Tax Provisions in the Reconciliation Bill: Combined Distributional Impacts

Key Takeaways

-

The tax provisions of the reconciliation bill would be regressive: as a share of income, average tax cuts are larger for higher-income households than for lower-income households.

-

Regressivity is largely driven by the extension of expiring tax cuts, while new provisions in the bill, like no tax on tips and overtime, are generally targeted towards middle- and upper-middle income households.

-

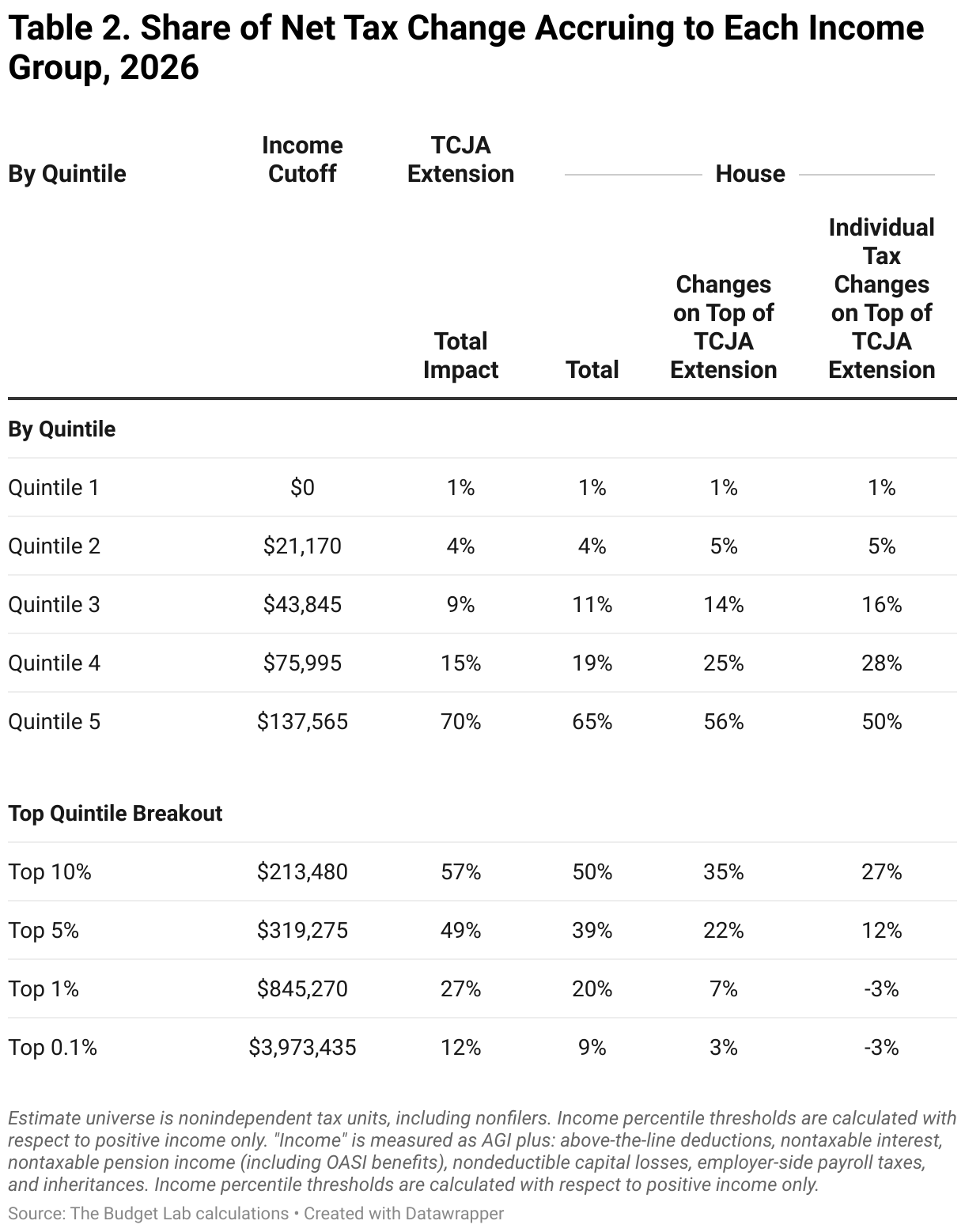

Because low-income Americans often do not owe any tax to begin with, new tax cuts provide little tax relief for these groups. About 5 percent of the bills’ total tax change in 2026 would accrue to the bottom two quintiles.

