Estimated Budgetary, Distributional, and Macroeconomic Effects of “Tariff Dividends”

Key Takeaways

-

A one-time $2,000 per-person rebate with an income limit of $100,000 would cost $450 billion. That is about twice as large as the total revenue that will be raised by the administration’s tariff hikes in 2026, per Budget Lab estimates.

-

Because every person below the income limit would receive the same dollar amount, the rebate would be progressive—that is, it represents a larger share of income for lower-income families.

-

GDP growth and employment would rise slightly in 2026 (0.3 and 0.15 percentage points, respectively). But this temporary boost to output would be erased after several years.

-

Impacts on price pressures in the economy would be muted. The annual rate of inflation would increase by less than 0.1 percentage points over the next few years, with a cumulative impact on the price level of about 0.2 percent after a decade.

-

In 2035, the debt-to-GDP ratio would be about 1.5 percentage points higher than its baseline projected value of 118.5 percent.

Background

President Trump has recently introduced the idea of a “tariff dividend”—a one-time payment of $2,000 to each American, financed with federal tariff revenue. Beyond social media posts and subsequent television appearances by Treasury Secretary Scott Bessent, who indicated the payments would be limited based on income, there are no firm details on how such a policy would work. In this post, we treat the “tariff dividend” as an income-limited refundable tax credit and look at the budgetary, distributional, and macroeconomic consequences of such a policy.

Policy Design Considerations

In this post, we assume the “tariff dividend” would take the form of a one-time refundable credit of $2,000 per person for tax units with 2025 Adjusted Gross Income (AGI) strictly below $100,000, with no adjustment for filing status and no limit on the number of eligible people in the household.

Under this interpretation, a married couple with two children and AGI of $95,000 would receive up to $8,000 (four eligible people at $2,000 each). A single filer with AGI of $99,000 would receive $2,000. But in both cases, an additional dollar of income that pushes taxable income above the $100,000 cutoff would cause the entire payment to disappear.

This is one of many possible design options, and choices along certain dimensions—e.g., should the credit phase out over an income range, or should eligibility thresholds vary by marital status—would present budgetary, distributional, and incentive tradeoffs. For instance, structuring the income limit with a phaseout range rather than a cliff would mitigate income timing incentive concerns but increase the budget cost. See the Appendix for budget cost estimates of alternative design options.

Estimated Budget Cost

For the purposes of budget accounting, existing tariff policy and a new “tariff dividend” are conceptually separate. At different times, the administration has argued that tariff revenues will simultaneously (1) finance tax cuts under the 2025 reconciliation act (2) finance the dividend (3) reduce the deficit. But each dollar of tariff revenue can be “used” only once. If tariff receipts are devoted to tax cuts or rebates, they are not available to reduce the deficit. Conversely, if tariffs are treated as a tool for deficit reduction, then any new transfers—whether called “tariff dividends” or otherwise—must be financed by higher borrowing, lower spending elsewhere, or other tax increases.

Using the Budget Lab’s Tax-Simulator model, we estimate that a per-person credit with a strict $100,000 income cutoff would cost about $450 billion. For context, the Budget Lab estimates that the administration’s tariffs will raise about $240 billion next year. (This figure falls by more than half if IEEPA is invalidated by the Supreme Court and the revenue is not replaced with tariffs under other legal authorities.)

This is a conventional revenue estimate, meaning it does not incorporate any macroeconomic feedback (such as people working fewer hours at the end of 2025 to stay under the income limit). If we account for the second-order revenue impacts of slightly higher near-term growth, net budget cost falls to about $410 billion.

The policy would also create ongoing future interest costs due to a higher stock of debt. These costs are about 0.05% of GDP annually over the next ten years, which brings the total cost estimate to about $620B over the FY2026-2035 period. The debt-to-GDP ratio would rise by about 1.5pp, up from its projected baseline level of 118.5 percent.

