is 2.5x that of the top decile (-2.5% versus -1.0%). The average annual cost to households in the 2nd, 5th, and top decile rise to $1,100; $1,900; and $5,000 respectively.

Tariffs are more distributionally-ambiguous in the longer-run. Tariffs reduce both labor income and above-normal returns to capital, or rents. We assume that owners of capital hold rents rather than consume them in the short-run, but do consume them over their lifecycle in the long-run. The implication is that the tariff burden is more regressive in the short-run and more evenly-distributed across households in the long-run.

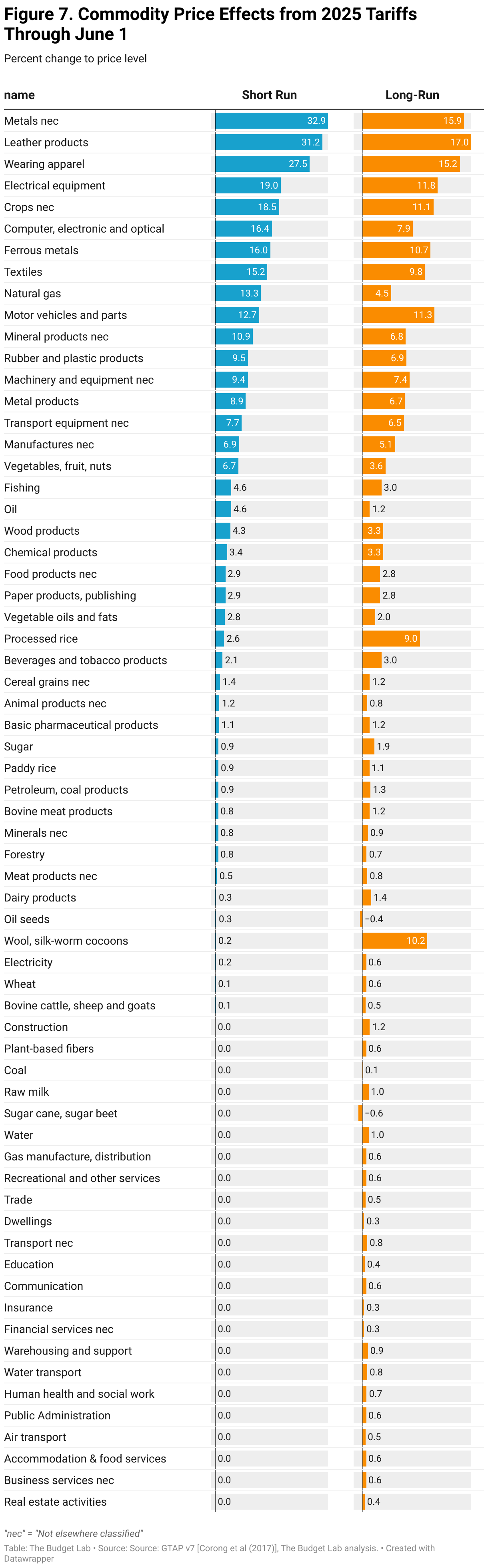

Commodity Price Effects

The charts below show how the 1.5% price level increase from the 2025 tariffs to date would look across individual commodities in the short-run (pre-substitution), as well as the 1.3% long-run price increase (post-substitution). Some high level takeaways:

- Consumers face high increases in clothing and textile prices in the short-run: prices increase 31% for leather products (shoes and hand bags), 28% for apparel, and 15% for textiles. After substitution and global supply shifts in the long-run, prices remain 17%, 15%, and 10% higher, respectively.

- Food prices rise 2.4% in the short-run and stay 2.4% higher in the long-run. Fresh produce is initially 6.7% more expensive while stabilizing at 3.6% higher.

- Motor vehicle prices rise 12.7% in the short-run and 11.3% in the long-run, the the equivalent of an additional $6,100 and $5,400 respectively to the price of an average 2024 new car.

Footnotes

- TBL assumes throughout its tariff analysis that the transition to longer-run GTAP equilibria occurs after three years.

- TBL employs a “relaxed conventional” assumption for the retaliation scenario, whereby foreign income is permitted to fall but US income remains fixed.