-

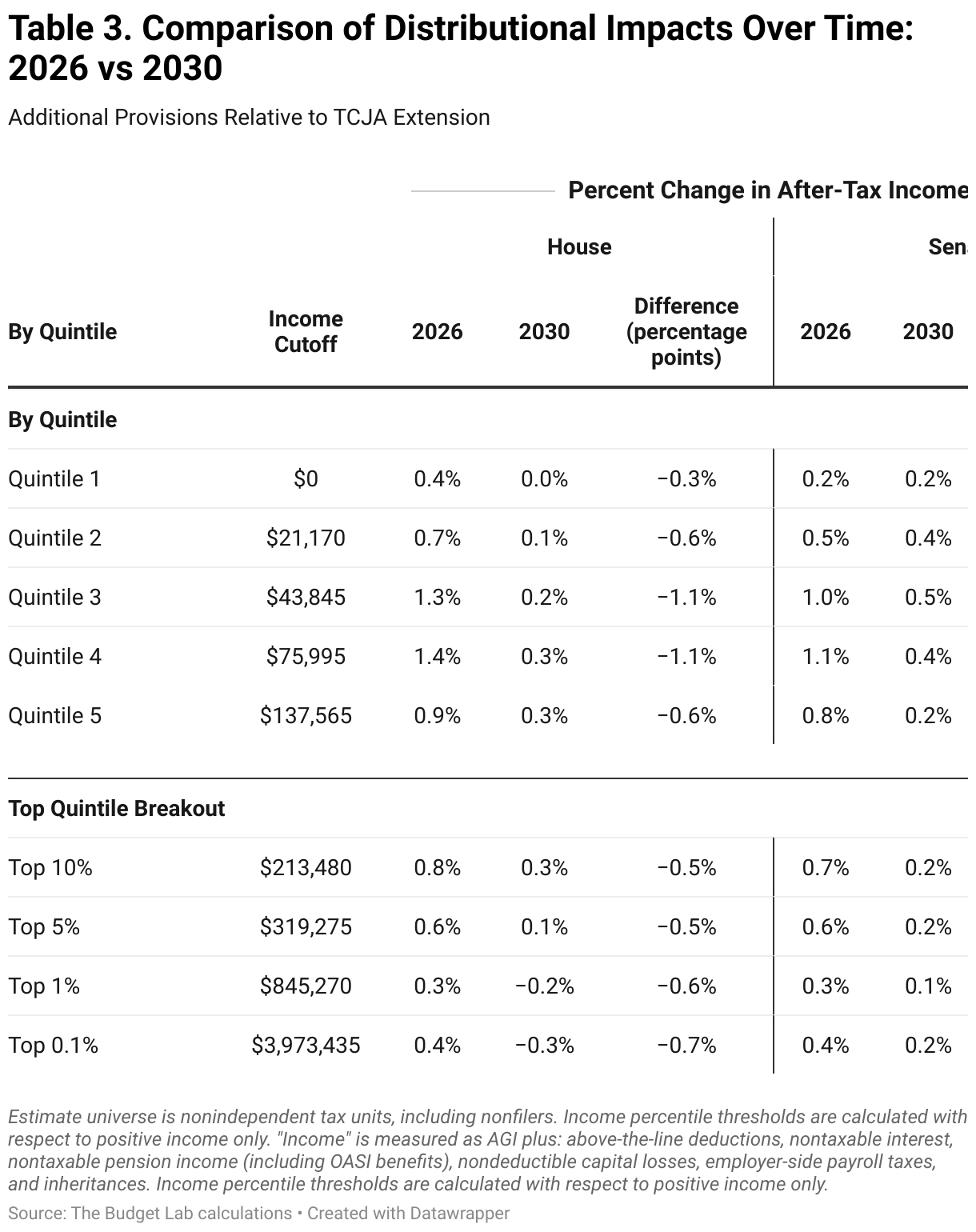

Many of the bill’s new provisions are temporary. Starting in 2029, average tax cuts would fall for most income groups.

Both the House and Senate versions of the reconciliation bill would make meaningful changes to individual, estate, and business taxes. A prior Budget Lab analysis broke down the impact of these tax changes by looking at how each provision, considered independently, would affect after-tax incomes across the income distribution.

In this piece, we build on our previous work by looking at the combined impact of these provisions. We focus on two metrics: percent change in after-tax income and share of the total tax change accruing to each income group. We also compare the effects of each bill to those of a straightforward extension of the Tax Cuts and Jobs Act (TCJA).

Tables 1, 2, and 3 below present our findings, underscoring several important takeaways.