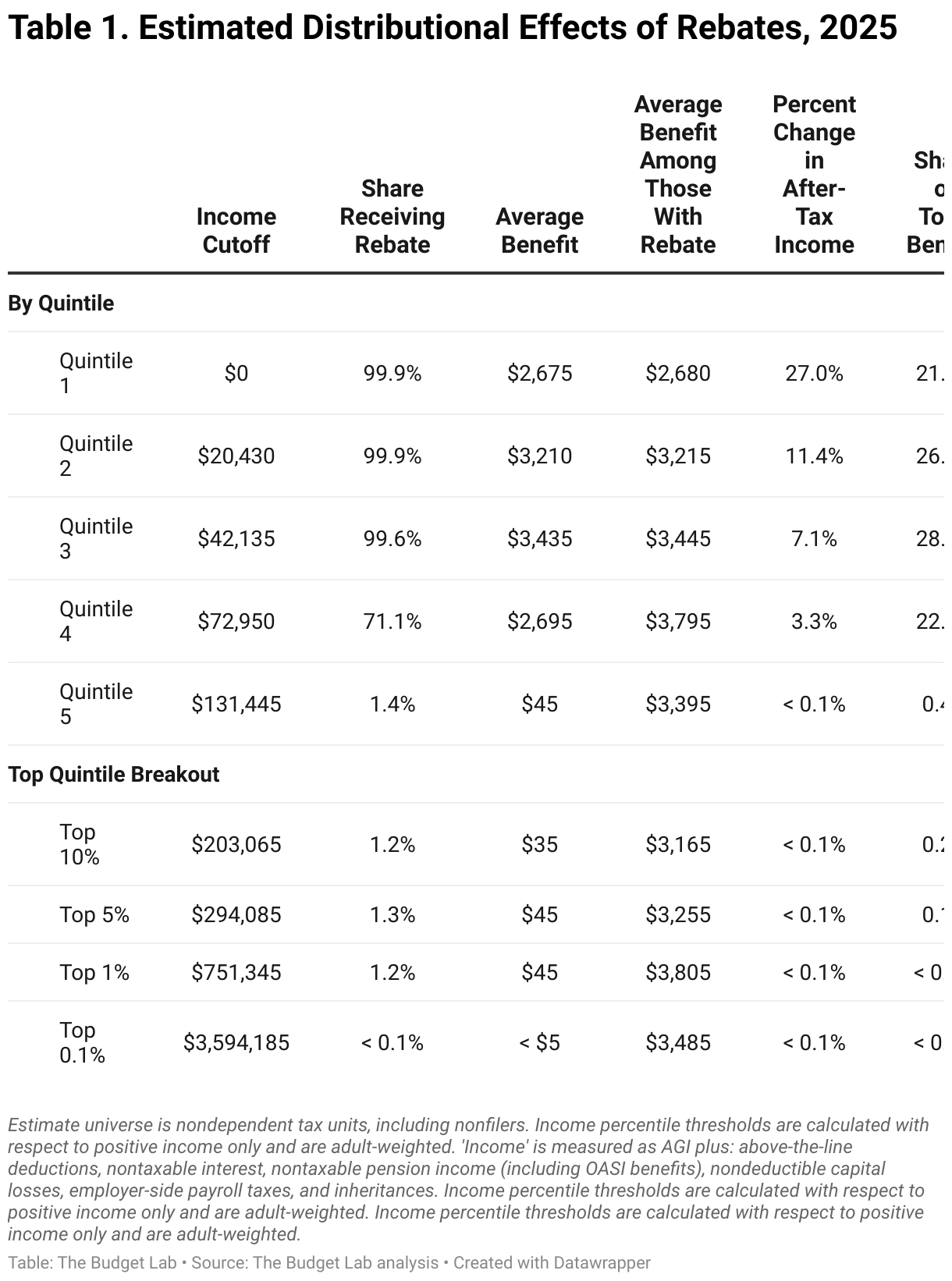

Estimated Distributional Effects

Per-person rebates are distributionally progressive. This is because a fixed dollar rebate represents a larger fraction of income for low-income households than it does for high-income households.1 In addition, income limitations would increase progressivity. Table 1 shows our estimated distributional impacts for the “tariff dividend” policy, excluding any second-order effects from macroeconomic feedback or eventual financing of the policy.2

Estimated Macroeconomic Effects

In this section, we use the United States Macro Model (USMM) to estimate the macroeconomic effects of “tariff dividend” rebates. As explored in a prior Budget Lab report, the macroeconomic impacts of fiscal policy shocks depend in part on how the Federal Reserve conducts policy. In our simulations, we assume the Federal Reserve reacts to the policy change and succeeds over the medium term in meeting its employment and inflation goals.

Figure 1 shows our estimates for four key indicators: real GDP, unemployment, the Consumer Price Index (CPI), and the rate on 10-year Treasury bonds. These series underscore several big-picture takeaways:

- Temporary, retroactive policy does not change incentives to work and invest. The “tariff dividend”, if designed to be a one-year policy with eligibility based on 2025 income, has no direct bearing on how much households work or how much businesses invest. This is because the rebate amount that a household gets is based on past economic decisions, not decisions in the future, and therefore represents a pure “windfall”. Our simulations bear this out: after temporary improvements due to demand-side factors, GDP and unemployment return to their longer-run baseline projection levels.

- Price impacts are relatively modest. We estimate that the rebates would create inflationary pressures of less than 0.1 percentage points per year. After a decade, the cumulative price level impact is about 0.2 percent.