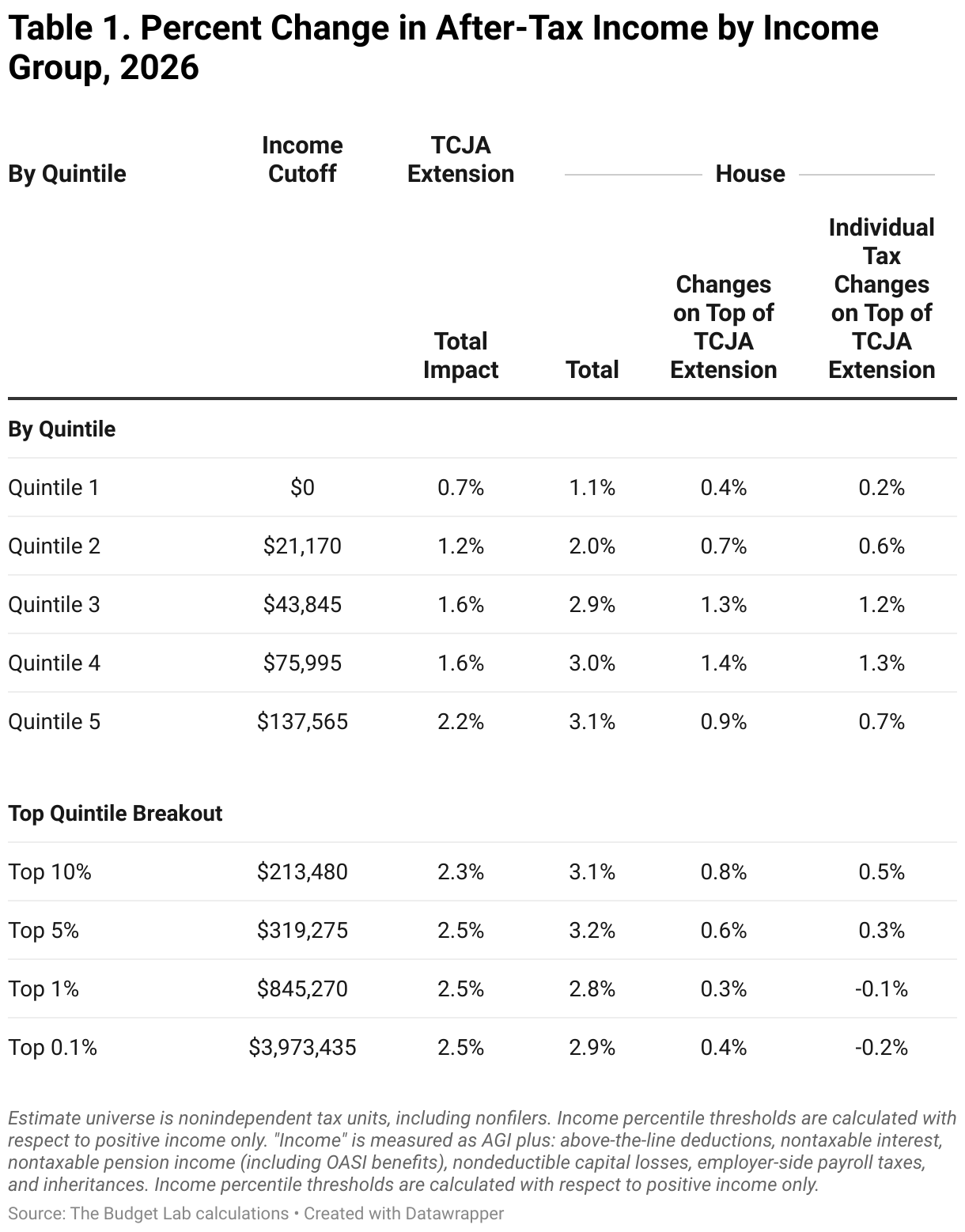

TCJA extension would be regressive. As a share of income, average tax cuts rise as income rises. Almost half of the total benefit of extending the expiring pieces of the 2017 tax law, the Tax Cuts and Jobs Act (TCJA), would accrue to the top 5 percent of households by income. These figures include the effects of extending the estate tax cuts and business investment depreciation rules in place as of 2025.1

Each version of the bill would be regressive (though slightly less so than TCJA extension). Across quintiles, both the House and Senate bills. Within the top quintile, however, the story is mixed: due to new limitations on itemized deductions and changes to Alternative Minimum Tax, benefits (as a share of income) either remain flat or decline slightly at the very top. These figures include the effects of the incremental estate tax and depreciation changes above and beyond a straightforward TCJA extension.2

New income tax provisions in each bill are tailored to benefit middle- and upper-middle income households. Both the House and Senate bills would introduce new tax breaks, such as tax exemptions for tips, overtime, and car loans. Each would also increase the maximum value of the Child Tax Credit and exempt more income from tax for seniors. These provisions are designed with phaseouts, meaning that higher-income households wouldn’t benefit. And tax relief in the form of new deductions or larger nonrefundable credits does not accrue to low-income households for the reasons described above. Along with several other reforms which pare back deductions for high-income households, these design choices combine to concentrate benefits in the $50,000 to $300,000 income range.