- A one-off fiscal shock of this size is relatively small in terms of the broader economy. Our results show relatively muted effects on all major macroeconomic indicators. Some back-of-the envelope math helps illustrate why this is the case. Assuming a marginal propensity to consume out of the tariff dividend of 0.25, consistent with evidence from recent instances of temporary tax rebates, implies a one-time direct increase in spending of 0.25 x $450 billion = $113 billion, approximately 0.35% of GDP. Over the full 10 years, the rebate generates consumer spending that averages 0.06% of GDP.3

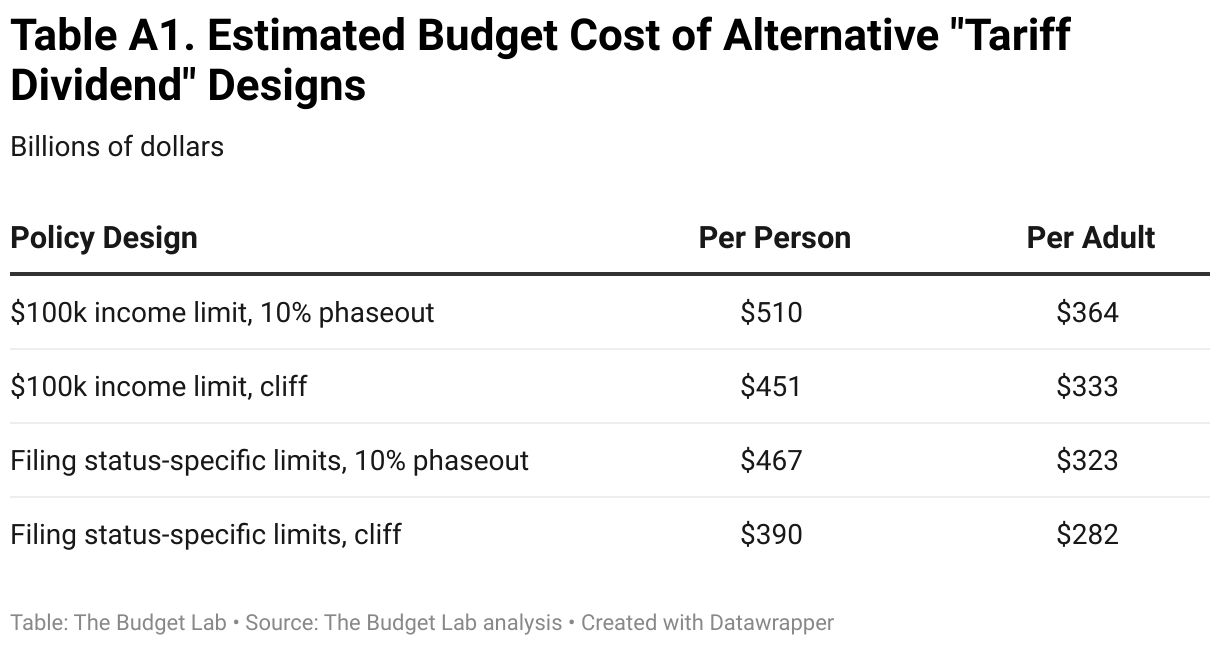

Appendix

As stated in the text, the ultimate effects of a "tariff dividend" policy depend on the exact policy design details. This report explores one design option: a $2,000 per-person credit with a flat $100,000 income cutoff (cliff). To offer a sense of magnitudes involved for different design choices, we show the budget costs of alternative designs along three margins:

- Per-person vs. per-adult: Should the credit include children, or only adults?

- Income threshold: Should the income limit be a flat dollar amount for all filing statuses, or should it vary by filing status? Higher values for joint returns would adjust the means-test for family size and reduce marriage penalties. In the exercise below, we set the AGI limit to $50,000 for single filers, $100,000 for married filing jointly, $75,000 for head of household.

- Phaseout structure: Should the credit phase out gradually or disappear entirely once income exceeds the threshold (cliff)? In the exercise below, we illustrate the effects of a 10% phase out rate (i.e. the rebate is reduced by 10 cents for every dollar of AGI above the threshold).

Table A1 shows the estimated budget cost for each combination of these design choices.

Footnotes

- 1

The exact size of this effect depends on how broadly “income” is defined. If income is defined narrowly such that only market income is included, the relative impact of a cash transfer for low-income families is large. If income is defined broadly to include nonmarket and noncash sources of income like transfer programs and familial transfers, the relative effect is smaller. TBL’s distribution tables include only a limited subset of nonmarket income and thus report very large figures for the low end of the distribution for the “percent change in after-tax income” metric.

- 2

In the interest of expediency, we do not include the effects of deficit financing on this distribution, a topic which TBL has written about and is working on incorporating into distributional analysis. TBL plans to produce updated analysis accounting for this dynamic.

- 3

A portion of the tariff dividend is saved, which supports a slightly higher level of spending in the future.