But many of these new benefits are temporary. By 2030, many of the provisions will have expired per sunsets written into the bill. This includes both the “no tax on...” provisions as well as sunsets for the expanded Child Tax Credit and business cost recovery changes in the House version. Relative to the first full year of enactment (2026), average tax cuts would fall for most income groups in 2030.

Benefits would be minimal for the bottom half of households. Because the US income tax system is progressive, many households in the bottom half of the income distribution do not owe any income tax. Therefore, further income tax cuts in the form of lower rates or new deductions offer little to no benefits to these households. Only about 5 percent of the total tax cut in 2026 would flow to the bottom two quintiles in either bill.

Taxes are only one side of the equation. This analysis is limited to tax provisions only. Including the spending provisions increases the regressivity of the legislation, since most of the broader bill’s spending cuts likely fall most acutely on lower-income households. The Budget Lab is in the process of updating its prior analyses of both the spending and tax side.

Footnotes

- For estate taxes, the 2026 policy change consists of increasing the exemption from about $7.2M to $14.3M. For depreciation, the 2026 policy change consists of increasing the bonus depreciation rate from 20% (2026 current law) to 40% (2025 current policy).

- For estate taxes, the 2026 policy change consists of increasing the exemption from about $14.3M to $15M. For depreciation, the 2026 policy change consists of increasing the bonus depreciation rate from 40% (2025 current policy) to 100% (the proposal under both versions of the reconciliation bill).